Analysis of the day

M&A and Fundraising Analysis for July 19, 2026

From mixed reality to low-carbon cement, global delivery to space sovereignty: Europe acquires, consolidates, and raises capital—today's overview for decision-makers and investors.

· Proplace

🌐 Translated from the French original by AI — the French version is authoritative.

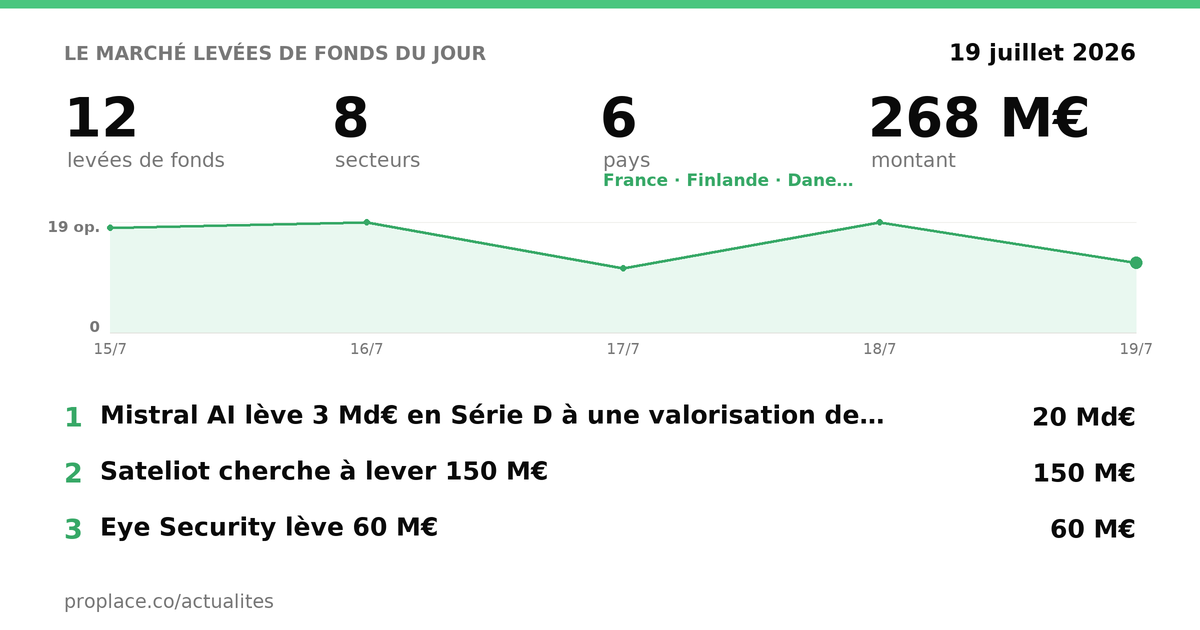

📊 Today's pulse — 30 deals · 17 M&A · 13 fundraisings · €34.3bn in play.

AI, infrastructure, and the consolidation of sectors under structural pressure dominate the day. In Europe, major maneuvers are playing out at different speeds: mega-deals reshaping entire markets alongside meticulously planned build-ups and fundraisings in construction materials or cybersecurity. France is not to be outdone—between LBOs, acquisitions of assets in liquidation, and early-stage venture capital, the flow is dense. Here's what really matters.

🤝 Mergers & acquisitions today · 17

In focus — the deals we decoded

Uber swallows Delivery Hero: when the platform becomes the market itself

Source: economiematin.fr → · Sector Mobility & Transportation — 📬 subscribe to the Mobility & Transportation newsletter

Uber announces the acquisition of Delivery Hero for €13 billion (approximately $14.8 billion), at €41.50 per share—a premium of approximately 34% over the three-month average preceding the announcement. The transaction, if approved by regulators, would bring the combined presence to 99 countries. In parallel, SSW Partners is acquiring Delivery Hero's assets in 14 markets where the two groups directly overlap, for approximately €1.4 billion—a preventive divestiture aimed at defusing antitrust objections even before the investigation begins.

The immediate interpretation: Uber is consolidating global delivery, eliminating a competitor, and buying geographical coverage. This is true, but incomplete.

What the operation reveals is the inherent logic of mature platforms. Uber already held 25% of Delivery Hero directly, plus 12% via financial instruments. Prosus, the largest shareholder with nearly 17%, has agreed to sell its entire position. This is not a classic acquisition: it's the closing of a cross-investment that had lasted for years, transformed into full control at a time when the delivery market is tightening. Delivery Hero was worth less than €20 at the beginning of the year—the premium paid today actually finances the orderly exit of its major shareholders as much as it finances Uber's strategy.

The real issue is not geographical coverage, it's data: 99 countries means a flow of food purchasing and mobility behaviors that no one else will possess on this scale—and this, more than cost synergies, justifies the price.

For a European delivery or fast-food player, the question is no longer whether Uber will dominate—that's a given in most markets—but how quickly it will impose its pricing conditions once the competition is absorbed.

SAP acquires Prior Labs: one billion for eighteen months of existence

SAP is acquiring Prior Labs for over one billion euros, eighteen months after the German startup's founding. Prior Labs has developed what are called tabular foundation models—AI trained once, capable of processing any corporate data table (churn prediction, supplier risk, payment delays) without specific reconfiguration for each dataset. Its flagship model, TabPFN, is already in use at Hitachi and TD.

The obvious interpretation: SAP is buying an AI building block that was missing from its ERP offering to remain credible against Salesforce, Oracle, and Microsoft.

But look at the structure of the operation. Prior Labs retains its brand, its management team, its research agenda, and will continue to publish its work and make its models accessible. SAP is not buying a product—it is buying a frontier research team and positioning it as an internal lab while allowing it to operate as an independent academic player. This is exactly what Google did with DeepMind in 2014: acquiring scientific credibility without killing it through integration.

One billion for eighteen months of existence is less a revenue valuation than a premium on scarcity: teams capable of building foundation models for structured enterprise data can be counted on one hand in Europe, and SAP has just locked one in.

For French CIOs and CFOs evaluating their forecasting tools: Prior Labs' tabular models are already in production at major international accounts. Integration into the SAP ecosystem will likely accelerate their availability—and their exit cost.

EssilorLuxottica acquires Lynx: intellectual property survives, the startup disappears

EssilorLuxottica is acquiring the assets of Lynx, a French mixed reality startup, following its judicial liquidation. The acquisition covers intellectual property, brand, code, databases, 3D design files, and industrial know-how. The majority of employees are joining EssilorLuxottica. Founder Stan Larroque is joining Parrot.

The amount is not disclosed—in the context of a judicial liquidation, it will likely be modest compared to the capital invested since its creation.

EssilorLuxottica already manufactures Ray-Ban Meta in partnership with Meta. It now owns the intellectual property of a direct competitor to Meta in mixed reality, as well as the teams that built it. The operation cannot be explained by immediate product logic: Lynx never managed to scale commercially.

What the Franco-Italian group is acquiring is a strategic option—the ability not to depend solely on Meta to define the next generation of connected glasses, at a time when this market is just beginning to emerge.

For the French deeptech ecosystem, the signal is more bitter: a startup that had raised funds, built recognized technology, and generated real European interest ends up being acquired in liquidation, its assets absorbed without value returning to the founders or initial investors. The technology survives, the company does not.

MDA Space takes control of CLS with CNES as reference shareholder

MDA Space, a Canadian space technology group, is acquiring a majority stake in CLS (Collecte Localisation Satellites), a subsidiary of CNES founded in 1986, specializing in Earth observation data analysis using artificial intelligence, present in 150 countries with approximately 1,200 employees. CNES remains the reference shareholder. The firm FTPA advised CNES on all legal aspects.

The operation brings together MDA Space's industrial and satellite capabilities—launchers, satellite manufacturing—with CLS's analytical and geospatial expertise. For CNES, it's about giving CLS the resources to accelerate internationally without losing its strategic French anchor.

The structure is well-calibrated: operational control passes to a private industrial player capable of investing, while sovereignty over terrestrial observation data remains protected by CNES's presence in the capital—a balance that few transactions in institutional space manage to achieve.

VINCI Energies launches a tender offer for All for One with a 95% premium

VINCI Energies, a subsidiary of VINCI (€75 billion in revenue, 120 countries), is launching a public tender offer for All for One Group SE, a listed German SAP integrator, at €67.50 per share—a premium of approximately 95.5% over the last closing price before the announcement, and approximately 105% over the weighted average of the last three months. All for One's management and supervisory boards support the operation.

VINCI Energies already owns Axians, its ICT brand. All for One is one of the leading SAP partners for the midmarket in Europe. The stated ambition: to create the European leader in end-to-end transformations for mid-sized companies, combining Axians' technical infrastructure and All for One's SAP application expertise.

A 95% premium for a listed company is the price of a position that VINCI cannot build organically—the client base, SAP certifications, and trained teams cannot be improvised. In a market where SAP is pushing its clients towards the S/4HANA cloud, owning the midmarket's reference integrator means capturing the migration rent for the next ten years.

Omio acquires Rail Europe: consolidating rail distribution before platforms capture it

Source: railadvent.co.uk → · Sector Retail & E-commerce Tech — 📬 subscribe to the Retail & E-commerce Tech newsletter

Omio Group, a German multimodal aggregator, is acquiring Rail Europe, an international rail distribution platform. The operation would bring the combined volume to 22 million train tickets per year, working with over 28,000 transport operators and resellers.

Rail Europe is historically the international distribution channel for European railway companies for travelers outside Europe. Omio brings its technology, its multimodal inventory (train, bus, ferry), and Rome2Rio, its travel discovery brand.

The logic is as defensive as it is offensive: before Uber, Google, or an Asian platform establishes itself as the sole interface for terrestrial travel in Europe, Omio is building the critical mass that makes eviction difficult. Rail Europe gives it the B2B distribution depth that its B2C platform could not generate alone.

Banijay Gaming takes over four Joa casinos in Pays de la Loire

Source: informateurjudiciaire.fr → · Sector Gaming — 📬 subscribe to the Gaming newsletter

Banijay Gaming—formed by the merger of Betclic and Tipico within the Banijay group—is acquiring four establishments of the Joa group in Pays de la Loire (including Les Sables-d'Olonne and Saumur), as part of the broader acquisition of Joa from funds managed by Blackstone and Kings Park Capital. Finalization is expected in the second half of the year.

Banijay Gaming is deploying an omnichannel strategy: combining online gaming (Betclic) and physical establishments to create loyalty loops that neither pure digital nor isolated casinos can build alone. Physical casinos provide the license, territorial anchoring, and local clientele; digital provides monetization between visits.

In a sector where physical casino margins are eroding and online gaming remains under regulatory pressure, combining the two creates a hybrid position that is difficult to replicate—provided that French online gaming regulations do not tighten the conditions for cross-selling between the two channels.

ABB acquires Rotork to expand its industrial automation offering

Source: machineedgeglobal.com → · Sector Horizontal & Productivity SaaS — 📬 subscribe to the Horizontal & Productivity SaaS newsletter

ABB, a Swiss electrical engineering and automation group, is acquiring Rotork, a British manufacturer of actuators and flow control systems. The amount is not disclosed.

Rotork is a benchmark in electric and pneumatic actuators for the oil, gas, water, and energy industries. Its integration into ABB strengthens the process automation offering at a time when the energy transition is generating structural demand for complex network control equipment.

For ABB, Rotork is not a diversification—it is a missing link in the value chain of critical infrastructure automation, whose demand will grow with industrial electrification.

Heliaq acquires Synten: the fifth building block of a Parisian cloud build-up

Heliaq, a Gironde-based IT services company specializing in IT infrastructure, cloud, and cybersecurity, is acquiring Synten, a cloud host based in Saint-Cloud, for €5 million in revenue (of which €4 million is recurring), and about twenty employees. This is the fifth acquisition since the LBO carried out in March 2025 with Chevrillon and Arkéa Capital, and the first of the fiscal year opened in April 2026.

Synten is integrated into Heliaq Solutions, the subsidiary dedicated to managed cloud and cybersecurity. The logic is clear: in an IT services build-up, recurring revenue is the metric that matters—€4 million out of €5 recurring is a quality asset for an acquirer whose financial shareholders value visibility.

Heliaq is methodically building an Île-de-France footprint from a Gironde base—the geography of the acquisition is as deliberate as the nature of the revenue.

Respire enters Capza's fold via a primary LBO

Respire, a French brand of natural cosmetics and household products, welcomes Capza as a minority shareholder in a primary LBO. The founders remain in the capital and at the helm. The firm VOLT Associés advised the founders.

The primary LBO is the company's first formal financial structuring: the founders partially monetize their position while retaining control, and Capza provides the resources to accelerate—distribution, internationalization, potentially external growth. In a consolidating natural and organic market, having a structured financial partner is now a condition for keeping pace with large brands that acquire independents.

Les Jeunes Pousses acquires struggling micro-nurseries

Les Jeunes Pousses, a growing personal services operator, is acquiring micro-nurseries to, in its words, "save as many jobs as possible in early childhood." The amount and number of establishments are not specified.

The micro-nursery sector is undergoing a structural crisis: fragile economic model, dependence on public aid, cost pressure. Acquisitions of distressed assets allow consolidating operators to acquire licenses, locations, and teams on favorable terms—the rhetoric of saved jobs is real, but it also accompanies a logic of external growth with low entry costs.

Dilosk sold to Pepper Advantage: consolidation of Irish mortgage credit

Source: businessnewsforprofit.com → · Sector Construction & PropTech — 📬 subscribe to the Construction & PropTech newsletter

Dilosk (brands Dilosk and ICS Mortgages), an Irish mortgage origination and servicing platform, is being sold to Pepper Advantage, a subsidiary of J.C. Flowers & Co., a global financial services specialist. Pepper Advantage manages €75 billion in assets in Ireland, Spain, and the UK. Financial terms are not disclosed.

The operation combines Dilosk's Irish origination with Pepper Advantage's credit management infrastructure and technology, creating an integrated chain from loan production to recovery. For institutional investors, this is a promise of direct access to assets originated and managed by the same entity—an increasingly decisive argument in private credit.

All of today's M&A, by sector

The full list for today — including the deals decoded above.

B2B Software & Cloud · 2 →

- Impact du GEO sur la demande internet des PME

- All for One — VINCI Energies s'associe à All for One pour accélérer sa croissance

Retail & E-commerce Tech · 2 →

- TCOG — Alistar intègre TCOG pour préparer la mode et retail à l'IA

- Micromania — Un groupe franco-canadien reprend Micromania, leader du jeu vidéo en France

Commerce & Consumer · 1 →

- Delivery Hero — Uber rachète Delivery Hero pour 13 Md€, fusion majeure de la livraison🔮 The next move: GrabFood — Their strong presence in Southeast Asia would extend their geographical reach after the acquisition of Delivery Hero. · hypothesis, not a fact

Construction & PropTech · 1 →

- Synten — Heliaq rachète Synten pour renforcer son offre en Île-de-France

Developer & IT Infrastructure · 1 →

- Prior Labs — SAP rachète Prior Labs, startup IA allemande, pour plus de 1 Md€

FinTech · 1 →

- Dilosk — Pepper Advantage rachète Dilosk, plateforme irlandaise de crédit immobilier

Gaming · 1 →

- Joa — Banijay Gaming rachète Joa, deuxième opérateur de casinos en France

Health & Wellness · 1 →

- Respire — Capza entre au capital de Respire dans le cadre d'un LBO primaire

Mobility & Transportation · 1 →

- Rail Europe — Omio Group rachète Rail Europe pour renforcer sa position ferroviaire

Robotics & Automation · 1 →

- Rotork — ABB rachète Rotork pour renforcer son offre d'automatisation

Space Tech · 1 →

- CLS — MDA Space rachète CLS, opérateur spatial français, avec soutien du CNES

The Physical World · 1 →

- Lynx — EssilorLuxottica rachète Lynx, startup française de réalité mixte

Other deals (sector not classified) · 3

- Services à la personne. En croissance, Les Jeunes pousses rachètent des micro-crèches pour "sauver un maximum d’emplois dans la petite enfance"

- DJUST Customer - C10

- Alerion Avocats conseil Entrepreneur Invest et BNP Paribas Développement - Alerion Avocats Paris

🚀 Fundraisings today · 13

In focus — the deals we decoded

Mistral raises at €20 billion valuation: the European fund enters the scene

Mistral AI is raising €3 billion in Series D at a valuation of €20 billion—up from €11.7 billion last September. EQT is in discussions to lead or co-lead this round via the new €5 billion European scale-up fund for which it has been appointed manager. The company is on track to exceed €1 billion in ARR in 2026 and has already raised $830 million in debt to finance its data centers, with a target of one gigawatt of capacity in Europe by 2030.

The immediate interpretation: Mistral confirms its status as a European AI champion and raises capital on terms that rival American labs.

But what changes in nature here is the source of capital. EQT is not acting as a classic venture fund—it is deploying European public money through an institutional vehicle designed to finance continental scale-ups. This is the first time a European industrial policy instrument has directly entered the capital of an AI lab of this magnitude, at this valuation.

The tension is real: one gigawatt of data centers is an infrastructure that costs billions before generating a single euro of margin. Most of the fundraising does not finance salaries—it finances compute, energy, concrete. Almost all the money is converted into fixed capital before value begins to circulate. And yet, the valuation doubles in less than a year.

What the market is betting on is that Mistral will not only be a model provider but the cognitive infrastructure of European enterprise—a rent-seeking position, not a simple product line. If this bet is right, the valuation is reasonable. If it is not, the debt and immobilized capital will weigh heavily.

For a French executive or investor: the question is no longer whether Mistral will survive—it is whether Europe can build an ecosystem of applications and services around it that justifies the infrastructure. Without that, the gigawatt of capacity will seek its customers elsewhere.

NeoCem raises €17 million for cement with nine times less carbon

NeoCem closes a €17 million fundraising round with Crédit Mutuel Impact to industrialize its low-carbon clay-based binder, presented as reducing CO₂ emissions by up to 90% compared to reference cement (CEM I), with no advertised additional cost for the user. Production has started at a site in Saint-Maximin (Oise), with a target capacity of 200,000 tons per year.

Cement is one of the most difficult sectors to decarbonize—clinker firing generates CO₂ through chemical reaction, not just combustion. NeoCem bypasses the problem by partially substituting clinker with activated clay. The price competitiveness argument is strategic: in construction, a green solution that costs more remains marginal, regardless of regulatory pressure.

€17 million to go from a pilot site to industrial capacity is a consistent ticket for the stage—the real question will be the speed of adoption by public contracting authorities, who represent the primary natural outlet for such an innovation.

Patrowl raises €11 million in Series A for attack surface management

Source: globalsecuritymag.fr → · Sector Cybersecurity — 📬 subscribe to the Cybersecurity newsletter

Patrowl raises €11 million in Series A. The company develops a continuous attack surface management platform—in short, it constantly maps what an organization exposes externally and identifies vulnerabilities before attackers do.

In a context where information systems are expanding (cloud, subcontractors, shadow IT), the attack surface has become an operational concept that CISOs struggle to control with traditional tools. Patrowl positions itself in this rapidly growing segment, competing with already well-funded American players.

€11 million in Series A is a ticket that allows for hiring sales teams and accelerating in the European market—where data sovereignty and regulatory requirements (NIS2, DORA) create a structural advantage for a French player.

Sateliot raises €150 million to connect smartphones directly from orbit

Sateliot, a Spanish startup, is seeking to raise €150 million to deploy a low-orbit satellite constellation offering direct 5G connectivity to smartphones—without terrestrial infrastructure. The technology targets white zones and emerging markets where deploying mobile towers is economically impossible.

The market for direct-to-device satellite connectivity is opening up: Starlink Direct to Cell, AST SpaceMobile, and now several European players. Sateliot's differentiation comes from the 3GPP standard (native compatibility with existing 5G networks) rather than proprietary technology.

€150 million is the minimum ticket to launch a credible constellation—but it is also the threshold below which one remains a niche player. The real competition lies in the ability to secure partnerships with telecom operators, not in technology alone.

Eye Security raises €60 million for sovereign cyber-defense with American backers

Source: siliconcanals.com → · Sector The Physical World — 📬 subscribe to the The Physical World newsletter

Eye Security, founded by former members of the Dutch intelligence services, raises €60 million to build a sovereign European cyber-defense offering. Two of its investors are American.

The tension is explicit in the very title of the fundraising: a company positioning itself on European digital sovereignty accepts American capital. This is not an absolute contradiction—American funds regularly finance European security assets—but it is a structural limit to the sovereign discourse. For institutional and governmental clients, the question of the capital control chain will be raised sooner or later.

€60 million for a managed cybersecurity player is a size that allows it to serve SMEs and mid-caps across Europe—the real test will be the ability to win public contracts in states that closely scrutinize the shareholding structure of their security providers.

Hyperion Robotics raises €6.4 million for robotic concrete microfactories

Source: eu-startups.com → · Sector Developer & IT Infrastructure — 📬 subscribe to the Developer & IT Infrastructure newsletter

Hyperion Robotics (Espoo, Finland) raises €6.4 million in a growth round, co-led by Course Corrected and the EIC Fund, with participation from RE Ventures (Romande Energie) and existing investors. The company deploys robotic microfactories for low-carbon concrete foundations, directly on construction sites or nearby, reducing the carbon footprint by up to 70% according to its data.

The approach is decentralized by design: rather than a central factory, Hyperion installs local production units where concrete is used, eliminating transport and adapting production to local demand. Romande Energie's participation (via RE Ventures) is a signal: energy companies are starting to invest in low-carbon construction materials, whose decarbonization directly depends on renewable electricity.

Z_One: Zest and Eureka! launch an early-stage AI and UrbanTech fund

Source: renseignementeconomique.fr →

Zest and Eureka! are launching Z_One, an early-stage fund targeting AI and UrbanTech, with a target of €55 million and a first closing at €5 million. The strategy targets early funding rounds in two verticals: applied artificial intelligence and urban technologies (mobility, energy, real estate, infrastructure).

The AI + UrbanTech combination reflects a growing shared conviction: the major application areas for AI in Europe are in slow-transforming sectors—cities, buildings, energy—where regulatory barriers and long cycles create windows for patient and specialized players.

Mio raises €1.9 million in pre-seed for an AI assistant in Slack

Source: thesaasnews.com → · Sector B2B Software & Cloud — 📬 subscribe to the B2B Software & Cloud newsletter

Mio (Paris) raises €1.9 million in pre-seed to develop an AI assistant that integrates directly into Slack workflows. The positioning is narrow and deliberate: rather than a general-purpose tool, Mio targets teams that live in Slack and want to automate tasks without changing environments.

The market for AI assistants integrated into collaboration tools is crowded, but the distribution logic through native integration is solid—adoption occurs where teams already work, without onboarding friction.

Nomad Éducation raises €800,000 to consolidate its free model

Source: aefinfo.fr → · Sector B2B Software & Cloud — 📬 subscribe to the B2B Software & Cloud newsletter

Nomad Éducation raises €800,000 from a round of business angels—including Damien Guermonprez (Lemon Way), Samuel Tual (Actual), Alain Rausher (Antin Infrastructure), and Philippe Yonnet (Search Foresight)—with the support of BPI France and Coface. The co-founders remain strongly majority shareholders.

Nomad Éducation offers a free learning application, primarily for high school and university students. The free model is assumed—monetization relies on partnerships and targeted premium offers. The fundraising aims to consolidate this model before international expansion.

📩 Subscribe to our newsletter to follow daily M&A and fundraising news: https://proplace.co/newsletter

All of today's fundraisings, by sector

The full list for today — including the deals decoded above.

Climate & Energy Tech · 2 →

- Triton Depth — Triton Depth lève des fonds pour sa technologie de surveillance sous-marine

- NeoCem — NeoCem lève 17 M€ pour son ciment bas carbone innovant

Cybersecurity · 2 →

- Patrowl — Patrowl lève 11 M€ en série A menée par Crédit Mutuel Innovation

- Eye Security — Eye Security lève 60 M€ en série C pour la cyberdéfense européenne souveraine

Developer & IT Infrastructure · 2 →

- Aqarios — Aqarios entre en bourse via SPAC, premier pure-play quantique allemand

- Mistral — Mistral lève 20 Md€ en série D menée par EQT depuis le Scale Up Fund

Robotics & Automation · 2 →

- microagi — microagi lève 55 M$ en seed pour sa plateforme Atlas de robotique

- Hyperion Robotics — Hyperion Robotics lève 6,4 M€ pour l'IA physique en infrastructure

B2B Software & Cloud · 1 →

- Mio — Mio lève 1,9 M€ en pre-seed pour sa solution SaaS

Education & EdTech · 1 →

- Nomad éducation — Nomad éducation lève 800 k€ pour son modèle gratuit et l'international

Space Tech · 1 →

- Sateliot — Sateliot lève 150 M€ pour la 5G par satellite directement aux téléphones

Other deals (sector not classified) · 2

- Zest et Eureka! lancent Z_One, un fondsêrly-stage ciblant l'IA et l'UrbanTech (objectif 55 M€) — Renseignement Économique

- RightLiens lance RightAdvisory : le conseil stratégique mensuel pour dirigeants et actionnaires - RightLiens