Analysis of the day

M&A and Fundraising Analysis for July 16, 2026

Defense, deep tech, and industrial consolidation dominate a busy day — from Thales-Exail to Helsing, European capital chooses its camps.

· Proplace

🌐 Translated from the French original by AI — the French version is authoritative.

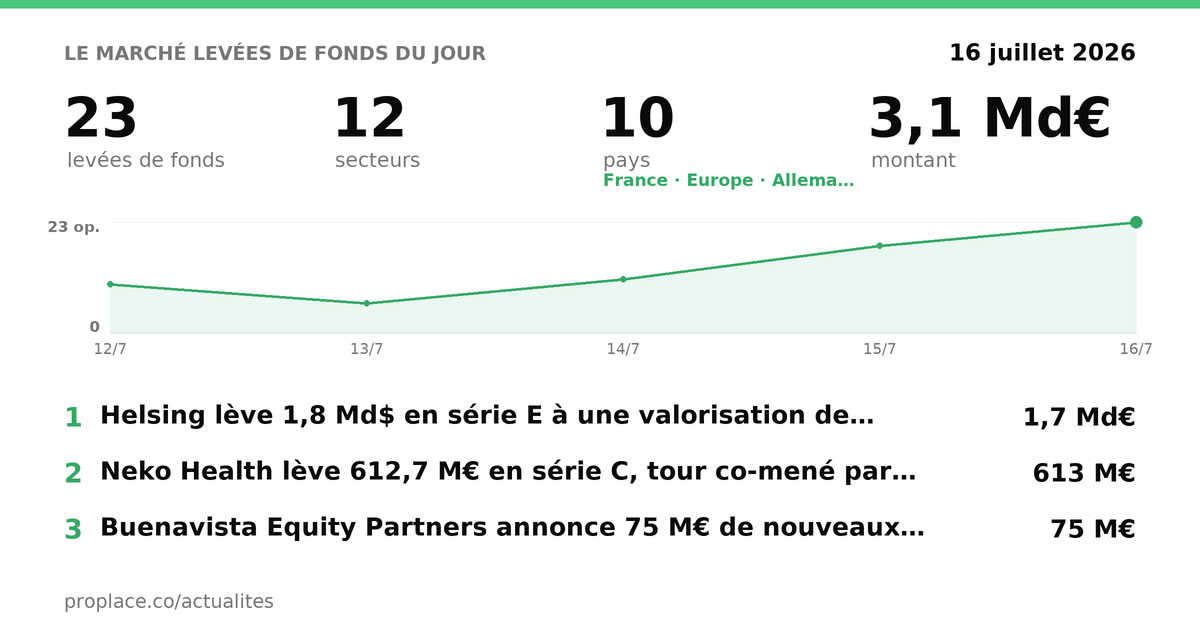

📊 Today's pulse — 57 deals · 34 M&A · 23 fundraisings · €10.5bn in play.

July 16 brings together two mutually reinforcing dynamics: a wave of industrial consolidation in France — defense, automotive, agri-food, construction — and an influx of capital into European breakthrough technologies, from AI defense to construction robotics. It's no coincidence that Thales' acquisition of Exail for €3.9 billion and Helsing's record fundraising of €1.7 billion coincide: the same geopolitical pressure is, upstream, reorienting state budgets, and downstream, reorienting private capital.

🤝 Mergers & acquisitions today · 34

In focus — the deals we decoded

Thales absorbs Exail: Sovereignty as the entry price

Thales announces the acquisition of the Gorgé family's stake in Exail Technologies (35.51%) at €134 per share, followed by a mandatory offer for the remainder, for a total enterprise value of €3.9 billion — a 44% premium over the unaffected share price on June 25. Exail reported €479 million in revenue in 2025 and covers underwater warfare, maritime drones, inertial navigation, and quantum sensors.

The immediate interpretation: Thales is consolidating its capabilities in the most technical segments of naval defense, with a return on investment from the first year announced by management.

But the real logic is more structural. Exail is one of the few European players mastering both precision inertial navigation and quantum sensors — two technologies that define the ability to operate without GPS in a contested environment. By absorbing Exail rather than settling for a partnership, Thales is locking in an irreplaceable building block before American consolidators or infrastructure funds value it out of reach. This is not a growth acquisition; it's a closing acquisition: you buy so no one else can buy.

For a French industrial group exposed to defense or precision navigation, the signal is clear: high-tech sovereignty assets are becoming rare and expensive. The window to access these building blocks — through partnership, co-development, or acquisition — is closing as major contractors repatriate them.

Lactalis and Quebec cheeses: The global leader's mechanics

Lactalis is acquiring a division from Canadian cooperative Agropur comprising three Quebec brands — Monsieur Gustav, OKA, and L'Extra — as well as two production sites in southern Quebec and import activities, for a turnover of approximately €115 million (CA$180 million). The transaction amount was not disclosed.

Canada is already Lactalis' third-largest market. The operation is consistent: established local brands, two industrial facilities, 400 employees retained. What this operation primarily illustrates is the logic of a mature global consolidator: each acquisition is modest in absolute value, but each strengthens a local distribution position that no one else can replicate without spending ten times more.

Unipres buys out its Italian partner to close a difficult decade

Source: lejournaldesentreprises.com →

Unipres, a Japanese automotive structural parts supplier, is acquiring for €45 million its Italian partner Magnetto's stake in their joint factory in Biache-Saint-Vaast (Pas-de-Calais), renamed Unipres France SAS. The site employs 250 people and supplies Renault, Stellantis, and Nissan. In 2025, the entity reported €79.5 million in revenue with a net loss of €42.5 million.

One buys out a deficit-making joint venture for €45 million when losing €42.5 million per year: the rationality is not short-term financial, it is industrial. Unipres is preserving a strategic production tool for its French customers and avoiding a liquidation that would cost it more in supply disruption and penalties. This is the price of maintaining a presence in a strained European automotive sector — a real option on recovery, not a profitable investment today.

TCRI Group: Montefiore consolidates industrial fluid distribution

Source: lejournaldesentreprises.com →

TC Concept and LRI-Sodime, two Lyon-based companies supported by Montefiore Investment since 2022, are merging to form TCRI Group, a player in the distribution of fluid transfer solutions (steel and stainless steel tubes, industrial valves). The new entity has nearly €200 million in revenue, 500 employees, and 37 sites in France, Spain, Morocco, and China. The stated ambition: €400 million in revenue within three years through organic growth and acquisitions.

Classic PE build-up operation in a fragmented market: two complementary products brought together under one banner to create an integrated offering difficult to replicate. The signal for regional players in the sector: consolidation has begun, and future targets will be valued as TCRI Group grows.

Leikar acquires France à Vélo: A venture studio goes operational

Leikar, a venture studio focused on sport and wellness, is making its first operational acquisition by buying France à Vélo, a specialist in cycling tours since 2000 — 30,000 cyclists accompanied, 140 itineraries, €17 million spent in the regions. The transaction amount was not disclosed.

A venture studio buying a profitable and established company rather than building one from scratch: this is a bet on the digital overhaul of a solid analog asset. The real question is whether Leikar can transform a niche operator into a European platform without diluting what makes France à Vélo valuable — its territorial depth and trusted relationship with cyclists.

KKR and Apax compete for Logoplaste: Plastic packaging resists

Source: privateequitywire.co.uk →

KKR and Apax Partners have submitted non-binding offers to acquire Logoplaste, a Portuguese manufacturer of rigid plastic packaging, in a transaction that could value the group at over €1.7 billion. The seller is Ontario Teachers' Pension Plan (OTPP), which acquired a stake in 2021 at approximately €1.4 billion. The founders would retain a minority stake.

The case illustrates the persistent appetite of funds for industrial packaging assets with a defensive position: Logoplaste operates integrated factories at its clients' sites (an "in-house" model), which creates an operational dependency difficult to break. For OTPP, the exit at over €1.7 billion validates an industrial infrastructure thesis — and for potential acquirers, the real value is in the stickiness of the model, not in growth.

Bridgepoint acquires GBA from Ardian: Certification as a recurring asset

Bridgepoint is acquiring a majority stake in GBA Group, a German laboratory testing and certification group, from Ardian, for a valuation exceeding €1 billion. GBA operates approximately 100 sites in Europe, North America, and Asia-Pacific, serving over 60,000 clients in agri-food, pharmaceuticals, medical devices, and cosmetics.

Bridgepoint is a repeat player in the sector: it has previously owned Element Materials Technology, LGC, Fera Science, and NMi. This is not diversification; it's sectoral conviction. Testing and certification companies have the ideal economic structure for private equity: recurring revenues backed by regulatory obligations, low capital intensity, and demand that grows with the complexity of global supply chains — every new regulation is a long-term contract.

Ryze enters Spain via Krata: Real estate, consulting, and continental expansion

Source: realassetinsight.com →

Ryze, an Italian real estate consulting and management firm, is acquiring Krata, a Madrid-based company specializing in real estate appraisal and technical consulting — the group's first Spanish operation. The transaction is valued at €250 million according to available sources.

Classic geographical expansion move for a real estate services player looking to cover the most liquid markets in Southern Europe. Spain, with Madrid as a hub, is the natural target after Italy.

HANZA acquires five Fortaco sites: European heavy mechanics restructuring

Source: nordicdefencesector.com →

HANZA, a Swedish contract manufacturing group, is acquiring five production sites specializing in heavy mechanics and complex assembly from Fortaco — located in Finland, Estonia, and Poland. The operation adds approximately 1,300 employees and €170 million in annual revenue to the HANZA platform.

The acquisition is part of HANZA's 2028 strategy: to build a European manufacturing platform capable of absorbing growing demand for complex industrial production, particularly in defense and heavy equipment. In a context of European reindustrialization, players capable of aggregating fragmented manufacturing capacities into a coherent network have increasing value — which is exactly what HANZA is doing.

Batibig ventilates its Parisian growth

Source: cfnews.net → · Sector FinTech — 📬 subscribe to the FinTech newsletter

Batibig, a Parisian construction group supported by Siparex and EMZ, with approximately €350 million in revenue, is making a new build-up acquisition in Île-de-France. The target and amount are not disclosed, but the thesis is one of sectoral consolidation in secondary works and building services in the Paris region — a fragmented market, with demand supported by energy renovation and the Grand Paris project.

All of today's M&A, by sector

The full list for today — including the deals decoded above.

Industrial Tech & Manufacturing · 7 →

- Redo Oy — Invex Group acquiert Redo Oy (Finlande) via Mutares

- Advantics — ABB acquiert Advantics (technologies industrielles, France)

- TC Concept — TC Concept et LRI-Sodime fusionnent pour créer TCRI Group (France)

- Unipres — Unipres investit 45 M€ pour reprendre intégralement son usine (France)

- Kronos Polymer Polska — Aliplast acquiert 70% de Kronos Polymer Polska (recyclage plastique, Pologne)

- Logoplaste — KKR et Apax enchérissent pour Logoplaste (emballage, 1,7 Md€)

- HANZA — HANZA acquiert une entreprise générant 1,9 Md SEK de revenus annuels

Climate & Energy Tech · 4 →

- Eurowind Energy — Eurowind Energy acquiert la plateforme d'énergies renouvelables suédoise d'EnBW

- Carbyon — Airhive acquiert Carbyon (capture directe du CO2, Europe)

- Elemo — Waldevar acquiert Elemo (spécialiste réseau électrique, Roumanie)

- Cogenio — GETEC acquiert Cogenio (énergie distribuée, Italie)

B2B Software & Cloud · 3 →

- GBA — Bridgepoint acquiert une majorité de GBA pour plus de 1 Md€ (Europe)

- Solver Machine Learning — Var Group acquiert Solver Machine Learning (IA, Espagne)

- Oscar ai — Oscar ai veut automatiser et démocratiser le SEO et le GEO pour les entreprises

Food & AgTech · 3 →

- Agropur — Lactalis rachète trois marques de fromages d'Agropur (produits laitiers, Canada)

- Keragum — Nexira rachète Keragum (caroube, Maroc)

- Alma — Apheon acquiert Alma (snacks surgelés asiatiques, France)

Mobility & Transportation · 3 →

- TotalEnergies B2B charging — CUBOS acquiert l'activité de recharge B2B de TotalEnergies (Allemagne)

- IBH — Hunyvers acquiert IBH pour former le numéro deux du camping-car (France)

- France à Vélo — Leikar acquiert France à Vélo (cyclotourisme, France)

Biotech & Pharma · 2 →

- Recordati — CVC et GBL proposent une OPA sur Recordati (pharma, Italie)

- Esperion — Archimed prend le contrôle d'Esperion (biotech pharma, États-Unis)

Developer & IT Infrastructure · 2 →

- Exail Technologies — Thales prend le contrôle d'Exail Technologies pour 3,9 Md€ (France)

- Friendship Systems — Maya HTT acquiert Friendship Systems et CAESES (simulation logicielle)

Health & Wellness · 2 →

- Pflegia — Ardian acquiert une participation majoritaire dans Pflegia (santé, Allemagne)

- Floralpina — Groupe PLC acquiert Floralpina (compléments alimentaires, France)

Retail & E-commerce Tech · 2 →

- Alinea — MH France/Aosom rachète la marque Alinea (mobilier, France)

- Trakks — I-Run acquiert la chaîne de retail Trakks (outdoor, Belgique)

Robotics & Automation · 2 →

- Smart Innovation — KION acquiert 70% de Smart Innovation (chariots autonomes, Belgique)

- Autonomous forklift division — KION acquiert 70% de la division chariots autonomes de Colruyt (Belgique)

Construction & PropTech · 1 →

- Krata — Ryze acquiert Krata et entre en Espagne (évaluation immobilière)

Cybersecurity · 1 →

- Lyvoc — Allurity acquiert Lyvoc (intégration cybersécurité)

MedTech & Devices · 1 →

- Tedisel Medical — Reinsberg Group acquiert Tedisel Medical (équipements médicaux, Espagne)

Other deals (sector not classified) · 1

- Lactalis: accord pour acheter trois marques de fromages du canadien Agropur - 15/07/2026 à 17:29 - Boursorama

🚀 Fundraisings today · 23

In focus — the deals we decoded

Helsing raises €1.7 billion at $18 billion: Europe gets its Anduril

Source: agenccy.ai → · Sector The Physical World — 📬 subscribe to the The Physical World newsletter

Helsing, a Munich-based AI defense company, closes a Series E round of $1.8 billion (approximately €1.7 billion) at a valuation of $18 billion — the largest funding round ever for a European defense startup. Demand "significantly" exceeded allocation. The round brings together Goldman Sachs Alternatives, Dragoneer, Iconiq, Lightspeed, the Canada Pension Plan Investment Board, and JPMorgan Chase.

Helsing builds strike drones (HX-2), an operational command platform (Altra), and autonomy software for armed forces. The thesis: modern deterrence is played out in the software layer — the speed at which a force perceives, decides, and strikes — and Europe cannot outsource this layer to the United States.

What is striking about the composition of the round is less the amount than the nature of the investors. Canadian sovereign pension funds, a leading American investment bank, crossover funds usually reserved for mature technology stocks: this capital does not come from traditional venture capital; it comes from allocators who treat Helsing as national security infrastructure. When a private asset is financed like sovereign debt, it means that states — at least implicitly — are assumed to be long-term customers. The $18 billion valuation is not a venture bubble: it is an anticipation of defense budgets that will not decrease.

For a French investor or industrialist exposed to defense, the lesson is twofold: the capital available for AI defense technologies is now unlimited on a European scale, but the window to build competitive positions is closing fast — Helsing is already at $18 billion.

Neko Health raises €613 million: Daniel Ek bets on large-scale prevention

Source: eu-startups.com → · Sector HealthTech & Digital Health — 📬 subscribe to the HealthTech & Digital Health newsletter

Neko Health, a Swedish health tech company co-founded by Daniel Ek (Spotify founder), raises €612.7 million in a Series C round, led by Lightspeed Venture Partners and co-led by O.G. Venture Partners, with participation from Atomico, General Catalyst, Lakestar, and several new entrants. The round follows a Series B of €250 million in January 2025.

Neko Health offers comprehensive health check-ups via body-scanning — one hour of scanning, exhaustive physiological data, a logic of early detection. The fundraising finances the opening of the first American clinics in New York.

The list of individual investors — Zuckerberg, Sharapova, Thierry Henry, will.i.am — is a signal of positioning as much as conviction: Neko targets the premium segment of health prevention, where brand and community matter as much as technology. The real bet is not medical; it is economic: convincing solvent individuals to pay regularly to stay healthy rather than paying occasionally to get well — a reversal of the traditional healthcare model which, if it holds, generates recurring revenue that even insurers have not been able to capture.

LinqAlpha raises $22 million for its AI agents in finance

Source: actudesseries.com → · Sector FinTech — 📬 subscribe to the FinTech newsletter

LinqAlpha raises $22 million (approximately €20 million) in a Series A round, led by AVP, Atinum, and GFT Ventures. The company develops artificial intelligence agents specialized in reading financial documents — regulatory filings, analyst transcripts, news feeds — for hedge funds and asset managers. It claims over 70 financial institution clients.

Where general-purpose tools fail in finance — source traceability, regulatory precision, operational speed — LinqAlpha builds vertical specialization. What is being financed here is less AI than friction: analysts spend a considerable part of their time extracting signals from long and repetitive documents, and every hour saved on this extraction is directly convertible into a competitive advantage for a fund.

Forsee Power and FCAP: Recapitalization under foreign investment control

Forsee Power, a specialist in smart battery systems for commercial and industrial electric vehicles, enters into exclusive negotiations with FCAP Investors Pte. Ltd, a Singaporean fund specializing in innovative technologies and industries, for a capital increase of approximately €20 million. The operation includes the repurchase of Mitsui & Co's stake by Eurazeo, Noria, and FCAP's SPV. Current shareholders — Bpifrance Investissement, Eurazeo, Noria — maintain their support.

The operation is subject to prior authorization from the Ministry of Economy under foreign investment control — a signal that Forsee Power is considered a sensitive asset in the industrial electric vehicle value chain. What this recapitalization reveals is the structural fragility of an electric transition player in a market that is slow to take off: equity needs to be strengthened not to finance hypergrowth, but to hold on until demand catches up with supply.

NeoCem raises €17 million for its low-carbon binder

Source: finyear.com → · Sector Knowledge & Media — 📬 subscribe to the Knowledge & Media newsletter

NeoCem, a Lille-based startup developing cementitious materials based on calcined clays to reduce CO₂ emissions, raises €17 million with the entry of a new investor alongside existing shareholders. Cement accounts for approximately 8% of global CO₂ emissions; alternative binders are one of the few decarbonization pathways available on an industrial scale without waiting for a technological breakthrough. NeoCem is tackling a structurally conservative market — construction — with a solution that reduces emissions without changing implementation processes: it is precisely this type of compatibility with existing practices that conditions large-scale adoption.

Valarian raises $50 million for sovereign British AI

Source: aimagazine.com → · Sector Developer & IT Infrastructure — 📬 subscribe to the Developer & IT Infrastructure newsletter

Valarian, a British cybersecurity and AI infrastructure company, raises $50 million (approximately €46 million) in a Series A round led by New Enterprise Associates (NEA). Its ACRA platform allows organizations to deploy AI models while keeping sensitive data within their own environment — without exporting it to American cloud infrastructures.

The context is explicit: the United Kingdom is deemed too dependent on American technology infrastructures (Microsoft, Palantir, Amazon), and Valarian responds to a governmental and defense demand for AI deployable without external dependence. Digital sovereignty is no longer a political argument — it is a market. And this market is all the more defensible as customers (governments, defense, regulated sectors) cannot easily change providers once the infrastructure is in place.

Monumental raises $32 million to robotize construction sites

Source: headlinesbriefing.com → · Sector Construction & PropTech — 📬 subscribe to the Construction & PropTech newsletter

Monumental, an Amsterdam-based construction robotics startup, raises $32 million (approximately €29 million) in a Series B round led by Khosla Ventures, with participation from Plural and Hummingbird. The co-founders — Salar al Khafaji and Sebastiaan Visser — previously sold Silk to Palantir in 2016 and are applying Palantir's deployed engineering model to physical robotics.

The construction industry has seen declining productivity since the 1960s in the United States — a paradox for a sector that has not experienced a revolution in its methods while all others have mechanized. Monumental first targets Europe, then the United States where the labor shortage in construction is estimated to be between 200,000 and 400,000 positions per month according to industry sources. What makes the thesis strong is that Monumental is not trying to replace skilled labor — it is trying to fill a void that the market can no longer fill otherwise. When the shortage is structural, robotics ceases to be an option and becomes a necessity.

Risk Ledger raises €28 million for supply chain security

Source: thesaasnews.com → · Sector B2B Software & Cloud — 📬 subscribe to the B2B Software & Cloud newsletter

Risk Ledger raises £24 million (approximately €28 million) in a Series B round led by Axiom Equity to expand its supply chain security platform and launch operations in the United States. The company offers a network for sharing risk data between principals and suppliers, allowing continuous assessment of the security posture of each link in a chain.

In an environment where rebound attacks — compromising a supplier to reach a customer — have become the norm, supply chain security has moved from "nice to have" to "regulatory obligation." Risk Ledger positions itself on this structural constraint, with a network model that self-reinforces as the number of participants grows.

Buenavista Equity Partners: €75 million for Spanish mid-market buyout

Buenavista Equity Partners, an independent Madrid-based asset management firm founded in 1996, announces €75 million in new commitments from Fond-ICO Global in its third buyout fund, Buenavista Buyout Innvierte III. Buenavista manages over €1.3 billion across several vehicles (private equity, infrastructure, venture) and operates in the Spanish low-to-mid market segment.

Commitment from a Spanish public fund of funds to a regional buyout vehicle: this is the development model of the Iberian PE ecosystem, where Fond-ICO Global plays the role of institutional catalyst. For LPs seeking exposure to the Spanish mid-market, Fond-ICO Global's presence in a fund is both a signal of seriousness and a guarantee of public co-investment — but it says little about future performance.

📩 Subscribe to our newsletter to follow daily M&A and fundraising news: https://proplace.co/newsletter

All of today's fundraisings, by sector

The full list for today — including the deals decoded above.

B2B Software & Cloud · 4 →

- Mio — Mio lève 1,9 M€ pour son assistant IA intégré à Slack (France)

- Display.dev — Display.dev lève 470 K€ en pre-seed pour sa plateforme IA (Estonie)

- Buenavista Equity Partners — Buenavista Equity Partners lève 75 M€ pour son 3e fonds (Espagne)

- Nous — Nous lève 2,3 M€ en seed pour scaler Koncentra

Climate & Energy Tech · 3 →

- NeoCem — NeoCem lève 17 M€ pour sa technologie bas carbone (France)

- Munich Electrification — Ardian investit dans Munich Electrification (batterie, Allemagne)

- Forsee Power — Forsee Power entre en négociation avec FCAP pour un investissement

Construction & PropTech · 3 →

- Batibig — Batibig poursuit sa croissance en Île-de-France avec Siparex et EMZ

- Nestermind — Nestermind lève un montant à 7 chiffres en seed pour son CRM IA

- Rivage — Rivage lève 1,5 M€ pour sa plateforme de gestion locative (France)

FinTech · 3 →

- Nopan — Nopan lève 7,2 M€ pour optimiser les paiements compte-à-compte

- Float — Float lève 4,5 M€ en série A pour sa plateforme financière IA (Suède)

- LinqAlpha — LinqAlpha lève 22 M$ pour ses agents IA en finance (France)

Cybersecurity · 2 →

- Risk Ledger — Risk Ledger lève 24 M£ en série B pour la gestion des risques cyber

- Valarian — Can UK Tech Firm Valarian Ensure Secure AI Deployment?

Developer & IT Infrastructure · 2 →

- Meticulous — Meticulous lève 15 M$ en série A pour vérifier le code généré par IA

- Helsing — Helsing lève 1,8 Md$ en série E+ pour la défense et l'IA (Allemagne)

Gaming · 1 →

- SoccerSolver — SoccerSolver lève 850 K€ en pre-seed pour l'IA du football professionnel

HealthTech & Digital Health · 1 →

- Neko Health — Neko Health lève 612,7 M€ en série C pour son expansion US

Logistics & Supply Chain · 1 →

- TIP Group — I Squared Capital cède 25% de TIP Group à 4 Md€ de valorisation

MedTech & Devices · 1 →

- Cornea Sense — Cornea Sense lève 1,1 M€ en pre-seed pour mesurer l'hydratation cornéenne

RegTech & Compliance · 1 →

- Skalar — Skalar lève 12 M€ en seed pour son cabinet de conseil fiscal IA

Robotics & Automation · 1 →

- Monumental — Monumental lève 32 M$ en série B pour l'automatisation de la construction