Analysis of the day

M&A and Fundraising Analysis for July 18, 2026 SUBTITLE=== Building maintenance, tabular AI, industrial robotics, and textile recycling: today's capital is deployed on assets that withstand the test of time as much as on short-term technological bets — the complete overview for decision-makers and investors. ===BODY=== The day combines two seemingly unrelated logics: on one hand, so-called "defensive" assets — building maintenance, waste management, accounting expertise — attracting mid-market and large-cap tickets; on the other, a handful of technological bets where money is invested quickly and heavily, from AI for corporate spreadsheets to physical robotics and underground geolocation. France is at the heart of both movements. # 🤝 M&A Deals ## Batibig: When an "Unexciting" Asset is Worth Over a Billion **Charterhouse Capital Partners** is entering exclusive negotiations to acquire **Batibig**, a French building maintenance and repair group, in a transaction valued at over **€1 billion** — with a double-digit multiple and a full divestment of shares by **Siparex** and **EMZ**, the two exiting funds. Founders **Charles and Justin Bignon** are reinvesting and retaining management. Closing is expected in October 2026. The surface reading: a strong growth LBO, buy-and-build, pan-European, in a consolidating sector. Nothing surprising for those following the facilities services market. What deserves attention is the market context in which this deal was closed. The LBO market is described as "congested" by the players themselves — processes drag on, valuations are fiercely negotiated, buyers hesitate. Batibig did the opposite: launched in March, signed before summer, fifteen expressions of interest in the first round, including **CVC**, **ICG**, **Partners Group**, and **Krefeld**. It wasn't the size that accelerated the process, it was the nature of the asset. Over 300,000 interventions per year, revenues exceeding **€500 million**, demonstrated growth, and — crucially — an activity that depends neither on an investment cycle, nor a political decision, nor imminent technological disruption. When a boiler breaks down on a Sunday, no one waits for the next budget window. *In a market where mid and large-cap capital is desperately seeking assets with recurring, non-cyclical revenues, Batibig played the role that highway infrastructure once did: something you cannot not use. It is precisely this profile that drove up the bids.* For an acquirer or executive in France: the pan-European build-and-build strategy announced by Charterhouse means that regional building maintenance targets will be approached in the coming months. First and second tier. ## SAP Swallows Prior Labs: Spreadsheet AI, Not Chatbot Chatter **SAP** is finalizing the acquisition of **Prior Labs**, an AI laboratory founded in Freiburg eighteen months ago, for a total commitment exceeding **€1 billion** over four years. The startup had raised **€9 million** in pre-seed funding in 2025. Prior Labs will continue to publish its research and operate under its own brand. Everyone talks about generative AI, large language models, enterprise chatbots. Prior Labs does the exact opposite: its models read tables — rows, columns, structured databases — and predict, classify, and detect anomalies from this raw material. Its TabPFN model was published in *Nature* and has set the state of the art in hundreds of independent studies. The turnaround lies in the nature of the problem SAP seeks to solve. Companies have heavily invested in generative AI tools that answer prose questions well but remain blind to a sales data file, a cash flow forecast table, or an industrial maintenance log. Yet this is precisely where real decisions live: in the structured data of SAP, Oracle, Salesforce. Prior Labs fills this gap with an approach that large generalist models do not cover — and SAP knows this, to the point of freezing recruitment and travel to fund the AI push. *Eighteen months of existence, nine million raised, a billion-euro acquisition: the multiplier is less about revenue than about the rarity of a skill that SAP could not rebuild internally in time. This is a strategic acquisition, not a revenue acquisition.* For European executive teams: this is one of the rare recent acquisitions where a European software champion buys a cutting-edge European laboratory and keeps it open, publishing, and independent. The strategic signal is as valuable as the deal itself. ## CVC DIF Acquires EcoEridania: The Green Annuity at €1.1 Billion **CVC DIF**, the infrastructure arm of the **CVC Capital** group, is signing the acquisition of a majority stake in **EcoEridania**, a leading Italian special waste management company, for a valuation exceeding **€1.1 billion**. The seller is **iCon Infrastructure**. More than twenty international investors were in the running; the final round pitted CVC DIF against **Ardian** and **Swiss Life Asset Managers**. Industrial and special waste management presents exactly the profile that infrastructure funds seek: long-term contracts, regulated or quasi-regulated revenues, structurally growing demand driven by traceability and depollution obligations, and a regulatory barrier to entry that makes competition difficult. *EcoEridania is not a growth story — it is a story of sustainable annuity in a sector where regulation is the best bulwark against disruption.* ## Mollie Raises €350 Million to "Not Build a Superapp" **Mollie**, the Dutch payment fintech, announces a **€350 million** European expansion plan. The title of the Sifted article quotes the CEO: "Superapp is a convoluted word" — in other words, the company explicitly rejects the temptation to aggregate all financial services under one roof, a strategy attempted by Revolut, N26, and others. *The clarity of positioning here is the signal: in a market where generalist fintechs are fighting on all fronts with rising acquisition costs, Mollie bets that depth in SME payments is worth more than breadth. This is a choice of discipline as much as strategy.* ## Volati Acquires Tramex: Humidity Measurement as an Add-on The Swedish industrial conglomerate **Volati** is acquiring **Tramex**, an Irish manufacturer of professional moisture meters founded in 1974, for approximately **€51 million**. The transaction is the first add-on for **Corroventa**, Volati's platform specializing in water damage drying. Tramex generates approximately SEK 90 million in annual revenue with an adjusted EBITA margin of around 20%. The integration is logical: Corroventa dries, Tramex measures. Both products target the same customers — disaster restoration companies, building inspectors, construction companies. *A pure technical complementarity add-on, without market risk: Tramex's margin mechanically improves the platform's consolidated profile.* ## Hexawin Joins a Build-up Group **Hexawin**, an IT service provider based in Vitrolles offering cloud hosting and IT services to SMEs, becomes the fourth acquisition of the group formed by a family office, for **€35 million**. This is a classic sectoral consolidation operation in digital services for SMEs, a segment that remains highly fragmented in France. ## Baker Tilly Absorbs Corex in Hauts-de-France **Baker Tilly France** (**€219 million** in revenue, 2,200 employees) is acquiring **Corex**, an accounting firm established in Saint-André-lez-Lille since 1958, for approximately **€17 million**. Corex employs 48 people, 8 partners, serves 2,300 clients, and generated €7.5 million in revenue in its last fiscal year. The transaction creates a new regional territory for Baker Tilly in Hauts-de-France, as part of its Convergence 2030 plan aiming for €400 million in revenue within four years. The consolidation of accounting expertise follows a well-established mechanism: independent regional firms struggle to invest alone in the digital tools, CSR, and wealth management advice that SME clients are beginning to demand. Baker Tilly provides the range of services, Corex provides local roots and a client base. *Nothing unexpected — but this is precisely the type of acquisition that builds a mid-sized professional services firm over ten years.* ## Audensiel Establishes Presence in Occitanie via iTekway **Audensiel**, a Parisian consulting and digital services group (3,500 employees, €350 million in revenue targeted in 2026), is acquiring the **Efis** group — which includes **iTekway Occitanie** and **iTekway Île-de-France** — for **€8 million**. The two entities employ approximately 100 people, 75% of whom are consultants with disabilities, and generate over €5 million in revenue. The **Impact Partners** fund is exiting the capital. The operation combines two logics: a strategic establishment in Toulouse's aerospace and space sector, and the strengthening of an inclusive employment policy that is becoming a criterion for accessing large corporate markets. *For Audensiel, iTekway is not just a revenue acquisition — it is a commercial differentiation asset in tenders where ESG criteria carry weight.* ## Gruppo Peppe: An LBO Without a Sponsor Fund **Gruppo Peppe**, a young Parisian group of Neapolitan pizzerias with **€20 million** in revenue, is opening its capital to a sector-specific fund as part of a sponsorless LBO, for approximately **€35 million**. A sponsorless LBO — without a traditional private equity fund at the helm — is a structure that gives founders more operational freedom while providing them with growth debt. In the restaurant industry, where cycles are short and decisions are quick, this is often a better fit than an institutional sponsor. ## France-Germany vs. China: A Common Trade Roadmap According to *Les Échos*, France and Germany are preparing a common roadmap to coordinate their response to Chinese trade practices. No financial operation here, but a signal of regulatory and geopolitical framework: for companies exposed to Chinese competition — industrial equipment, chemicals, batteries, electric vehicles — Franco-German coordination, if it materializes, could alter the conditions of access to the European market for Chinese products. *To be watched by anyone arbitrating between Asian sourcing and local production.* ## Danske Bank Explores Significant Risk Transfers **Danske Bank** is evaluating Significant Risk Transfer (SRT) operations to free up regulatory capital, joining a broader movement among European banks. These instruments allow the transfer of credit risk from a loan portfolio to third-party investors, without divesting ownership. *For alternative credit funds and insurers seeking yield on bank-quality assets, this is a window to access exposures that do not go through the traditional bond market.* # 🚀 Fundraisings ## Mistral and EQT: European Private Equity Enters the Race for Large Models **EQT** is reportedly in negotiations to lead or co-lead **Mistral AI**'s Series D through its **€5 billion Scaleup Europe** fund, according to sources cited by ONE.WORKS. The financial details of the round remain partially obscured in the source, but the dynamic is clear: Mistral, already valued at around **$6 billion** during its Series C, would attract a leading European buyout player as a lead investor in a growth round. EQT's entry — a fund whose culture is control, operational optimization, and defined-horizon exit — into the capital of a generative AI laboratory is a signal of the sector's maturity as much as a structural anomaly. Large language models have colossal infrastructure costs, fierce global competition, and still uncertain revenue trajectories. This is not the usual profile of an EQT investment. *What is at stake here goes beyond Mistral: if EQT validates this round, it means that European private equity is beginning to treat sovereign AI laboratories as strategic infrastructures — assets to be protected as much as to be made profitable. The logic is no longer just financial, it is geopolitical.* ## Syntetica: Brands Fund Their Own Material Supplier **Syntetica**, a French deeptech company specializing in textile nylon recycling based in Reims, raises **$30 million** (approximately **€28 million**) in Series A. The round is led by **Bpifrance** via its **Ecotechnologies 2** fund (France 2030), with **EQT Ventures**, **SWEN Capital Partners**, **Lululemon**, **MAS Holdings**, and the family offices of **Peugeot**, **Etam**, and the largest shareholder of **Indorama Ventures**. The European Innovation Council also provides equity and grants. The money will fund the construction of a first commercial demonstration plant in France. The composition of the round is worth noting. Lululemon, Etam, and MAS Holdings are not just financial investors: they are potential customers, or more precisely, companies that have a problem that Syntetica claims to solve. Recycled nylon still accounts for about 2% of the global market (according to figures cited by the company, based on Textile Exchange); almost all nylon textile waste ends up incinerated or in landfills. The technical reason: Nylon 6 and Nylon 6,6 — the two dominant grades — mix in waste and are difficult to separate. Syntetica claims to be able to recycle both simultaneously, at low temperatures, leaving the elastane present in mixtures intact. *By investing, Lululemon and Etam are not making a philanthropic bet: they are securing a future supply of virgin-quality recycled material, while funding the infrastructure that will make it possible. This is upstream integration disguised as impact investment — and it is probably the only way to bring this type of industrial asset to fruition in Europe.* For a French industrialist or investor: the "brands in the recycler's capital" model is exportable to other materials (polyester, cotton, wool). Syntetica sets the precedent. ## Stoïk: SME Cyber Insurance Moves to Series C **Stoïk** closes **€20 million** in Series C. The round is led by **Impala** (Veyrat family), a new investor, with **Opera Tech Ventures** and existing investors **Alven** and **Andreessen Horowitz**. The company now protects over 10,000 businesses, collaborates with over 2,000 broker partners, covers over 600 new businesses per month, and closed 2025 with over 200% annual growth, for nearly €50 million in gross written premiums. Stoïk has built a model that few players have successfully assembled: cyber insurance, proactive prevention, and an incident response team under one roof, targeting SMEs — a segment that large insurers handle poorly because it is costly to address individually. Impala's entry, a long-term family shareholder, alongside a16z, is a signal of credibility as much as capital. *At €50 million in premiums, Stoïk is no longer a startup — it is a specialized insurer in the industrialization phase.* ## Forsee Power: Refinancing Under Pressure **Forsee Power**, a French manufacturer of battery systems for sustainable mobility, announces a capital increase of **€20 million** led by **FCAP Investors** (a Singaporean fund) with the participation of **Eurazeo**, an existing reference shareholder. The operation is subject to prior authorization from the Ministry of Economy under foreign investment control. The press release speaks of a "demanding market environment" and an operation aimed at "strengthening equity." This vocabulary, in the world of finance, does not describe serene growth: it describes a company that needs to strengthen its balance sheet to stay on course with its strategic plan in a sustainable mobility battery market that has slowed faster than anticipated — between cost pressure, delays in electric fleet deployment, and Asian price competition. *The entry of a Singaporean fund like FCAP, subject to French regulatory scrutiny, highlights that strategic assets of the energy transition remain under surveillance — even when they are seeking emergency capital.* ## Wheere: Locating Where GPS Doesn't Reach **Wheere**, a Montpellier-based startup founded in 2020, raises **€8.5 million**, bringing its total raised to approximately **€20 million** since its inception. The company develops indoor and underground geolocation technology based on low-frequency VHF radio waves, capable of locating a person or object through up to 50 meters of concrete with sub-meter accuracy, using only four antennas per square kilometer. The target applications are industrial and defense: tracking isolated workers, traceability of hospital equipment, coordination of rescue efforts in collapsed buildings, navigation in GPS jamming zones. *In a context where GPS jamming has become a common tactic in conflict zones and the resilience of navigation systems is a defense priority, Wheere addresses a need that did not exist as a market five years ago.* ## SWISSto12: Smaller GEO Satellites, Bigger Raise **SWISSto12**, a Swiss space startup, closes a **$70 million** (approximately **€64 million**) Series C, bringing its total raised to over $100 million. The company had also secured an additional $73 million through the ESA HummingSat program in January 2026. It reports **$140 million** in revenue in 2025 and an order book exceeding **$500 million**, with commitments from **SES** and **Viasat**. SWISSto12 builds small geostationary satellites — a breakthrough in a segment where GEO satellites traditionally weighed several tons and cost hundreds of millions. The combination of a solid order book, ESA support, and a private Series C outlines a European space player that has moved beyond the demonstration stage. *With $500 million in orders in its portfolio, the question is no longer technology — it is production capacity, which this round precisely funds.* ## microagi: Germany's Largest Seed Round Ever, Funded by Human Data **microagi**, a Munich-based startup founded by **Bercan Kilic** — former aerodynamic engineer at Red Bull Racing F1 — raises **$55 million** (approximately **€51 million**) in a seed round, the largest ever for a German startup at this stage. The round is led by **Hummingbird**, with **Northzone**, **LocalGlobe**, **Village Global**, and **redalpine**. microagi builds neither robots nor proprietary foundational models. Its bet is elsewhere: factories already have robots, but these robots do not know how to execute the precise and variable gestures required for real production. microagi collects human movement data — through its **Shift** program, which pays over 20,000 people in 15 countries to record their physical gestures — and trains models that allow existing robots to be reprogrammed. *The logic is that of human labor as training raw material: tens of thousands of people perform gestures for remuneration, these gestures become data, this data becomes robotic competence. This is a new form of outsourcing of worker know-how — no longer to low-cost countries, but to models that permanently absorb it. The paradox is clear: humans are paid to teach machines to replace humans.* For French industrialists: microagi does not sell robots; it sells adaptability for the robots you already have. This is a model that directly addresses manufacturing SMEs with heterogeneous lines that cannot afford custom robotic integration. ## Greenjets: Green Propulsion with NATO Stamp **Greenjets**, a London-based aerospace startup founded in 2022, raises **€35 million** in Series A. The round is led by **Blossom Capital**, with the **NATO Innovation Fund** (NIF), the **National Security Strategic Investment Fund** (NSSIF), and existing investors including **Tanglin Ventures**. Greenjets develops propulsion architectures covering electric ducted fans to geared turbofans, with a stated goal of reducing certification costs. The simultaneous presence of the NATO Innovation Fund and the NSSIF in the round is the clearest signal: advanced aerospace propulsion is treated as a defense capability as much as a civilian technology. *This is no longer a classic aerospace deep tech round — it is industrial sovereignty funding in the propulsion sector, with national security institutions as co-investors.* ## Isometric: Certifying Industry at AI Scale **Isometric**, a London-based startup founded in 2022 by **Eamon Jubbawy** (co-founder of Onfido), raises **€34 million** in Series A. The round is led by **AVP**, with **Lowercarbon Capital**, **Plural**, and business angels **John Doerr** and **Walter Kortschak**. Isometric began as a carbon capture project verification platform — it has already certified over 16 million tons for **Microsoft**, **JPMorgan Chase**, **Anglo American**, and **Boeing**. With this raise, it is expanding its scope to industrial certification in a broader sense: compliance, safety, sustainability standards, in a market estimated at approximately €305 billion. Its **Certify** platform ingests millions of data points — satellite imagery, sensors — to detect anomalies and direct high-risk cases to human experts. *The model is that of augmented auditing: AI handles volume, humans decide on borderline cases. In a sector where certification is a bottleneck for any industrial or energy project, reducing verification time without compromising regulatory rigor is a directly monetizable value proposition.* 📩 Subscribe to our newsletter to follow daily M&A and fundraising news: https://proplace.co/newsletter ===WHYS=== 1. the acquirer seeks to consolidate its position as a global delivery leader after the integration of Delivery Hero 2. Their strong presence in Southeast Asia would extend their geographical reach post-Delivery Hero 3. the acquirer seeks to expand its pipeline of psychedelic therapies for mental disorders, particularly postpartum depression 4. Their expertise in DMT-based medicines and psychedelic therapies complements their recent acquisition, strengthening their mental health pipeline 5. des Déchets is Veolia’s waste treatment and recycling arm, focused on collecting, sorting, treating, and valorizing waste 6. Their expertise in the circular economy and recycling complements their recent acquisition, strengthening their integrated positioning

· Proplace

🌐 Translated from the French original by AI — the French version is authoritative.

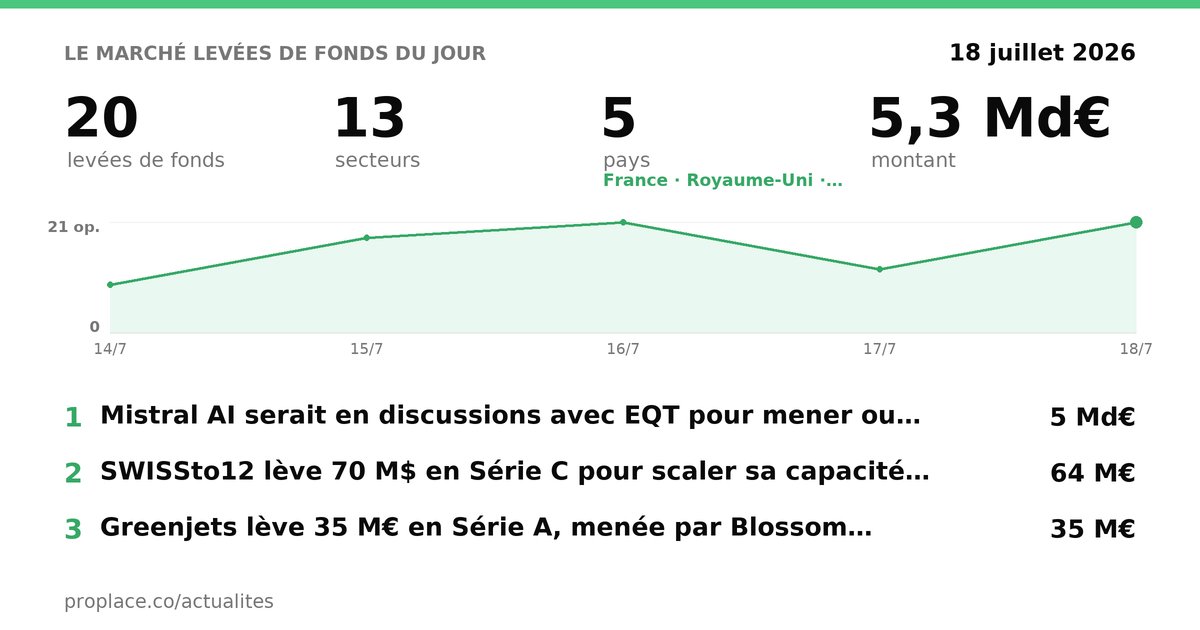

📊 Today's pulse — 43 deals · 25 M&A · 18 fundraisings · €25bn in play.

The day combines two seemingly unrelated logics: on one hand, so-called "defensive" assets — building maintenance, waste management, accounting expertise — attracting mid-market and large-cap tickets; on the other, a handful of technological bets where money is invested quickly and heavily, from AI for corporate spreadsheets to physical robotics and underground geolocation. France is at the heart of both movements.

🤝 Mergers & acquisitions today · 25

In focus — the deals we decoded

Batibig: When an "Unexciting" Asset is Worth Over a Billion

Source: headlinesbriefing.com → · Sector Construction & PropTech — 📬 subscribe to the Construction & PropTech newsletter

Charterhouse Capital Partners is entering exclusive negotiations to acquire Batibig, a French building maintenance and repair group, in a transaction valued at over €1 billion — with a double-digit multiple and a full divestment of shares by Siparex and EMZ, the two exiting funds. Founders Charles and Justin Bignon are reinvesting and retaining management. Closing is expected in October 2026.

The surface reading: a strong growth LBO, buy-and-build, pan-European, in a consolidating sector. Nothing surprising for those following the facilities services market.

What deserves attention is the market context in which this deal was closed. The LBO market is described as "congested" by the players themselves — processes drag on, valuations are fiercely negotiated, buyers hesitate. Batibig did the opposite: launched in March, signed before summer, fifteen expressions of interest in the first round, including CVC, ICG, Partners Group, and Krefeld. It wasn't the size that accelerated the process, it was the nature of the asset. Over 300,000 interventions per year, revenues exceeding €500 million, demonstrated growth, and — crucially — an activity that depends neither on an investment cycle, nor a political decision, nor imminent technological disruption. When a boiler breaks down on a Sunday, no one waits for the next budget window.

In a market where mid and large-cap capital is desperately seeking assets with recurring, non-cyclical revenues, Batibig played the role that highway infrastructure once did: something you cannot not use. It is precisely this profile that drove up the bids.

For an acquirer or executive in France: the pan-European build-and-build strategy announced by Charterhouse means that regional building maintenance targets will be approached in the coming months. First and second tier.

SAP Swallows Prior Labs: Spreadsheet AI, Not Chatbot Chatter

SAP is finalizing the acquisition of Prior Labs, an AI laboratory founded in Freiburg eighteen months ago, for a total commitment exceeding €1 billion over four years. The startup had raised €9 million in pre-seed funding in 2025. Prior Labs will continue to publish its research and operate under its own brand.

Everyone talks about generative AI, large language models, enterprise chatbots. Prior Labs does the exact opposite: its models read tables — rows, columns, structured databases — and predict, classify, and detect anomalies from this raw material. Its TabPFN model was published in Nature and has set the state of the art in hundreds of independent studies.

The turnaround lies in the nature of the problem SAP seeks to solve. Companies have heavily invested in generative AI tools that answer prose questions well but remain blind to a sales data file, a cash flow forecast table, or an industrial maintenance log. Yet this is precisely where real decisions live: in the structured data of SAP, Oracle, Salesforce. Prior Labs fills this gap with an approach that large generalist models do not cover — and SAP knows this, to the point of freezing recruitment and travel to fund the AI push.

Eighteen months of existence, nine million raised, a billion-euro acquisition: the multiplier is less about revenue than about the rarity of a skill that SAP could not rebuild internally in time. This is a strategic acquisition, not a revenue acquisition.

For European executive teams: this is one of the rare recent acquisitions where a European software champion buys a cutting-edge European laboratory and keeps it open, publishing, and independent. The strategic signal is as valuable as the deal itself.

CVC DIF Acquires EcoEridania: The Green Annuity at €1.1 Billion

CVC DIF, the infrastructure arm of the CVC Capital group, is signing the acquisition of a majority stake in EcoEridania, a leading Italian special waste management company, for a valuation exceeding €1.1 billion. The seller is iCon Infrastructure. More than twenty international investors were in the running; the final round pitted CVC DIF against Ardian and Swiss Life Asset Managers.

Industrial and special waste management presents exactly the profile that infrastructure funds seek: long-term contracts, regulated or quasi-regulated revenues, structurally growing demand driven by traceability and depollution obligations, and a regulatory barrier to entry that makes competition difficult. EcoEridania is not a growth story — it is a story of sustainable annuity in a sector where regulation is the best bulwark against disruption.

Mollie Raises €350 Million to "Not Build a Superapp"

Mollie, the Dutch payment fintech, announces a €350 million European expansion plan. The title of the Sifted article quotes the CEO: "Superapp is a convoluted word" — in other words, the company explicitly rejects the temptation to aggregate all financial services under one roof, a strategy attempted by Revolut, N26, and others.

The clarity of positioning here is the signal: in a market where generalist fintechs are fighting on all fronts with rising acquisition costs, Mollie bets that depth in SME payments is worth more than breadth. This is a choice of discipline as much as strategy.

Volati Acquires Tramex: Humidity Measurement as an Add-on

Source: finanznachrichten.de →

The Swedish industrial conglomerate Volati is acquiring Tramex, an Irish manufacturer of professional moisture meters founded in 1974, for approximately €51 million. The transaction is the first add-on for Corroventa, Volati's platform specializing in water damage drying. Tramex generates approximately SEK 90 million in annual revenue with an adjusted EBITA margin of around 20%.

The integration is logical: Corroventa dries, Tramex measures. Both products target the same customers — disaster restoration companies, building inspectors, construction companies. A pure technical complementarity add-on, without market risk: Tramex's margin mechanically improves the platform's consolidated profile.

Hexawin Joins a Build-up Group

Source: cfnews.net → · Sector FinTech — 📬 subscribe to the FinTech newsletter

Hexawin, an IT service provider based in Vitrolles offering cloud hosting and IT services to SMEs, becomes the fourth acquisition of the group formed by a family office, for €35 million. This is a classic sectoral consolidation operation in digital services for SMEs, a segment that remains highly fragmented in France.

Baker Tilly Absorbs Corex in Hauts-de-France

Source: lejournaldesentreprises.com →

Baker Tilly France (€219 million in revenue, 2,200 employees) is acquiring Corex, an accounting firm established in Saint-André-lez-Lille since 1958, for approximately €17 million. Corex employs 48 people, 8 partners, serves 2,300 clients, and generated €7.5 million in revenue in its last fiscal year. The transaction creates a new regional territory for Baker Tilly in Hauts-de-France, as part of its Convergence 2030 plan aiming for €400 million in revenue within four years.

The consolidation of accounting expertise follows a well-established mechanism: independent regional firms struggle to invest alone in the digital tools, CSR, and wealth management advice that SME clients are beginning to demand. Baker Tilly provides the range of services, Corex provides local roots and a client base. Nothing unexpected — but this is precisely the type of acquisition that builds a mid-sized professional services firm over ten years.

Audensiel Establishes Presence in Occitanie via iTekway

Source: lalettrem.fr → · Sector Mobility & Transportation — 📬 subscribe to the Mobility & Transportation newsletter

Audensiel, a Parisian consulting and digital services group (3,500 employees, €350 million in revenue targeted in 2026), is acquiring the Efis group — which includes iTekway Occitanie and iTekway Île-de-France — for €8 million. The two entities employ approximately 100 people, 75% of whom are consultants with disabilities, and generate over €5 million in revenue. The Impact Partners fund is exiting the capital.

The operation combines two logics: a strategic establishment in Toulouse's aerospace and space sector, and the strengthening of an inclusive employment policy that is becoming a criterion for accessing large corporate markets. For Audensiel, iTekway is not just a revenue acquisition — it is a commercial differentiation asset in tenders where ESG criteria carry weight.

Gruppo Peppe: An LBO Without a Sponsor Fund

Source: cfnews.net → · Sector FinTech — 📬 subscribe to the FinTech newsletter

Gruppo Peppe, a young Parisian group of Neapolitan pizzerias with €20 million in revenue, is opening its capital to a sector-specific fund as part of a sponsorless LBO, for approximately €35 million. A sponsorless LBO — without a traditional private equity fund at the helm — is a structure that gives founders more operational freedom while providing them with growth debt. In the restaurant industry, where cycles are short and decisions are quick, this is often a better fit than an institutional sponsor.

France-Germany vs. China: A Common Trade Roadmap

According to Les Échos, France and Germany are preparing a common roadmap to coordinate their response to Chinese trade practices. No financial operation here, but a signal of regulatory and geopolitical framework: for companies exposed to Chinese competition — industrial equipment, chemicals, batteries, electric vehicles — Franco-German coordination, if it materializes, could alter the conditions of access to the European market for Chinese products. To be watched by anyone arbitrating between Asian sourcing and local production.

Danske Bank Explores Significant Risk Transfers

Source: x.com → · Sector Horizontal & Productivity SaaS — 📬 subscribe to the Horizontal & Productivity SaaS newsletter

Danske Bank is evaluating Significant Risk Transfer (SRT) operations to free up regulatory capital, joining a broader movement among European banks. These instruments allow the transfer of credit risk from a loan portfolio to third-party investors, without divesting ownership. For alternative credit funds and insurers seeking yield on bank-quality assets, this is a window to access exposures that do not go through the traditional bond market.

All of today's M&A, by sector

The full list for today — including the deals decoded above.

B2B Software & Cloud · 4 →

- iTekway — Audensiel acquiert iTekway (conseil numérique, Occitanie) pour s'implanter en région

- Bankers ICT — ILC-Europe (Riverdam) acquiert Bankers ICT pour étendre les services IT à Eindhoven

- Hexawin — Hexawin gagne un acquéreur en phase de build-up

- Corex — Baker Tilly se renforce dans les Hauts-de-France avec le rachat de Corex

Biotech & Pharma · 2 →

- AtaiBeckley — Lilly acquiert AtaiBeckley (biotech, Europe) pour jusqu'à 3,8 Md$

- Catalyst Pharmaceuticals — Angelini Pharma finalise l'acquisition de Catalyst Pharmaceuticals (USA)

FinTech · 2 →

- additiv — Temenos finalise l'acquisition d'additiv (technologie bancaire, Suisse)

- Acasi — Qonto rachète Acasi (logiciel comptabilité, France) pour renforcer son offre

Industrial Tech & Manufacturing · 2 →

- Batibig — Charterhouse reprend Batibig (maintenance bâtiments, France) auprès de Siparex et EMZ

- Tramex — Volati acquiert Tramex (tech industrielle, Suède)

Mobility & Transportation · 2 →

- Rail Europe — Omio Group acquiert Rail Europe pour créer un géant mondial du voyage ferroviaire

- Delivery Hero — Uber acquiert Delivery Hero pour 13 Md€, plateforme dans 99 pays🔮 The next move: Just Eat Takeaway.com — the acquirer seeks to consolidate its position as a global delivery leader after the integration of Delivery Hero · GrabFood — Their strong presence in Southeast Asia would extend their geographical reach post-Delivery Hero · hypothesis, not a fact

Climate & Energy Tech · 1 →

- Junkbusters — Seenons acquiert Junkbusters pour renforcer la gestion circulaire des déchets en Europe

Construction & PropTech · 1 →

- ONE EXPERIENCE — ONE EXPERIENCE acquiert un hôtel Première Classe de 72 chambres à Vannes

Cybersecurity · 1 →

- SaycurIT — SNS Security rachète SaycurIT (conseil cybersécurité, Île-de-France)

D2C & Consumer Brands · 1 →

- Alinéa — Alinéa rachetée par MH France (groupe chinois Aosom), reprise officielle 13 juillet 2026

Data & Analytics · 1 →

- Prior Labs — SAP acquiert Prior Labs (modèles IA tabulaires, Allemagne) pour 1 Md€+

Developer & IT Infrastructure · 1 →

- Oupi — Oupi Technologies développe un OS pour rendre l'IA souveraine et responsable

Food & AgTech · 1 →

- Gruppo Peppe — Gruppo Peppe enfourne un LBO sponsorless

Future of Work & HR Tech · 1 →

- HR Path — HR Path poursuit sa stratégie d'agrégation avec une acquisition par mois

Gaming · 1 →

- Micromania — Micromania reprise par un consortium franco-québécois, 300 magasins et 1200 emplois sauvés

HealthTech & Digital Health · 1 →

- Pflegia — Ardian Growth rachète Pflegia (plateforme IA santé, Allemagne) via LBO

Logistics & Supply Chain · 1 →

- Ecoeridania — Cvc Dif rachète Ecoeridania (gestion des déchets, Italie) pour 1,1 Md€

Social & Creator Economy · 1 →

- InterNations — FairCap acquiert InterNations en carve-out de New Work SE

Space Tech · 1 →

- QPerfect — BTQ rachète QPerfect (R&D quantique, France) et installe son pôle européen à Strasbourg

🚀 Fundraisings today · 18

In focus — the deals we decoded

Mistral and EQT: European Private Equity Enters the Race for Large Models

EQT is reportedly in negotiations to lead or co-lead Mistral AI's Series D through its €5 billion Scaleup Europe fund, according to sources cited by ONE.WORKS. The financial details of the round remain partially obscured in the source, but the dynamic is clear: Mistral, already valued at around $6 billion during its Series C, would attract a leading European buyout player as a lead investor in a growth round.

EQT's entry — a fund whose culture is control, operational optimization, and defined-horizon exit — into the capital of a generative AI laboratory is a signal of the sector's maturity as much as a structural anomaly. Large language models have colossal infrastructure costs, fierce global competition, and still uncertain revenue trajectories. This is not the usual profile of an EQT investment.

What is at stake here goes beyond Mistral: if EQT validates this round, it means that European private equity is beginning to treat sovereign AI laboratories as strategic infrastructures — assets to be protected as much as to be made profitable. The logic is no longer just financial, it is geopolitical.

Syntetica: Brands Fund Their Own Material Supplier

Source: renseignementeconomique.fr →

Syntetica, a French deeptech company specializing in textile nylon recycling based in Reims, raises $30 million (approximately €28 million) in Series A. The round is led by Bpifrance via its Ecotechnologies 2 fund (France 2030), with EQT Ventures, SWEN Capital Partners, Lululemon, MAS Holdings, and the family offices of Peugeot, Etam, and the largest shareholder of Indorama Ventures. The European Innovation Council also provides equity and grants. The money will fund the construction of a first commercial demonstration plant in France.

The composition of the round is worth noting. Lululemon, Etam, and MAS Holdings are not just financial investors: they are potential customers, or more precisely, companies that have a problem that Syntetica claims to solve. Recycled nylon still accounts for about 2% of the global market (according to figures cited by the company, based on Textile Exchange); almost all nylon textile waste ends up incinerated or in landfills. The technical reason: Nylon 6 and Nylon 6,6 — the two dominant grades — mix in waste and are difficult to separate. Syntetica claims to be able to recycle both simultaneously, at low temperatures, leaving the elastane present in mixtures intact.

By investing, Lululemon and Etam are not making a philanthropic bet: they are securing a future supply of virgin-quality recycled material, while funding the infrastructure that will make it possible. This is upstream integration disguised as impact investment — and it is probably the only way to bring this type of industrial asset to fruition in Europe.

For a French industrialist or investor: the "brands in the recycler's capital" model is exportable to other materials (polyester, cotton, wool). Syntetica sets the precedent.

Stoïk: SME Cyber Insurance Moves to Series C

Source: globalsecuritymag.com → · Sector Cybersecurity — 📬 subscribe to the Cybersecurity newsletter

Stoïk closes €20 million in Series C. The round is led by Impala (Veyrat family), a new investor, with Opera Tech Ventures and existing investors Alven and Andreessen Horowitz. The company now protects over 10,000 businesses, collaborates with over 2,000 broker partners, covers over 600 new businesses per month, and closed 2025 with over 200% annual growth, for nearly €50 million in gross written premiums.

Stoïk has built a model that few players have successfully assembled: cyber insurance, proactive prevention, and an incident response team under one roof, targeting SMEs — a segment that large insurers handle poorly because it is costly to address individually. Impala's entry, a long-term family shareholder, alongside a16z, is a signal of credibility as much as capital. At €50 million in premiums, Stoïk is no longer a startup — it is a specialized insurer in the industrialization phase.

Forsee Power: Refinancing Under Pressure

Forsee Power, a French manufacturer of battery systems for sustainable mobility, announces a capital increase of €20 million led by FCAP Investors (a Singaporean fund) with the participation of Eurazeo, an existing reference shareholder. The operation is subject to prior authorization from the Ministry of Economy under foreign investment control.

The press release speaks of a "demanding market environment" and an operation aimed at "strengthening equity." This vocabulary, in the world of finance, does not describe serene growth: it describes a company that needs to strengthen its balance sheet to stay on course with its strategic plan in a sustainable mobility battery market that has slowed faster than anticipated — between cost pressure, delays in electric fleet deployment, and Asian price competition. The entry of a Singaporean fund like FCAP, subject to French regulatory scrutiny, highlights that strategic assets of the energy transition remain under surveillance — even when they are seeking emergency capital.

Wheere: Locating Where GPS Doesn't Reach

Source: journaldugeek.com → · Sector Mobility & Transportation — 📬 subscribe to the Mobility & Transportation newsletter

Wheere, a Montpellier-based startup founded in 2020, raises €8.5 million, bringing its total raised to approximately €20 million since its inception. The company develops indoor and underground geolocation technology based on low-frequency VHF radio waves, capable of locating a person or object through up to 50 meters of concrete with sub-meter accuracy, using only four antennas per square kilometer.

The target applications are industrial and defense: tracking isolated workers, traceability of hospital equipment, coordination of rescue efforts in collapsed buildings, navigation in GPS jamming zones. In a context where GPS jamming has become a common tactic in conflict zones and the resilience of navigation systems is a defense priority, Wheere addresses a need that did not exist as a market five years ago.

SWISSto12: Smaller GEO Satellites, Bigger Raise

SWISSto12, a Swiss space startup, closes a $70 million (approximately €64 million) Series C, bringing its total raised to over $100 million. The company had also secured an additional $73 million through the ESA HummingSat program in January 2026. It reports $140 million in revenue in 2025 and an order book exceeding $500 million, with commitments from SES and Viasat.

SWISSto12 builds small geostationary satellites — a breakthrough in a segment where GEO satellites traditionally weighed several tons and cost hundreds of millions. The combination of a solid order book, ESA support, and a private Series C outlines a European space player that has moved beyond the demonstration stage. With $500 million in orders in its portfolio, the question is no longer technology — it is production capacity, which this round precisely funds.

microagi: Germany's Largest Seed Round Ever, Funded by Human Data

microagi, a Munich-based startup founded by Bercan Kilic — former aerodynamic engineer at Red Bull Racing F1 — raises $55 million (approximately €51 million) in a seed round, the largest ever for a German startup at this stage. The round is led by Hummingbird, with Northzone, LocalGlobe, Village Global, and redalpine.

microagi builds neither robots nor proprietary foundational models. Its bet is elsewhere: factories already have robots, but these robots do not know how to execute the precise and variable gestures required for real production. microagi collects human movement data — through its Shift program, which pays over 20,000 people in 15 countries to record their physical gestures — and trains models that allow existing robots to be reprogrammed.

The logic is that of human labor as training raw material: tens of thousands of people perform gestures for remuneration, these gestures become data, this data becomes robotic competence. This is a new form of outsourcing of worker know-how — no longer to low-cost countries, but to models that permanently absorb it. The paradox is clear: humans are paid to teach machines to replace humans.

For French industrialists: microagi does not sell robots; it sells adaptability for the robots you already have. This is a model that directly addresses manufacturing SMEs with heterogeneous lines that cannot afford custom robotic integration.

Greenjets: Green Propulsion with NATO Stamp

Source: eu-startups.com → · Sector Industrial Tech & Manufacturing — 📬 subscribe to the Industrial Tech & Manufacturing newsletter

Greenjets, a London-based aerospace startup founded in 2022, raises €35 million in Series A. The round is led by Blossom Capital, with the NATO Innovation Fund (NIF), the National Security Strategic Investment Fund (NSSIF), and existing investors including Tanglin Ventures.

Greenjets develops propulsion architectures covering electric ducted fans to geared turbofans, with a stated goal of reducing certification costs. The simultaneous presence of the NATO Innovation Fund and the NSSIF in the round is the clearest signal: advanced aerospace propulsion is treated as a defense capability as much as a civilian technology. This is no longer a classic aerospace deep tech round — it is industrial sovereignty funding in the propulsion sector, with national security institutions as co-investors.

Isometric: Certifying Industry at AI Scale

Isometric, a London-based startup founded in 2022 by Eamon Jubbawy (co-founder of Onfido), raises €34 million in Series A. The round is led by AVP, with Lowercarbon Capital, Plural, and business angels John Doerr and Walter Kortschak.

Isometric began as a carbon capture project verification platform — it has already certified over 16 million tons for Microsoft, JPMorgan Chase, Anglo American, and Boeing. With this raise, it is expanding its scope to industrial certification in a broader sense: compliance, safety, sustainability standards, in a market estimated at approximately €305 billion. Its Certify platform ingests millions of data points — satellite imagery, sensors — to detect anomalies and direct high-risk cases to human experts.

The model is that of augmented auditing: AI handles volume, humans decide on borderline cases. In a sector where certification is a bottleneck for any industrial or energy project, reducing verification time without compromising regulatory rigor is a directly monetizable value proposition.

📩 Subscribe to our newsletter to follow daily M&A and fundraising news: https://proplace.co/newsletter

All of today's fundraisings, by sector

The full list for today — including the deals decoded above.

Climate & Energy Tech · 6 →

- Greenjets — Greenjets lève 35 M€ en Série A pour sa technologie aérospatiale verte

- VARM — VARM lève 17,5 M€ en Série A pour son plateforme d'isolation thermique résidentielle

- Syntetica — Syntetica lève 30 M$ pour industrialiser le recyclage du nylon en France

- Porelio — Porelio lève 2,4 M€ en pré-seed pour ses matériaux avancés de traitement de l'eau

- Forsee Power — Forsee Power bénéficie d'un refinancement mené par FCAP Investors et Eurazeo

- Visibuilt — Visibuilt lève 3,34 M€ en seed pour ses liants biosourcés pour la construction

Mobility & Transportation · 2 →

- Wheere — Wheere lève 8,5 M€ pour son GPS fonctionnant sous terre et en bâtiments fermés

- A Former Red Bull F1 Engineer Just Raised Germany's Biggest Seed Round Ever - Startup Fortune

B2B Software & Cloud · 1 →

- Mistral — Mistral en discussions avec le fonds EQT pour une levée majeure

Biotech & Pharma · 1 →

- Sightera Biosciences — Sightera Biosciences lève 3 M€ en pré-seed pour sa plateforme IA de découverte de médicaments

Cybersecurity · 1 →

- Stoïk — Stoïk lève 20 M€ en Série C menée par Impala et Opera Tech Ventures

FinTech · 1 →

- PARIS - In Extenso Finance In Extenso Finance Paris

Food & AgTech · 1 →

- Agripower — Agripower lève 0,6 M€ en placement privé pour son activité agricole

HealthTech & Digital Health · 1 →

- Womed — Womed lève plus de 7 M€ pour sa plateforme de santé utérine

Industrial Tech & Manufacturing · 1 →

- Isometric — Isometric lève 34 M€ en Série A pour sa plateforme IA de certification industrielle

RegTech & Compliance · 1 →

- Naaia — Naaia lève 6 M€ pour la conformité à l'AI Act européen

Space Tech · 1 →

- SWISSto12 — SWISSto12 lève 70 M$ en Série C pour développer des petits satellites géostationnaires

The Physical World · 1 →

- Engo — Engo lève 5,1 M€ pour miniaturiser ses lunettes connectées