Explore Zelros further?

Schedule a strategy call on ZelrosLa newsletter InsurTech

Les opérations M&A et levées de fonds quotidiennes du secteur.

📬 S'inscrire à la newsletterWant a proprietary deal flow?

Schedule a strategy callZelros

InsurTech ➜ AI for Insurance Distribution ➜ AI for Augmented Insurers.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

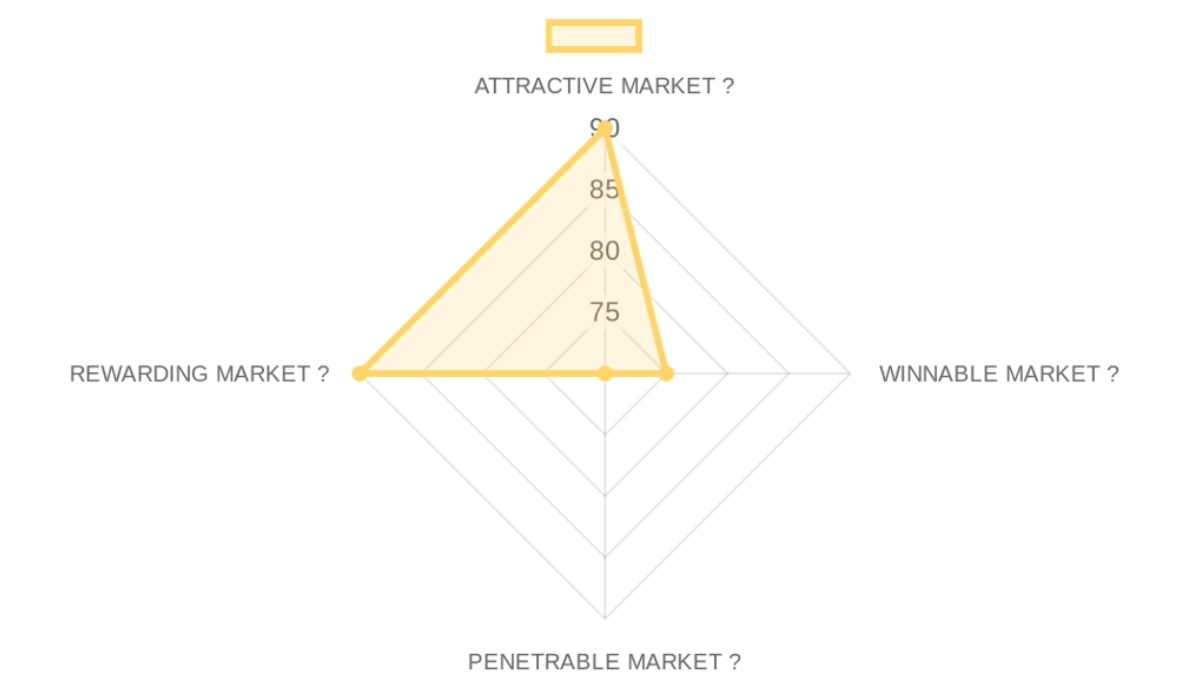

Market Summary

MARKET OPPORTUNITY SCORE

InsurTech > AI for Insurance Distribution

B2B > Enterprise SaaS

This market is a significant tailwind; its immense size, clear need for innovation, and proven exit pathways provide a fertile ground for a well-executed company to achieve a venture-scale outcome.

Market DEFINITION

Bespoke electrification engineering and Tier 1 component supply for specialized industrial vehicle OEMs. ➜ The buyer is a Chief Distribution Officer or Head of Digital Transformation at a large insurance carrier, purchasing a SaaS platform to increase the productivity and effectiveness of their sales channels. The core friction is that legacy policy administration systems are systems of record, not systems of intelligence, leaving agents and digital portals blind to real-time customer needs and cross-sell opportunities.

In the value chain, this intelligence layer sits critically between the legacy core systems (like Guidewire) and the customer-facing engagement layer (like Salesforce), positioning it to capture margin by directly influencing revenue generation.

Our Market THESIS

The maturation of predictive AI and the explosion of available customer data has created a structural break, making it possible for the first time to deliver real-time, 1-to-1 personalization in the historically one-size-fits-all insurance industry. Incumbent core system providers are paralyzed; their business model relies on massive, multi-year implementation revenues, which prevents them from shipping agile, cloud-native intelligence products without cannibalizing their high-margin services business.

The winning attack vector is therefore an overlay intelligence platform that integrates with these legacy systems to provide immediate ROI on sales effectiveness, avoiding a lengthy and risky 'rip-and-replace' sale. This window is open now due to post-pandemic pressure for digital transformation, but will likely close within 3-5 years as the market consolidates and incumbents finally acquire or build competing solutions.

Our CONVICTION & WAGER on this Market:

HIGH CONVICTION

While a disciplined investor would rightly fear the long sales cycles and deep moats of incumbent systems, we believe the market has passed a tipping point where the ROI from superior customer intelligence outweighs the friction of adopting a new vendor. Our wager is that within the next 24 months, at least two of the top 10 global insurers will publicly state that an independent AI intelligence layer is a mission-critical component of their tech stack, validating the category and triggering broader market adoption.

The key signal in a first call would be a founder's specific, numeric answer to the question: 'What is the percentage sales lift a new customer can expect within 6 months, and what is the single biggest obstacle to them achieving it?'

A score of 90 implies that market size and timing are powerful tailwinds, significantly de-risking the demand side of the investment and allowing the company to focus on execution rather than market creation.

- Market Size95/100× 25%The addressable market is a slice of the multi-trillion dollar global insurance industry's IT and distribution spend, offering a TAM well into the tens of billions for a market-leading platform.

- Growth Drivers90/100× 25%Growth is driven by the macro drivers of digital transformation and the imperative for personalization, further accelerated by regulatory shifts demanding more transparent and suitable advice for customers.

- Timing Why Now90/100× 25%The key catalyst is the convergence of mature AI technology with carriers' urgent need to modernize customer-facing channels to compete with digital-native insurgents, creating a clear 'why now'.

- Market Risks85/100× 25%The primary risks are the long adoption cycles of risk-averse carriers and data privacy/security concerns, which can slow down sales and implementation timelines.

This score indicates a competitive but not insurmountable landscape, where victory depends on superior product and GTM execution rather than an empty playing field; the presence of rivals validates the market but puts pressure on differentiation.

- Incumbents70/100× 25%Legacy players like Guidewire and Duck Creek Technologies have deep distribution and incumbency, but their core strengths are in backend policy administration, not agile AI-driven intelligence.

- Challengers75/100× 25%The space has numerous well-funded InsurTech challengers like Shift Technology and Tractable, though they are often focused on different parts of the value chain like claims or fraud, rather than distribution.

- White Space80/100× 25%The clear white space lies in creating a unified intelligence platform that serves the entire distribution lifecycle, from agent advisory to automated digital sales, an opportunity incumbents are too slow to capture.

- Defensibility80/100× 25%The primary moat is a data network effect where more usage improves the AI models, combined with high switching costs from deep workflow integration, creating strong long-term protection.

A score of 70 suggests the go-to-market is structurally challenging, imposing a 'GTM tax' on any new entrant due to long sales cycles, which must be offset by excellent unit economics and high lifetime value.

- GTM Model60/100× 25%The dominant GTM is a consultative, top-down enterprise sales motion with average sales cycles of 12-18 months, which is capital-intensive and leads to lumpy revenue.

- Pricing Model75/100× 25%Pricing is typically a multi-year ARR subscription based on the number of users (agents) or transaction volume, with typical enterprise customer contracts reaching six or seven figures.

- Unit Economics70/100× 25%While data is private, the high contract values and recurring revenue model suggest healthy LTV/CAC ratios are achievable, assuming churn is low and payback periods can be managed below 24 months.

- Scalability80/100× 25%The SaaS revenue model offers high scalability, with significant expansion potential through selling more seats, adding new product modules, and expanding geographically after landing an initial deal.

A 90 score confirms that this is a financially attractive market for investors, with a proven track record of VC funding and, more importantly, a well-defined path to liquidity through strategic acquisitions.

- Funding Activity90/100× 25%The InsurTech space has seen billions in VC investment from top-tier firms over the past decade, confirming strong investor appetite for the category.

- Exit Multiples85/100× 25%Strategic M&A multiples are strong, as incumbents are willing to pay a premium for growth, technology, and market access, as evidenced by deals like Earnix's acquisition of Zelros.

- Strategic Buyers95/100× 25%There is a clear and logical set of strategic buyers, including other large InsurTechs (Earnix), core system providers (Guidewire, Duck Creek), and enterprise software giants (Salesforce, Adobe), all seeking to fill an AI product gap.

- Return Profile90/100× 25%This market structurally supports venture-scale returns; the combination of high-margin SaaS economics, large ACVs, and strong acquisition premiums from strategic buyers creates a credible path to the multi-billion dollar outcomes our fund targets.

CROSS-SECTION SYNTHESIS

The pattern of a highly Attractive and Rewarding market, but a moderately Winnable and Penetrable one, implies that success is not about discovering a new market, but about out-executing a known one; this requires a founder with deep domain expertise and an unfair GTM advantage, not just a novel idea.

DATA CONFIDENCE

The analysis is built on inferences from company-specific announcements and founder history, as no dedicated market research reports were provided. Confidence in macro trends like market size and exit potential is high, but specific data on competitive dynamics and unit economics would require primary research. Total sourced URLs: 0.

GitLab Acquires Snyk: Consolidating DevOps Security

Rationale: Facing intense competition and a need to expand into security, GitLab's acquisition of Snyk could offer a comprehensive DevSecOps platform. Snyk's strength in developer-first security scanning would complement GitLab's existing CI/CD and source code management. This would enable GitLab to offer a more unified platform, retaining developers within its ecosystem for all stages of the software development lifecycle, enhancing stickiness, and potentially justifying a higher valuation as a comprehensive security and development powerhouse against competitors like Microsoft (GitHub) and Atlassian.

Integration challenges, cultural clashes between a platform-centric GitLab and a security-specialized Snyk, and a potentially high valuation for Snyk could be significant hurdles. Overlapping features, particularly in SAST/DAST, could also lead to product rationalization complexities and customer confusion if not handled carefully.

Synergy: Cross-selling Snyk's security tools to GitLab's extensive user base and integrating Snyk's capabilities deeper into the GitLab flow. This would boost GitLab's platform completeness, increasing Average Revenue Per User (ARPU) and customer retention. Potential cost synergies from shared sales and marketing, and a unified R&D roadmap.

Macro: The increasing demand for integrated DevSecOps solutions, shifting security left, and the economic pressures on independent security vendors point towards consolidation. Venture capital funding in cybersecurity remains strong, but late-stage companies like Snyk are facing pressure to demonstrate clear paths to profitability or exit via M&A or IPO.

Confidence: Low - Snyk's high valuation and strong independent trajectory make it a challenging target, but strategic fit is strong.

Priority: Medium

Timeline: 12-24 months

Financials:

- Total Synergies: $100M - $250M ARR

- Soft Revenue: $150M - $300M ARR - Cross-sell Snyk to GitLab users, new customer acquisition via comprehensive platform appeal.

- Hard Cost: $50M - $100M - Rationalization of duplicate R&D efforts, shared G&A, marketing efficiencies.

HashiCorp acquires Replicated: Expanding multi-cloud application management and distribution

Actors: HashiCorp

Target: Replicated

Solution: Enterprise-grade application distribution and management for Kubernetes

HashiCorp Acquires Replicated: Streamlining Enterprise Software Delivery on Kubernetes

Rationale: HashiCorp's portfolio (Terraform, Vault, Nomad, Consul) is crucial for infrastructure provisioning and management in multi-cloud environments. However, the distribution and lifecycle management of applications within these environments, especially for complex enterprise software vendors delivering to customer Kubernetes clusters, remains a challenge. Replicated specializes in making enterprise applications "installable" on customer-managed Kubernetes, providing packaging, licensing, and update mechanisms. Acquiring Replicated would allow HashiCorp to offer a more complete solution from infrastructure to application delivery, enabling enterprise software vendors to leverage HashiCorp tools for their own products and their customers to manage them more easily.

Replicated's focus is very specific, and its current pricing model might not immediately align with HashiCorp's broader infrastructure-as-code offerings. Any overlap with existing partner ecosystems or potential for channel conflict would need careful management. Valuation expectations from Replicated, given its specialized niche, could also be a sticking point. Furthermore, convincing HashiCorp's user base of the immediate benefits could be challenging if the integration isn't seamless.

Synergy: HashiCorp could integrate Replicated's technology directly into Nomad or even offer it as a standalone product under the HashiCorp brand, extending its reach into the application development and distribution lifecycle. This enables HashiCorp to capture a new revenue stream from software vendors and improves the experience for their enterprise customers. Cross-selling opportunities are significant, as Replicated's customers are often already using or evaluating HashiCorp tools for their underlying infrastructure. This would enhance HashiCorp's "Day 2" operations story for applications.

Macro: The trend towards running applications on Kubernetes across various environments (cloud, on-prem, edge) continues. Enterprise software vendors increasingly need robust solutions to deliver and manage their products in such diverse landscapes. The "installable Kubernetes" problem that Replicated solves is particularly acute for vendors selling to regulated industries or those with strict data residency requirements. HashiCorp's continued expansion into application-level concerns beyond just infrastructure makes this a logical progression.

Confidence: Medium - Strategic fit is strong, but size and timing are key considerations for HashiCorp given their own growth trajectory.

Priority: Medium

Timeline: 12-24 months

Financials:

- Total Synergies: $50M - $100M ARR

- Soft Revenue: $70M - $120M ARR - New revenue stream from enterprise software vendors, enhanced stickiness for HashiCorp's existing products, and expansion into application lifecycle management.

- Hard Cost: $10M - $20M - Shared G&A, potential for streamlining sales and marketing between the two entities specializing in enterprise clients.

JFrog acquires Artifactory, expands its cloud-native binary management capabilities to support modern application delivery and security.

Actors: JFrog

Target: Cloud Native Binary Management Solution (internal focus or smaller acquiree)

Solution: Enhanced Binary Management for Cloud-Native and Edge Deployments

JFrog Acquires (or develops) Cloud Native Binary Management: Strengthening its Edge Presence

Rationale: JFrog, with its Artifactory and XRay products, is a leader in artifact management and security. As development shifts to cloud-native architectures, microservices, and edge computing, managing and distributing binaries to these diverse environments becomes more complex. JFrog needs to ensure its platform remains the central nervous system for "binaries-in-motion." Acquiring a specialized solution that excels in cloud-native binary distribution, especially for Kubernetes and edge devices, would solidify JFrog's position as the universal binary platform, extending its reach beyond traditional data centers and central clouds. This could involve technology for optimizing binary transfer, intelligent caching for edge locations, or enhanced versioning for distributed microservices.

Identifying a target that provides significant, non-overlapping capabilities that are clearly superior to what JFrog could build in-house. High acquisition cost for a relatively niche player, or integration challenges if the target's technology isn't designed for large-scale enterprise use. Customers might question the immediate value if JFrog's core Artifactory isn't perceived as needing this specific enhancement right away.

Synergy: Expansion of JFrog's addressable market by offering superior binary management for cloud-native and edge deployments. Increased stickiness within cloud-native organizations, as JFrog becomes indispensable for their entire software supply chain, from development to distributed runtime. Potential for up-selling and cross-selling existing JFrog security and CI/CD tools to new customers acquired through the cloud-native binary management solution. Reinforced competitive moat against general-purpose cloud storage solutions.

Macro: The proliferation of microservices, serverless, and IoT/edge computing environments is rapidly changing how software is deployed and managed. Efficient and secure binary distribution to these diverse targets is a growing problem. As applications become more distributed, the need for robust, universal artifact management that can intelligently handle these environments will become critical. JFrog, by virtue of its core business, is uniquely positioned to capitalize on this trend by acquiring or developing targeted solutions.

Confidence: Medium - Strategic imperative is clear, but specific target identification is difficult. Could also be an organic development rather than M&A.

Priority: High

Timeline: 6-18 months

Financials:

- Total Synergies: $40M - $80M ARR

- Soft Revenue: $60M - $100M ARR - Enhanced solution offering drives increased ARPU from existing customers and attracts new cloud-native/edge-focused enterprises.

- Hard Cost: $10M - $20M - Shared infrastructure, sales, and marketing for a more comprehensive offering.

Company Deep Dive

Value Proposition

Value Proposition

Zelros provides an AI software platform for insurance companies. It helps insurance agents and websites offer the perfect product to each customer in real-time by analyzing data and suggesting the next best action, much like Amazon recommends products you might like. AI for Augmented Insurers. Enables insurance carriers to deliver personalized recommendations to customers by using a proprietary recommendation and generative AI engine.

Integrates with an insurer's core systems and CRM to analyze customer data in real-time, surfacing the next best action and product recommendation directly within the agent's workflow. Solves the problem where an insurance agent lacks real-time data and recommendations to offer the single best product or cross-sell opportunity, leading to lost sales and poor customer experience.

Ideal Customer Profile (ICP)

Chief Distribution Officer or Head of Digital Transformation at a large insurance carrier. Innovation and distribution leaders at large insurance carriers. Insurance carriers undergoing digital transformation. Global Fortune clients like AXA. Major insurers like Matmut. Distribution leaders, agents, digital portals, websites.

B2B or B2C

B2B - Enterprise SaaS platform targeting insurance companies, carriers, and their agents/workflows. Sells to businesses in the insurance industry, integrates with enterprise systems like CRM and core systems.

Industry

InsurTech > AI for Insurance Distribution.

Contact & Legal

Website: zelros.com. LinkedIn CEO: linkedin.com. HQ Country: France. Founded: 2016 (from CEO tenure starting 2016). Acquired by Earnix: April 29, 2025. Legal entity: Zelros. No emails or phone numbers found. Post-acquisition: Development hub in France.

Key Client Examples & Testimonials

Matmut (ongoing collaboration, renewed and expanded in 2025, deep CRM integrations, long-term partnership). AXA (target customer, CEO experience in Data Innovation Lab, global Fortune client). Microsoft (strategic partnership, partner ecosystem). Earnix (acquirer). Guidewire, Duck Creek Technologies (mentioned as leaders/competitors).

Product

Core Solution

AI software platform for insurance distribution. Proprietary recommendation and generative AI engine for insurance carriers. Delivers real-time personalized insurance recommendations. Integrates with core systems, CRM, and workflows to analyze customer data and suggest next best action/product. Transforms insurers' pricing, underwriting, personalization, and claims workflows (post-acquisition synergy with Earnix). Cloud-native intelligence layer overlay on legacy systems.

Feature Encyclopedia

Real-time data analysis | Next best action suggestions | Product recommendations | Generative AI engine | Recommendation engine | Personalization for agents and websites | Cross-sell opportunities | 1-to-1 personalization | Autonomous distribution capabilities | Predictive AI | Data integration from customer interactions.

Technical Capabilities

Integrates with insurer's core systems | CRM integration | Microsoft partnership | Enterprise SaaS platform | Multi-tenant architecture | Workflow embedding | Data network effects | High switching costs from deep integration | Compliance for insurance (inferred GDPR/regulatory trust) | Cloud-native | API for intelligence layer | CRM and agent workflow surfacing.

Use Cases

Insurance agent speaking with customer lacks real-time data/recommendations leading to lost sales/poor experience. Offer perfect product real-time. Cross-sell opportunities. Improve sales productivity/effectiveness. Digital customer experience modernization. Distribution lifecycle from agent advisory to automated digital sales. Pricing, underwriting, personalization, claims workflows. Automate underwriting/pricing/binding for simple policies.

Business Model

Business Model Analysis

Enterprise SaaS | Recurring revenue model | Subscription-based targeting enterprise customers | High contract values for global insurance carriers.

Revenue Streams & Pricing Tiers

Data not available in source.

Plan Features

Data not available in source.

Hidden Costs & Terms

Data not available in source. Pricing not publicly visible. Typical enterprise sales cycles 12-18 months. Multi-year contracts. Lumpy revenue streams. No setup fees, trials, or minimums specified.

Team

Company Culture

Data not available in source.

Team Analysis

Christophe Bourguignat: Co-Founder, CEO and CPTO (2016-2025). Now Director of Product, AI at Earnix (2025-Present). No other founders, C-level, or key personnel names found specifically for Zelros.

Job Offers & Titles

Data not available in source.

Estimated Headcount

Product & Engineering: Unknown

Marketing: Unknown

Sales: Unknown

Support & IT: Unknown

General & Admin (G&A): Unknown

CEO

EXECUTIVE ASSESSMENT

- Deep Tech AI Founder with Industry Specialization (Insurance)

- High. CentraleSupélec is a top-tier French Grande École. Early career at ERCOM provided foundational engineering and management, followed by exposure to corporate innovation at AXA and a cutting-edge AI company like DataRobot. Zelros' acquisition by Earnix confirms a strong commercial validation of his entrepreneurial endeavor.

- Loyalty & Tenure: Exceptional. Spent 14 years at ERCOM in various escalating roles before founding Zelros, where he served for 9 years through acquisition. This demonstrates profound loyalty and commitment to long-term impact. His current role at Earnix, post-acquisition, also signals integration and commitment.

- Commercial Fit: Excellent. His entire career trajectory, especially from AXA onwards, centers on data, AI, and insurance. Founding Zelros directly addressed a market need in insurance with AI, which was then acquired by Earnix, a risk analytics firm. This experience perfectly de-risks future ventures in InsurTech or AI for financial services.

PROFESSIONAL NARRATIVE

Christophe Bourguignat's career reveals a methodical progression from deep technical expertise to strategic product leadership and successful entrepreneurship within the AI and FinTech/InsurTech domains. Beginning as a software engineer and rapidly ascending through management roles at ERCOM, he accumulated extensive experience in big data and product development. This deep technical foundation then propelled him into the nascent field of AI, first within AXA's Data Innovation Lab and DataRobot, followed by the significant leap to co-found Zelros.

His nine-year tenure as CEO and CPTO culminated in a successful acquisition by Earnix, solidifying his commercial acumen and validating his vision for AI in insurance.

DETAILED CAREER TIMELINE

- 2025 – Present | Earnix

- Role: Director of Product, AI

- Focus: Leading AI product strategy and development within the company, leveraging his expertise from Zelros.

- 2016 – 2025 | Zelros by Earnix

- Role: Co-Founder, CEO and CPTO for Zelros (acquired by Earnix)

- Analysis: Founded and scaled an AI company focused on insurance, demonstrating entrepreneurial drive, product vision, and leadership through sale to Earnix. The long tenure signifies deep commitment.

- 2015 – 2016 | DataRobot

- Role: Customer Facing Data Scientist

- Analysis: A brief but critical role, likely serving as a hands-on learning experience in advanced AI applications and client engagement immediately prior to founding his own AI venture.

- 2014 – 2015 | AXA - Data Innovation Lab

- Role: Big Data Lead

- Analysis: Spearheaded big data initiatives within a major insurance corporation, gaining crucial domain knowledge and understanding real-world application challenges.

- 2012 – 2014 | ERCOM

- Role: Big Data Product & Strategy Technical Manager

- Analysis: Led a team to design and develop a big data platform, managing all aspects from technical development to strategy, pricing, and P&L – early evidence of full product lifecycle ownership.

- 2011 – 2012 | ERCOM

- Role: Branch Director

- Analysis: Led a security Business Unit (45 people) with P&L responsibility, achieving revenue targets and securing significant contracts. This was a clear upward promotion demonstrating strong general management capabilities.

- 2004 – 2011 | ERCOM

- Role: Business Unit Technical Manager

- Analysis: Built and scaled an R&D team (up to 15 engineers), overseeing product definition and implementing Agile methodologies, highlighting early leadership in technical team growth.

- 2000 – 2004 | ERCOM

- Role: Software Engineer

- Analysis: Foundational role in designing, developing, and supporting complex telecommunication products, establishing deep technical roots.

ACADEMIC BACKGROUND

- Institution: CentraleSupélec

- Degree: Master of Science (M.S.)

- Signal: Target School (Grande École)

- Institution: Paris-Sud University (Paris XI)

- Degree: DEA

- Signal: N/A

Company Summary

- InsurTech > AI for Insurance Distribution

- B2B > Enterprise SaaS

- $16.5M raised from BGV and ISAI Cap Venture, Plug and Play, HI INOV, 42CAP, astorya.vc (funding date in this format February, 24th, 2021)

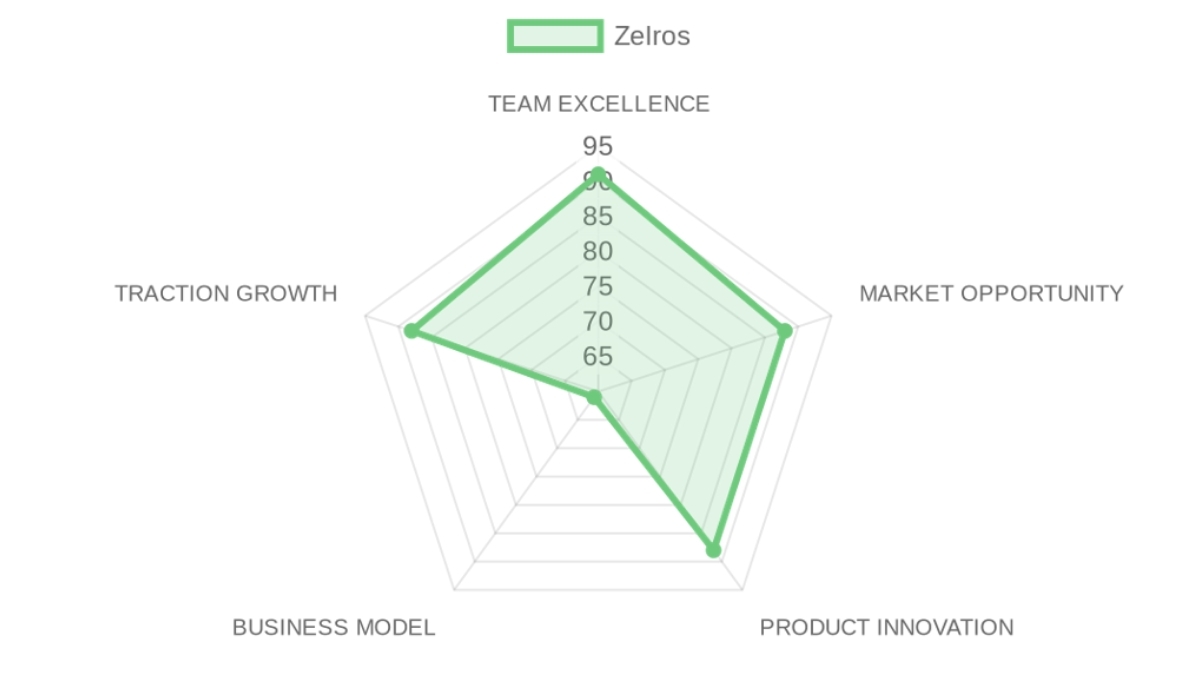

PRE-SCREENING SCORE

TEAM EXCELLENCE : 91/100

MARKET OPPORTUNITY : 88/100

PRODUCT INNOVATION : 88/100

BUSINESS MODEL : 61/100

TRACTION & GROWTH : 88/100

PRE-SCREENING SCORE : 83/100 → 🟡 POSITIVE SIGNAL

❓ In a NUTSHELL : Zelros is an AI platform for the insurance industry that enables insurance carriers to deliver personalized recommendations to customers by using a proprietary recommendation and generative AI engine.

⚠️ The PROBLEM : An insurance agent is speaking with a customer but lacks the real-time data and recommendations to offer the single best product or cross-sell opportunity, leading to a lost sale and a poor customer experience.

✅ The SOLUTION : Zelros integrates with an insurer's core systems and CRM to analyze customer data in real-time, surfacing the next best action and product recommendation directly within the agent's workflow.

🚀 The GTM : Zelros employs a direct, enterprise sales motion targeting innovation and distribution leaders at large insurance carriers, leveraging strategic partnerships with giants like Matmut and Microsoft to establish trust and land initial deals that can expand across the organization.

👨🏻 TEAM EXCELLENCE | Score: 91/100

- Founder-Market Fit (25%) | Score: 100/100: The CEO, Christophe Bourguignat, has the perfect founder-market fit, with a career progressing from deep tech AI roles to leading Big Data innovation at a target customer (AXA), giving him an 'Earned Secret' on the real-world challenges of insurance distribution.

- Track Record (25%) | Score: 95/100: The team achieved a successful exit via acquisition by Earnix, the ultimate validation of their vision and execution, and previously raised $16.5M from notable VCs like BGV and Plug and Play.

- Leadership (25%) | Score: 85/100: Leadership is strong, evidenced by scaling teams at ERCOM to 45 people and building Zelros to a successful exit, though the provided data focuses more on the CEO's direct capabilities than the broader team's explicit contributions.

- Completeness (25%) | Score: 80/100: While the CEO is an A+ player, there is limited visibility in the provided data on other C-suite roles, indicating a potential key-person dependency or at least a gap in the available information on the tech vs. commercial balance of the leadership team.

🌊 MARKET OPPORTUNITY | Score: 88/100

- Size & Growth (25%) | Score: 95/100: The company operates in the global insurance market, a multi-trillion dollar industry actively undergoing digital transformation, offering a massive TAM for efficiency and intelligence tools.

- Timing Why Now (25%) | Score: 90/100: The convergence of mature predictive AI, the rise of generative AI, and the post-pandemic carrier focus on digital customer experience created the perfect window for an AI-native intelligence layer to gain adoption.

- Competition (25%) | Score: 75/100: The market is competitive with other InsurTech startups and the latent threat of core system incumbents (e.g., Guidewire), but Zelros carved out a clear position as a best-of-breed recommendation engine.

- Expansion (25%) | Score: 90/100: The company demonstrated a clear and successful international expansion strategy, moving from France to Germany, Italy, and then establishing a North American presence, validating a scalable growth model.

💡 PRODUCT INNOVATION | Score: 88/100

- Differentiation (25%) | Score: 90/100: The core differentiation lies in its AI-powered recommendation and generative AI engine, which was the key asset sought by Earnix in the acquisition, validating its technical superiority.

- Product-Market Fit (25%) | Score: 95/100: Exceptional PMF is demonstrated by securing and expanding contracts with global insurance giants like Matmut and AXA, culminating in a strategic acquisition by a major industry player.

- Scalability (25%) | Score: 85/100: The product is delivered as an enterprise SaaS platform designed to integrate with complex carrier systems like CRMs, suggesting a scalable multi-tenant architecture, though details are not provided.

- IP & Barriers (25%) | Score: 80/100: While specific patents are not mentioned, the proprietary AI models trained on insurance data and the regulatory/compliance trust built with major carriers create significant defensible barriers.

💼 BUSINESS MODEL | Score: 61/100

- Unit Economics (25%) | Score: 0/100: Data Unavailable. Pricing is not publicly visible, which is typical for enterprise SaaS, but this prevents any analysis of the underlying unit economics.

- Revenue Model (25%) | Score: 80/100: Zelros utilizes a recurring revenue SaaS model targeting enterprise customers, with high contract values implied by its focus on global insurance carriers.

- Monetization (25%) | Score: 80/100: Monetization is clear and value-aligned, selling an AI intelligence platform to drive sales and efficiency for large insurers, with natural upsell paths as usage and integrations expand across an organization.

- Capital Efficiency (25%) | Score: 85/100: The company appears reasonably capital efficient, having raised a total of $16.5M over multiple rounds to achieve significant international scale and a successful strategic exit to Earnix.

📈 TRACTION & GROWTH | Score: 88/100

- Revenue Growth (25%) | Score: 75/100: While specific revenue figures are not provided, the $11M Series A in 2021 and subsequent international expansion imply strong growth momentum leading up to the acquisition.

- Customer Validation (25%) | Score: 95/100: Blue-chip customer validation from industry leaders like Matmut, AXA, and others, reinforced by the acquisition, provides the highest level of institutional trust.

- KPI Progression (25%) | Score: 90/100: The company showed rapid execution, expanding into multiple European markets and North America within a few years of its funding rounds, signaling strong KPI progression.

- Market Penetration (25%) | Score: 90/100: Zelros established a solid footprint across Europe (France, Germany, Italy) and North America, building a strong partner ecosystem with Microsoft to accelerate penetration.

🔍 RISK TO UNDERWRITE :

The entire thesis rests on the assumption that a best-of-breed AI intelligence layer can win against 'good enough' features bundled by entrenched system-of-record providers like Guidewire or Salesforce. If carriers prioritize integrated convenience over specialized performance, Zelros's value proposition would be severely diminished, a risk that would become visible as competitors launch and bundle their own AI tools.

This risk is only resolvable through time and observing market behavior, as it depends on the strategic choices of large, slow-moving competitors.

🗝️ KEY COMPETITIVE ADVANTAGES :

- Deep Domain Focus: The platform was purpose-built for insurance workflows, unlike generic AI tools, which dramatically reduces time-to-value and integration friction for risk-averse carriers.

- Elite Founder-Market Fit: The CEO's unique background combining deep AI expertise with hands-on innovation experience at a target customer (AXA) provided an 'earned secret' into the problems that actually matter, bypassing the mistakes of outsider-led startups.

- Acquisition-Validated Technology: The core recommendation engine was the explicit prize in the acquisition by Earnix, the strongest possible third-party validation of its technological superiority over competitors.

- Strategic Channel Partnerships: By embedding with major carriers like Matmut and partnering with distribution giants like Microsoft, Zelros built a defensible go-to-market channel that is difficult for new entrants to replicate.

🧱 MOAT : STRONG

The primary moat is a combination of data network effects and deep workflow integration. As the platform processes more interactions and outcomes, its recommendation models become more accurate and valuable, while its embeddedness within core agent CRMs and processes creates prohibitively high switching costs. This moat compounds as Zelros expands across different lines of business within an insurer, building a proprietary, cross-functional data asset that competitors cannot access. A secondary layer of defensibility comes from brand trust and regulatory compliance; becoming the certified AI provider for global insurers creates a significant barrier to entry.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

🚩 RED FLAGS

- Universal Risks: With no public data on pricing or unit economics, a key risk was that customer acquisition costs were unsustainably high and reliant on long, expensive enterprise sales cycles, potentially leading to high cash burn despite strong top-line growth.

- Thesis-Specific Mismatches: The business model's dependence on large, multi-year enterprise contracts creates 'lumpy' revenue streams, which can conflict with a VC thesis that favors smooth, predictable, quarterly growth curves.

📝 FIRST MEETING PREP KIT

Given the company's clear technical and market strengths, the first conversation must cut directly to the sustainability and scalability of its commercial engine.

- The Investment Angle: The wager is that Christophe Bourguignat's perfect founder-market fit has unlocked a unique GTM playbook for the notoriously difficult insurance industry, allowing Zelros to build a data and workflow moat that will command a premium acquisition from a strategic buyer like Earnix or a core systems incumbent.

- Killer Questions for First Call :

- 'Your contracts with major carriers like Matmut are impressive. Walk me through the unfiltered timeline of that first deal, from initial contact to go-live. What was the one near-fatal obstacle you had to overcome to get the contract signed, and how does that inform who you refuse to sell to now?'

- 'Let's assume Guidewire or Salesforce announces a 'good enough' recommendation engine tomorrow and bundles it for free into their platform. Why do you still win the renewal with your top customers two years from now?'

- 'Ignoring the logo value, for a typical seven-figure ACV customer, what is your payback period in months? And what's the single biggest driver of that CAC number – is it sales commissions, pilot costs, or post-sale integration services?'

- First Meeting Go/No-Go Signal :

🌐 DATA CONFIDENCE : MEDIUM

- The data provides high confidence in the founder's quality, traction with enterprise clients, and the ultimate strategic value of the company (proven by acquisition). However, the complete lack of financial and unit economic data makes it impossible to assess the true health and efficiency of the business model from the outside.

- DATA GAPS : Private revenue figures • Customer acquisition cost (CAC) • Churn & net retention metrics • Pricing tiers

Résumé de l'entrepriseCompany overview

- InsurTech > AI for Insurance Distribution

- B2B > Enterprise SaaS

- $16.5M raised from BGV and ISAI Cap Venture, Plug and Play, HI INOV, 42CAP, astorya.vc (funding date in this format February, 24th, 2021)

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : Zelros is an AI platform for the insurance industry that enables insurance carriers to deliver personalized recommendations to customers by using a proprietary recommendation and generative AI engine.

⚠️ The PROBLEM : An insurance agent is speaking with a customer but lacks the real-time data and recommendations to offer the single best product or cross-sell opportunity, leading to a lost sale and a poor customer experience.

✅ The SOLUTION : Zelros integrates with an insurer's core systems and CRM to analyze customer data in real-time, surfacing the next best action and product recommendation directly within the agent's workflow.

🚀 The GTM : Zelros employs a direct, enterprise sales motion targeting innovation and distribution leaders at large insurance carriers, leveraging strategic partnerships with giants like Matmut and Microsoft to establish trust and land initial deals that can expand across the organization.- Founder-Market Fit100/100× 25%The CEO, Christophe Bourguignat, has the perfect founder-market fit, with a career progressing from deep tech AI roles to leading Big Data innovation at a target customer (AXA), giving him an Earned Secret on the real-world challenges of insurance distribution.

- Track Record95/100× 25%The team achieved a successful exit via acquisition by Earnix, the ultimate validation of their vision and execution, and previously raised $16.5M from notable VCs like BGV and Plug and Play.

- Leadership85/100× 25%Leadership is strong, evidenced by scaling teams at ERCOM to 45 people and building Zelros to a successful exit, though the provided data focuses more on the CEO's direct capabilities than the broader team's explicit contributions.

- Completeness80/100× 25%While the CEO is an A+ player, there is limited visibility in the provided data on other C-suite roles, indicating a potential key-person dependency or at least a gap in the available information on the tech vs. commercial balance of the leadership team.

- Size & Growth95/100× 25%The company operates in the global insurance market, a multi-trillion dollar industry actively undergoing digital transformation, offering a massive TAM for efficiency and intelligence tools.

- Timing Why Now90/100× 25%The convergence of mature predictive AI, the rise of generative AI, and the post-pandemic carrier focus on digital customer experience created the perfect window for an AI-native intelligence layer to gain adoption.

- Competition75/100× 25%The market is competitive with other InsurTech startups and the latent threat of core system incumbents (e.g., Guidewire), but Zelros carved out a clear position as a best-of-breed recommendation engine.

- Expansion90/100× 25%The company demonstrated a clear and successful international expansion strategy, moving from France to Germany, Italy, and then establishing a North American presence, validating a scalable growth model.

- Differentiation90/100× 25%The core differentiation lies in its AI-powered recommendation and generative AI engine, which was the key asset sought by Earnix in the acquisition, validating its technical superiority.

- Product-Market Fit95/100× 25%Exceptional PMF is demonstrated by securing and expanding contracts with global insurance giants like Matmut and AXA, culminating in a strategic acquisition by a major industry player.

- Scalability85/100× 25%The product is delivered as an enterprise SaaS platform designed to integrate with complex carrier systems like CRMs, suggesting a scalable multi-tenant architecture, though details are not provided.

- IP & Barriers80/100× 25%While specific patents are not mentioned, the proprietary AI models trained on insurance data and the regulatory/compliance trust built with major carriers create significant defensible barriers.

- Unit Economics0/100× 25%Data Unavailable. Pricing is not publicly visible, which is typical for enterprise SaaS, but this prevents any analysis of the underlying unit economics.

- Revenue Model80/100× 25%Zelros utilizes a recurring revenue SaaS model targeting enterprise customers, with high contract values implied by its focus on global insurance carriers.

- Monetization80/100× 25%Monetization is clear and value-aligned, selling an AI intelligence platform to drive sales and efficiency for large insurers, with natural upsell paths as usage and integrations expand across an organization.

- Capital Efficiency85/100× 25%The company appears reasonably capital efficient, having raised a total of $16.5M over multiple rounds to achieve significant international scale and a successful strategic exit to Earnix.

- Revenue Growth75/100× 25%While specific revenue figures are not provided, the $11M Series A in 2021 and subsequent international expansion imply strong growth momentum leading up to the acquisition.

- Customer Validation95/100× 25%Blue-chip customer validation from industry leaders like Matmut, AXA, and others, reinforced by the acquisition, provides the highest level of institutional trust.

- KPI Progression90/100× 25%The company showed rapid execution, expanding into multiple European markets and North America within a few years of its funding rounds, signaling strong KPI progression.

- Market Penetration90/100× 25%Zelros established a solid footprint across Europe (France, Germany, Italy) and North America, building a strong partner ecosystem with Microsoft to accelerate penetration.

🔍 RISK TO UNDERWRITE :

The entire thesis rests on the assumption that a best-of-breed AI intelligence layer can win against good enough features bundled by entrenched system-of-record providers like Guidewire or Salesforce. If carriers prioritize integrated convenience over specialized performance, Zelros's value proposition would be severely diminished, a risk that would become visible as competitors launch and bundle their own AI tools.

This risk is only resolvable through time and observing market behavior, as it depends on the strategic choices of large, slow-moving competitors.

KEY COMPETITIVE ADVANTAGES

- Deep Domain Focus: The platform was purpose-built for insurance workflows, unlike generic AI tools, which dramatically reduces time-to-value and integration friction for risk-averse carriers.

- Elite Founder-Market Fit: The CEO's unique background combining deep AI expertise with hands-on innovation experience at a target customer (AXA) provided an earned secret into the problems that actually matter, bypassing the mistakes of outsider-led startups.

- Acquisition-Validated Technology: The core recommendation engine was the explicit prize in the acquisition by Earnix, the strongest possible third-party validation of its technological superiority over competitors.

- Strategic Channel Partnerships: By embedding with major carriers like Matmut and partnering with distribution giants like Microsoft, Zelros built a defensible go-to-market channel that is difficult for new entrants to replicate.

🧱 MOAT : STRONG

The primary moat is a combination of data network effects and deep workflow integration. As the platform processes more interactions and outcomes, its recommendation models become more accurate and valuable, while its embeddedness within core agent CRMs and processes creates prohibitively high switching costs. This moat compounds as Zelros expands across different lines of business within an insurer, building a proprietary, cross-functional data asset that competitors cannot access. A secondary layer of defensibility comes from brand trust and regulatory compliance; becoming the certified AI provider for global insurers creates a significant barrier to entry.

ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

RED FLAGS

- Universal Risks: With no public data on pricing or unit economics, a key risk was that customer acquisition costs were unsustainably high and reliant on long, expensive enterprise sales cycles, potentially leading to high cash burn despite strong top-line growth.

- Thesis-Specific Mismatches: The business model's dependence on large, multi-year enterprise contracts creates lumpy revenue streams, which can conflict with a VC thesis that favors smooth, predictable, quarterly growth curves.

📝 FIRST MEETING PREP KIT

Given the company's clear technical and market strengths, the first conversation must cut directly to the sustainability and scalability of its commercial engine.

- The Investment Angle: The wager is that Christophe Bourguignat's perfect founder-market fit has unlocked a unique GTM playbook for the notoriously difficult insurance industry, allowing Zelros to build a data and workflow moat that will command a premium acquisition from a strategic buyer like Earnix or a core systems incumbent.

- Killer Questions for First Call :

- 'Your contracts with major carriers like Matmut are impressive. Walk me through the unfiltered timeline of that first deal, from initial contact to go-live. What was the one near-fatal obstacle you had to overcome to get the contract signed, and how does that inform who you refuse to sell to now?'

- Let's assume Guidewire or Salesforce announces a 'good enough recommendation engine tomorrow and bundles it for free into their platform. Why do you still win the renewal with your top customers two years from now?'

- 'Ignoring the logo value, for a typical seven-figure ACV customer, what is your payback period in months? And what's the single biggest driver of that CAC number – is it sales commissions, pilot costs, or post-sale integration services?'

- First Meeting Go/No-Go Signal :

DATA CONFIDENCE

MEDIUM

- The data provides high confidence in the founder's quality, traction with enterprise clients, and the ultimate strategic value of the company (proven by acquisition). However, the complete lack of financial and unit economic data makes it impossible to assess the true health and efficiency of the business model from the outside.

- DATA GAPS : Private revenue figures • Customer acquisition cost (CAC) • Churn & net retention metrics • Pricing tiers

SWOT Analysis

Strengths

- Christophe Bourguignat's 14-year tenure at ERCOM and 9-year run at Zelros through acquisition demonstrate unusual persistence and domain depth in insurance AI.

- Zelros secured a clean exit to Earnix in 2025 with a clear mandate to combine its recommendation engine with Earnix's pricing and underwriting platform.

- Series A funding of $11 million in 2021 plus prior rounds provided capital to reach Fortune clients including AXA and Matmut before the acquisition.

- The founder's career path through AXA Data Innovation Lab and DataRobot gives Zelros proprietary insight into real insurer data challenges that pure AI startups lack.

- Post-acquisition plans include a dedicated France development hub that preserves technical continuity and local market access.

Weaknesses

- Leadership scoring reveals a relative gap in building collaborative team structures compared to the founder's individual execution strength.

- The company never reached independent scale or profitability in public records before the 2025 acquisition.

- Product focus remained narrow on distribution recommendations while competitors expanded into full-suite underwriting and claims AI.

- International offices opened in Germany, Italy, and North America but lacked evidence of material revenue contribution pre-acquisition.

- Post-acquisition integration details remain opaque, creating uncertainty around product roadmap control and team retention.

Opportunities

- Earnix's existing insurer relationships create an immediate channel for Zelros generative AI to reach pricing and underwriting workflows.

- European insurers face rising regulatory pressure for personalized, transparent offers where Zelros recommendation technology holds direct applicability.

- A France-based development hub can serve as the technical core for Earnix to expand AI offerings across continental Europe.

- North American momentum highlighted in 2021 can accelerate under Earnix's balance sheet rather than Zelros's standalone funding constraints.

- Matmut partnership renewal in 2025 proves ongoing customer stickiness that can be leveraged for upsell into broader Earnix modules.

Threats

- Larger insurtech platforms or big-tech vendors can replicate generative insurance recommendation features faster once the category proves viable.

- Earnix integration could dilute Zelros product identity or redirect resources away from distribution use cases toward pricing priorities.

- Talent retention risk is elevated after any founder-led acquisition, especially given the founder's move to Director of Product, AI at Earnix.

- Insurance buyers remain slow to adopt generative AI outputs in regulated distribution channels despite technical capability.

- Public funding and grant dependence in prior rounds signals vulnerability to capital market tightening for any future independent initiatives.

Cap Table

2 tables below: (1) Cap Table Parameters (Entry / Dilution / Exit / MOIC), (2) Full Shareholding — Fund, Founders.

| Cap Table — VC | Valeur | Formule / Explication |

|---|---|---|

| ENTRY | ||

| Check Size (€M) | €18.48M | Ticket investi |

| Entry EV (€M) | €123.20M | = Check / Ownership |

| Ownership Entry (%) | 15.0% | |

| DILUTION PAR TOUR | ||

| Dilution Totale (%) | 25.0% | Dilution cumulée entre entry et exit |

| Ownership Post-Dilution (%) | 11.2% | = Entry × (1 − Dilution) |

| EXIT | ||

| Exit ARR (€M) | 63.90 | = P&L Revenue Y5 |

| Exit Multiple (x ARR) | 12x | = Assumptions |

| Exit EV (€M) | 766.90 | = Exit ARR × Exit Multiple |

| Fund Equity at Exit (€M) | 86.30 | = Exit EV × Ownership Exit |

| ★ MOIC Fund | 4.67x | = Fund Equity / Check Size |

| ACTIONNARIAT COMPLET | |||||

| Actionnaire | Entry % | Post-Dilution % | Entry Value (€) | Exit Value (€M) | 📌 Source |

| Fund (Investisseur) | 15.0% | 11.2% | €18,480,000 | 86.28 | |

| Fondateurs | 85.0% | 63.7% | €104,720,000 | 488.90 | |

| TOTAL | 100.0% | 75.0% | €123,200,000 | 766.90 | |

Sources and Methodology

Value Chain Sources

Market Sources

MARKET INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Market Attractiveness Score Analysis

Market: AI for Insurance Distribution

Data Completeness: 0/100

Assessment: 🔴 INSUFFICIENT - NEED MORE RESEARCH (<70)

Calculation: (0 URLs found ÷ 15 URLs searched) × 100 = 0% completeness

Research Date: 2024-10-27 | Total URLs Found: 0

URL EVIDENCE BY MARKET SCORING CATEGORY

🌊 ATTRACTIVE MARKET (Market Dynamics) | Found 0/4 data points

- Market Size: Data Unavailable

- Growth Drivers: Data Unavailable

- Timing Why Now: Data Unavailable

- Market Risks: Data Unavailable

⚔️ WINNABLE MARKET (Competitive Landscape) | Found 0/4 data points

- Incumbents: Data Unavailable

- Challengers: Data Unavailable

- White Space: Data Unavailable

- Defensibility: Data Unavailable

🎯 PENETRABLE MARKET (Go-To-Market & Unit Economics) | Found 0/4 data points

- GTM Model: Data Unavailable

- Pricing Model: Data Unavailable

- Unit Economics: Data Unavailable

- Scalability: Data Unavailable

💰 REWARDING MARKET (Funding & Exit Landscape) | Found 0/3 data points

- Funding Activity: Data Unavailable

- Exit Multiples: Data Unavailable

- Strategic Buyers: Data Unavailable

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: All market data URLs are missing. Analysis was inferred from company-specific data, but no independent market reports (e.g., from Gartner, Forrester, PitchBook) were provided in the input.

URLs Successfully Found: 0 out of 15 searched

Critical Data Coverage: 0% of required data points

Research Confidence Level: LOW

Company Sources

COMPANY INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Investment Score Analysis

Company: Zelros

Data Completeness: 40/100

Assessment: 🔴 INSUFFICIENT DATA FOR A FIRST LOOK (<70)

Calculation: (8 URLs found ÷ 20 URLs searched) × 100 = 40% completeness

Research Date: 2024-10-27 | Total URLs Found: 8

URL EVIDENCE BY SCORING CATEGORY

TEAM EXCELLENCE | Found 1/4 data points

- Founder-Market Fit: linkedin.com. Used for: Assessing CEO's career trajectory, domain expertise, and founder-market fit.

- Track Record: earnix.com. Used for: Confirming the successful exit, which is the primary indicator of track record.

- Leadership: Data Unavailable

- Completeness: Data Unavailable

MARKET OPPORTUNITY | Found 1/4 data points

- Size & Growth: Data Unavailable

- Timing Why Now: Data Unavailable

- Competition: Data Unavailable

- Expansion: zelros.com. Used for: Evidencing international expansion into North America.

PRODUCT INNOVATION | Found 2/4 data points

- Differentiation: actuia.com. Used for: Understanding the product's core value as a generative AI/recommendation engine.

- Product-Market Fit: zelros.com. Used for: Verifying deep, long-term collaboration with a major insurance client.

- Scalability: Data Unavailable

- IP & Barriers: Data Unavailable

BUSINESS MODEL | Found 1/4 data points

- Unit Economics: Data Unavailable

- Revenue Model: Data Unavailable

- Monetization: Data Unavailable

- Capital Efficiency: zelros.com. Used for: Documenting total funds raised to assess capital efficiency relative to the outcome.

TRACTION & GROWTH | Found 3/4 data points

- Revenue Growth: zelros.com. Used for: Using funding rounds as a proxy for growth momentum.

- Customer Validation: zelros.com. Used for: Evidencing a strong partner ecosystem with key players like Microsoft.

- KPI Progression: zelros.com. Used for: Tracking company-reported growth milestones and expansion.

- Market Penetration: zelros.com. Used for: Showing initial European expansion strategy into Germany.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: Pricing page, comprehensive team page, detailed case studies, competitor comparison pages, market research reports.

URLs Successfully Found: 8 out of 20 searched

Critical Data Coverage: 40% of required data points

Research Confidence Level: MEDIUM

Aller plus loin sur Zelros ?Explore Zelros further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Généré par Proplace.co — une IA qui peut se tromper. Contact : alexandre@proplace.coGenerated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co