Analysis of the day

Analysis of M&A & Fundraising Deals on July 17, 2026

Uber rewrites the global delivery map, Vinci Energies swallows a German SAP integrator, and European deep tech — robots, lasers, circular nylon, semiconductors — captures increasing investor attention: today's overview for decision-makers and investors.

· Proplace

🌐 Translated from the French original by AI — the French version is authoritative.

📊 Today's pulse — 38 deals · 21 M&A · 17 fundraisings · €31.9bn in play.

A two-speed day. On the major maneuvers front, Uber attempts one of the most structuring acquisitions in the European digital economy in years, while Vinci Energies discreetly acquires a foothold in German SAP integration. On the fundraising side, continental deep tech — industrial robotics, material recycling, power semiconductors, sovereign cyber defense, satellites — absorbs significant tickets, a sign that institutional capital is seeking positions in assets that resist software replication. Here's the essential decoded.

🤝 Mergers & acquisitions today · 21

In focus — the deals we decoded

Uber–Delivery Hero: When the Platform Becomes Global Infrastructure

Source: boursorama.com → · Sector Mobility & Transportation — 📬 subscribe to the Mobility & Transportation newsletter

Uber has officially announced the acquisition of Delivery Hero for approximately €13 to €14.8 billion (depending on the exchange rate used) — an all-stock transaction that would make Uber the leading delivery operator outside of China, present in 99 countries. Delivery Hero, of which Uber was already the largest shareholder, is also divesting its operations in 14 overlapping markets to SSW Partners for approximately €1.4 billion. Management recommends the offer of €41.50 per share; closing is expected in the second half of 2027, subject to competition authorities.

The surface reading: Uber consolidates global delivery, doubles its geographic footprint, and establishes a lasting presence in South Korea, Saudi Arabia, Italy, and Argentina.

What deserves attention is the very structure of the operation. Uber is paying in shares, not cash — meaning Delivery Hero shareholders become Uber shareholders, and Uber is not spending a single cent of cash to double in size. This is a sign of a platform that has understood that its most powerful currency is its own stock. The real bet is not food delivery: it's the densification of the urban logistics network — couriers, merchants, traffic data — that makes the platform almost mandatory for anyone who wants to distribute anything in the city. The prior divestment of the 14 overlapping markets to SSW Partners is surgical: Uber doesn't want mass, it wants the geographies where it wasn't yet the dominant operator. For a French or European group operating in local distribution, fast food, or last-mile logistics, this consolidation further reduces the negotiation space with platforms — and accelerates reflection on what data they are giving up in exchange for visibility.

Vinci Energies / All for One: SAP Integration as Digital Infrastructure

Vinci Energies is launching a tender offer for All for One, an SAP integrator listed in Frankfurt, for €338 million — or €67.50 per share, a premium of 95.5% over the last closing price. All for One employs 3,000 people and aims for revenues of €500 to €530 million in its current fiscal year, but without operating profit after a difficult first half.

The immediate reading: Vinci Energies, a subsidiary of Vinci, strengthens its presence in digital infrastructure services by acquiring a specialist in business application integration and maintenance.

The 95% premium on a stock without operating profit is the striking figure. Vinci Energies is not paying for today's profits — it's paying for a position. All for One is a leading SAP integrator in the German-speaking region, with captive industrial clients whose migration cycles to SAP S/4HANA span ten to fifteen years. In a digital transformation market where customer relationship is the real asset, an installed base of 3,000 German and Austrian companies is well worth a control premium. Vinci Energies is thus transforming a technical services subsidiary into a player in the transformation of industrial information systems on a European scale — a very different positioning from that of a classic IT service provider. For a French acquirer seeking to grow in Germany in consulting or systems integration, this operation sets a new valuation floor for established SAP integrators.

IPG Photonics Acquires Lumibird Medical: Medical Laser Division Changes Hands

Source: aseangazette.com → · Sector HealthTech & Digital Health — 📬 subscribe to the HealthTech & Digital Health newsletter

IPG Photonics Corporation (Nasdaq), an American specialist in high-power lasers, has made a firm offer to acquire the medical division of Lumibird for €920 million. Lumibird, listed in Paris, retains its industrial and defense laser activities. The divested medical division notably covers ophthalmic lasers.

This divestment is not a retreat — it's a strategic clarification. Lumibird has grown through successive acquisitions in two very different worlds: industrial physics and medicine. The two have R&D cycles, regulations, and customers that have almost nothing in common. By divesting the medical division to an American player for whom it is a primary growth axis, Lumibird recovers a considerable amount relative to its market capitalization and can concentrate its resources on industrial and defense lasers — a market in strong demand in Europe in the current context. IPG, for its part, acquires a regulatory and commercial platform in Europe, which would have taken it a decade to build alone. For investors in listed French industrial stocks, the transaction illustrates how a conglomerate split can create more value than the sum of the parts held together.

Micromania: A Historic Brand Acquired by a Franco-Quebecois Consortium

GameStop is divesting Micromania-Zing, its French video game retail chain founded in 1983, to a consortium led by Canadian entrepreneur Stephan Tétrault, alongside Jean-François Chenail and the couple Sandra and Stephen Callahan. The amount has not been officially disclosed — GameStop acquired Micromania in 2008 for approximately $700 million, an equivalent amount in euros at the time.

The context is brutal: Sony plans to stop PlayStation disc games from January 2028, and the market is shifting towards digital downloads. The question is not whether the historical model of the physical game store will survive — it will not survive as is. The question is whether a brand with 600 points of sale and a loyal customer base can transform into something else: community, events, accessories, second-hand, gaming café.

The bet of the Franco-Quebecois consortium is precisely that: not to defend the disc, but to retain the customer relationship to redirect it. It's a bet on the brand more than on the existing business model. If the plan fails, the residual asset (commercial leases, customer database) remains salable. If the plan succeeds, Micromania becomes something new with a historically low customer acquisition cost. For an investor in specialized physical retail, this is a textbook case on the residual value of a brand in a media transition.

Omio Acquires Rail Europe: Global Rail Distribution Consolidates

Omio Group, the Berlin-based multimodal booking scale-up, has announced the acquisition of Rail Europe, a French rail distribution platform founded over 90 years ago, for €84 million. Rail Europe joins the Omio ecosystem, which already includes a B2C platform, a B2B activity, and the travel discovery brand Rome2Rio.

Rail Europe is a distribution infrastructure: tariff agreements with dozens of global rail operators, a clientele of agencies and resellers, and institutional legitimacy built over nine decades. What Omio is acquiring is the portfolio of commercial agreements — impossible to replicate quickly — more than technology. By combining Rail Europe's B2B coverage with its own B2C interface, Omio is giving itself the means to become the essential gateway between rail operators and international travelers, in a market where demand for long-distance train travel is structurally increasing. For French rail operators (SNCF at the forefront), this consolidation of third-party distributors raises the question of tariff control and direct customer relationships.

PayFit: Profitability as a Starting Point, Not a Destination

PayFit simultaneously announces reaching profitability for the first time since its creation in 2015, and a major evolution in its positioning: the French payroll management unicorn is becoming a global HR platform. The stated objective is €150 million in ARR by the end of 2028. New modules are announced for 2026: mutual health and provident fund management, equipment tracking, integration of non-salaried workers.

This announcement is classified as M&A in the feed because it is accompanied by a secondary financing operation (share buyback), but the essential part is strategic.

The real news is not profitability — it's what it enables. PayFit is freed from the constraint of permanent external financing and can now finance its scope expansion through its own cash generation. The addition of freelancers as a managed population is the most interesting signal: it recognizes that classic salaried work is no longer the sole basic unit of HR, and that the platform that captures the management of mixed workforce (employees + independent contractors) will have a structural advantage over players who remain solely within the scope of the employment contract. For a CEO of a French SME or mid-cap company, PayFit is starting to look like a complete HR infrastructure rather than an improved payroll software — which changes the nature of the adoption decision.

Duranet Acquires Renaudin Propreté: Territorial Expansion in Industrial Cleaning

Source: lejournaldesentreprises.com →

Duranet Groupe, an industrial cleaning player based in Creil (Oise), acquires Renaudin Propreté, a Reims-based company with 26 employees and €1.3 million in revenue, founded in 1992. Amount undisclosed. Duranet thus increases its workforce to over 380 people, maintains nearly 600 sites, and establishes itself in the Grand Est region.

A classic external growth operation in a fragmented sector where geographic density is a direct competitive advantage: the closer to customers, the lower travel costs and the higher responsiveness. Nothing else to read here than a disciplined execution of a regional consolidation strategy.

All of today's M&A, by sector

The full list for today — including the deals decoded above.

B2B Software & Cloud · 3 →

- Shaped — Whatnot rachète Shaped pour l'IA du live shopping

- Trifork Group — Verdane acquiert un portefeuille d'activités technologiques de Trifork Group

- All for One — Vinci Energies rachète All for One pour 338 M€

Construction & PropTech · 3 →

- Izimmo — BPCE se renforce dans l'immobilier avec l'acquisition d'Izimmo et Liberkeys

- Bidault Bâtiment — Aurélien Le Borgne rachète les parts de Bidault Bâtiment

- KRATA — RYZE acquiert KRATA et entre sur le marché immobilier espagnol

Industrial Tech & Manufacturing · 2 →

- Phea — Hexalean renforce son offre industrielle avec l'acquisition du groupe Phea

- Rotork — ABB acquiert Rotork pour élargir son offre d'automatisation

MedTech & Devices · 2 →

- Primed Group — Inflexion acquiert Primed Group, spécialiste allemand des consommables médicaux

- Lumibird — IPG Photonics annonce une offre contraignante pour acquérir Lumibird Medical

Biotech & Pharma · 1 →

- Recordati — CVC propose une offre de retrait de 10,7 milliards d'euros pour Recordati

Commerce & Consumer · 1 →

- Delivery Hero — Uber acquiert Delivery Hero pour 13 milliards d'euros🔮 The next move: iFood — Their strong presence in Latin America would consolidate their global expansion post-Delivery Hero, especially in emerging markets · hypothesis, not a fact

Developer & IT Infrastructure · 1 →

- Lynx — EssilorLuxottica acquiert Lynx, startup française de matériel XR

Future of Work & HR Tech · 1 →

- PayFit — PayFit annonce sa rentabilité et son pivot vers plateforme RH

Health & Wellness · 1 →

- Orange-Sheep — Healthcare Brands Group acquiert Orange-Sheep pour élargir son portefeuille durable

HealthTech & Digital Health · 1 →

- GBA — Bridgepoint acquiert une participation majoritaire dans GBA, laboratoire allemand

Logistics & Supply Chain · 1 →

- Renaudin Propreté — Duranet s'implante dans le Grand Est avec le rachat de Renaudin Propreté

Mobility & Transportation · 1 →

- Rail Europe — Omio acquiert Rail Europe dans un accord majeur de distribution ferroviaire

Retail & E-commerce Tech · 1 →

- Micromania — Micromania-Zing sauvé par une alliance franco-québécoise

WealthTech & Asset Management · 1 →

- Ardian — Axa sort du capital d'Ardian au profit des Assurances du Crédit Mutuel et Wafra

Other deals (sector not classified) · 1

- M&A PME 2026 : volumes, multiples et perspectives

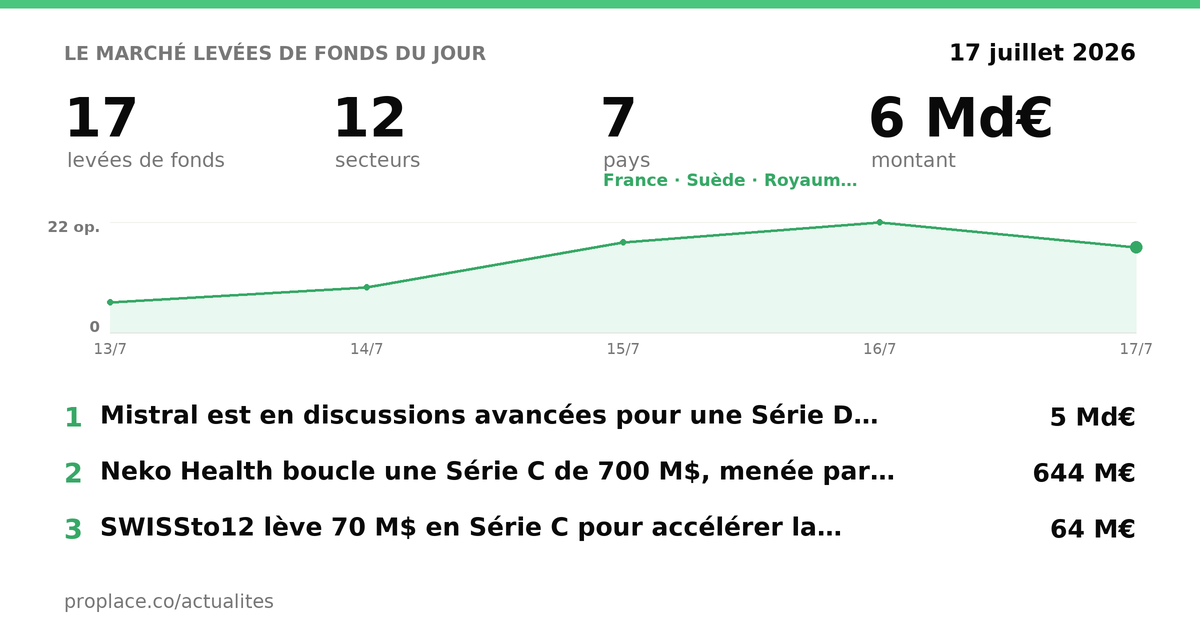

🚀 Fundraisings today · 17

In focus — the deals we decoded

EQT / Mistral: European Capital Bets on its AI Champion

EQT is in advanced discussions to lead or co-lead the Series D of Mistral, the French generative AI startup founded in 2023, via its Scaleup Europe fund with €5 billion. Mistral's valuation would reach €6.1 billion according to sources, compared to €2.9 billion in the previous round. Nvidia and Salesforce could re-participate. Mistral has already raised over €1 billion in total.

The obvious reading: EQT validates Mistral as the European champion in generative AI and provides it with the means to compete with American giants.

What is less obvious is EQT's profile in this operation. EQT is not a classic venture fund — it is a growth equity and buyout player that typically invests between €50 and €100 million per ticket, in companies that already have an established revenue trajectory. Its entry into Mistral's capital signals that the startup has crossed a threshold: it is no longer a technological gamble, it is an infrastructure under construction. Mistral's revenues would exceed $400 million annualized according to sources. At this level, the investor profile changes — it moves from the VC who finances hope to the institutional fund that finances the ramp-up of an already real player. For a French executive who uses or plans to use AI models in production, Mistral's increasing capitalization is a guarantee of service continuity — and an argument for not depending exclusively on American models.

Neko Health: $700 Million to Scan the Human Body at Scale

Source: france-jeunes.net → · Sector HealthTech & Digital Health — 📬 subscribe to the HealthTech & Digital Health newsletter

Neko Health, the Swedish MedTech co-founded by Daniel Ek (Spotify creator) and Hjalmar Nilsonne, closes a $700 million Series C (€644 million), bringing its valuation well over a billion. The round is led by Lightspeed Venture Partners and O.G. Venture Partners, with participation from Atomico, General Catalyst, Lakestar, and personalities such as Mark Zuckerberg, Thierry Henry, and Maria Sharapova. Total raised: over $1 billion.

Neko Health designs its own body scanners, analysis software, and clinics — a complete vertical integration in preventive medicine.

The amount is comparable to what generative AI labs raise, for a company that performs health check-ups. The key is vertical integration: Neko does not resell an existing medical service, it controls the entire chain — the scanning hardware, the analysis algorithm, the patient relationship, the longitudinal data. It is the latter that is the real asset: a database of human bodies scanned at regular intervals, over years, is one of the rarest and most valuable medical datasets that can exist. Each new patient strengthens the model; each additional scan on an existing patient increases predictive value. The celebrities in the cap table are not decoration — they are distribution ambassadors in wealthy customer segments that are difficult to reach through traditional advertising. For an investor in digital health, Neko raises the question of whether premium preventive medicine can become a mass market — or if it will remain an elite service with high margins.

SWISSto12: $70 Million for 3D-Printed Satellites

SWISSto12, a Swiss startup specializing in satellite platforms and payload technologies manufactured by 3D printing, raises $70 million (€64 million) in Series C to develop its multi-orbit business and meet growing commercial and governmental demand.

SWISSto12 manufactures RF (radio frequency) components and entire satellites with a much higher functional density than conventional processes allow, at reduced costs and lead times. In a space market where deployment speed has become as important a competitive advantage as technical performance, the ability to quickly manufacture custom satellites positions SWISSto12 as a critical supplier for constellation operators — a structurally growing market. For an investor in European deep tech, this is a niche player with high barriers to entry in a strategic sector.

Eye Security: €60 Million for Sovereign Cyber Defense… Funded by Americans

Source: siliconcanals.com → · Sector The Physical World — 📬 subscribe to the The Physical World newsletter

Eye Security, a Dutch startup founded by former Dutch intelligence agents, raises €60 million to build a European "sovereign" cyber defense offering for SMEs and mid-cap companies. Two of its investors are American.

The tension is there, in the press release itself: a company positioning itself on European digital sovereignty and raising funds from American funds. This is not necessarily a contradiction — capital has no nationality, and American funds readily invest in European players who capture local regulatory demand (NIS2, DORA). But for customers who choose Eye Security precisely to avoid American dependence, the capital structure deserves to be clearly stated. For a CIO of a French mid-cap company seeking a managed cybersecurity solution compliant with European regulatory requirements, the question of effective control of the asset remains relevant beyond the "sovereign" label.

Microagi: $55 Million to Teach Robots to Work in Factories

Source: sifted.eu → · Sector Industrial Tech & Manufacturing — 📬 subscribe to the Industrial Tech & Manufacturing newsletter

Microagi, a Munich-based startup founded ten months ago by Formula 1 engineers from Red Bull Racing and Mercedes-AMG Petronas, raises $55 million (€51 million) in what is announced as the largest seed round ever in Germany. The round is led by Hummingbird, with Northzone, LocalGlobe, Village Global, and Redalpine.

Microagi does not build robots. It collects data in factories and homes (its engineers wear head-mounted cameras to record real tasks), and uses this data to train and refine robotics models then deployed at its industrial clients. The hardware is purchased from Chinese manufacturers (Unitree, UBTech) and leased to factories.

The model is more subtle than it appears. Microagi has understood that in industrial robotics, the bottleneck is not the robot — it's the training data specific to each production environment. By setting up at client sites to collect this data, it creates a cumulative advantage: the more it deploys, the more precise its models, the more efficient its robots, the more new clients it attracts. The fact of buying its robots in China and injecting German software trained on New York data says something important about the real state of technological "decoupling": in physical robotics, international integration is still the norm, regardless of political statements. For a French industrial director evaluating the automation of their lines, Microagi represents a radically different approach from the classic large integrator — more agile, more data-driven, but still to be proven at scale.

Syntetica: $30 Million to Chemically Recycle Nylon

Syntetica, a startup based in Reims (Marne), closes a $30 million Series A (approximately €28 million) led by Bpifrance Green Venture, with participation from lululemon, Groupe Etam, MAS Holdings, SWEN Capital Partners, and the EIC (European Innovation Council). Founders Marco Bertone and Louis Monsigny had raised €4.2 million in November 2023, nine months after creation.

Syntetica has developed a green chemistry process that allows simultaneous recycling of different types of nylon without additional cost, to produce virgin-quality nylon. The funds will finance the doubling of staff and a commercial demonstration unit within the Michelin Innovation Park in Clermont-Ferrand.

What distinguishes this round is the composition of the investor syndicate. Lululemon, Etam, and MAS Holdings are not financiers — they are potential clients and players in the textile supply chain. Their presence in the capital transforms the fundraising into something closer to a future supply commitment than a simple financial bet. It is an industrial validation as much as a market validation: these groups do not put money into technology that does not interest them commercially. The establishment at the Michelin Innovation Park is also a strong signal — Michelin is one of the largest consumers of nylon in the world (tires contain significant quantities) and has an industrial infrastructure that few startups can hope to approach. For an investor in sustainable materials, Syntetica illustrates how a recycling technology can be financed by bringing its future buyers on board from the start — thus reducing commercial risk without waiting for large-scale demonstration.

AlpSemi: €17 Million for Smart Circuit Breakers in Data Centers

AlpSemi, a Grenoble-based startup specializing in semiconductor power switches, raises €17 million from Yotta Capital, SE Ventures (Schneider Electric's venture arm), Navitas Semiconductor, and Cycle Group. The funds are intended for the development of next-generation semiconductor circuit breakers for buildings and 800V DC AI data centers.

The presence of SE Ventures — Schneider Electric's fund — and Navitas Semiconductor (an American manufacturer of power semiconductors) in AlpSemi's capital is not insignificant. These are two players who have a direct industrial interest in the technology working and being deployed. 800V DC data centers are the emerging architecture for high-power density AI infrastructures — classic mechanical circuit breakers do not respond fast enough to the load variations generated by GPUs. AlpSemi addresses a concrete and growing problem, with potential clients who have already invested in the solution. For a data center operator or developer in France, AlpSemi is one to watch as a supplier of a critical component for next-generation electrical architectures.

Huard: MBI in Multi-Technical Building Services

Source: cfnews.net → · Sector FinTech — 📬 subscribe to the FinTech newsletter

Huard, a Paris region-based company providing multi-technical building services with €11 million in revenue, is acquired in an MBI (Management Buy-In) by a former TotalEnergies executive, with the support of a private equity fund. Amount undisclosed.

A classic business transfer operation for technical services via an experienced external acquirer. The acquirer's industrial profile (energy) suggests a development thesis in building energy efficiency services, a market driven by renovation obligations.

📩 Subscribe to our newsletter to follow daily M&A and fundraising news: https://proplace.co/newsletter

All of today's fundraisings, by sector

The full list for today — including the deals decoded above.

Climate & Energy Tech · 3 →

- VARM — VARM lève 17,5 M€ en série A pour l'isolation thermique

- Applied Computing — Applied Computing lève 17,4 M€ pour son IA énergie

- Syntetica — Syntetica lève 30 millions de dollars pour ses matériaux durables

Developer & IT Infrastructure · 3 →

- Valarian — Valarian lève 50 M$ pour son infrastructure IA souveraine

- AlpSemi — AlpSemi lève 17 millions d'euros pour ses interrupteurs d'alimentation nouvelle génération

- Arq — Arq lève 1,4 M$ en pre-seed pour l'internet quantique

B2B Software & Cloud · 2 →

- Marker — Marker lève 13 M$ en seed pour son éditeur IA collaboratif

- Mistral — EQT prêt à booster Mistral avec un fonds de 5 milliards d'euros

Robotics & Automation · 2 →

- Hyperion Robotics — Hyperion Robotics lève 7,4 M$ pour la construction robotisée

- Microagi — Microagi lève 55 M$ en seed, plus grand tour en Allemagne

Construction & PropTech · 1 →

- Visibuilt — Visibuilt lève 3,34 M€ en seed pour son liant biosourcé

Cybersecurity · 1 →

- Eye Security — Eye Security lève 60 M€ en série C pour la cyberdéfense souveraine

FinTech · 1 →

- Huard — Le courant passe entre Huard et un repreneur

HealthTech & Digital Health · 1 →

- Neko Health — Neko Health lève 700 millions de dollars en série C

Industrial Tech & Manufacturing · 1 →

- valuemize — valuemize lève sept chiffres en pre-seed pour la gestion des coûts

Logistics & Supply Chain · 1 →

- Stracker — Stracker lève 2,5 millions d'euros pour fluidifier le transport aérien d'urgence

Space Tech · 1 →

- SWISSto12 — SWISSto12 lève 70 M$ en série C pour son activité multi-orbite