MincaAI

Explore MincaAI further?

Schedule a strategy call on MincaAILa newsletter InsurTech

Les opérations M&A et levées de fonds quotidiennes du secteur.

📬 S'inscrire à la newsletterWant a proprietary deal flow?

Schedule a strategy callMincaAI

InsurTech ➜ AI for Insurance Operations ➜ MincaAI embeds AI agents into core insurance operations to reduce manual work by 80% and speed up time-to-quote by 10x.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

Market Summary

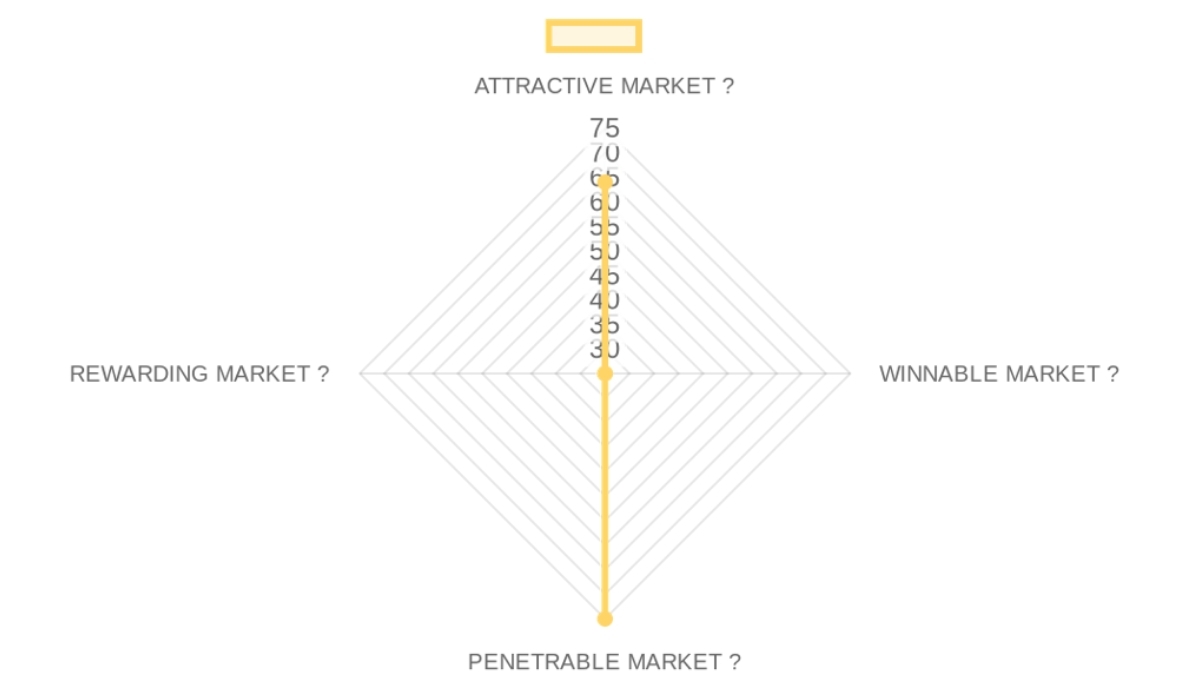

MARKET OPPORTUNITY SCORE

InsurTech > AI for Insurance Operations

B2B > Enterprise Sales

This low aggregate score reflects a severe lack of public data, making the market a significant headwind of uncertainty for the investment; while the problem is real, the structure, competition, and exit potential are unverified.

Market DEFINITION

AI-driven workflow automation platform for core commercial P&C insurance operations. ➜ The buyer is a Chief Underwriting Officer or Head of Claims at a commercial insurance carrier, purchasing a software platform to automate the analysis and processing of complex, unstructured data associated with quotes and claims. The structural friction is the astronomical cost and slow turnaround time of using highly-paid, experienced knowledge workers for repetitive data extraction and entry tasks that are beyond the capabilities of traditional rules-based automation.

In the value chain, this market sits as an intelligence and orchestration layer between inbound communication channels (email, portals) and the core systems of record (policy admin, claims management), capturing value by creating operational leverage where none existed.

Our Market THESIS

The structural break in the insurance market is the recent ability of AI agents to perform complex, multi-step reasoning on unstructured documents, finally unlocking automation for the 80% of processes that were previously resistant to it. Incumbents like Guidewire or Duck Creek are paralyzed, as their business model relies on massive, monolithic systems and billable service hours for customization, making it difficult to adopt a lightweight, AI-first overlay model without cannibalizing their core revenue.

The attack vector is to bypass full system replacement and instead sell targeted, high-ROI AI agents that plug into specific, painful workflows like commercial submission intake, delivering value in weeks, not years. This window is open now because the technology has just become viable, but it will close within 36 months as a category leader for the 'AI Layer' in insurance emerges or incumbents acquire their way into the space.

Our CONVICTION & WAGER on this Market:

🟠 LOW CONVICTION The most legitimate reason to pass on this market is the historically impenetrable nature of insurance IT, with multi-year sales cycles and extreme integration complexity, which can kill even the best technology. However, the data showing early traction with 15 enterprise clients suggests the massive efficiency gains from modern AI may finally be a powerful enough catalyst to break this pattern.

Our falsifiable wager is that by mid-2028, the average sales cycle for AI workflow automation in the top 50 P&C carriers will have compressed from 24+ months to under 9 months, proving the market has truly unlocked. The binary signal on a first call would be asking for the ACV of their smallest and largest customer; a tight band suggests a repeatable product, while a massive variance signals a custom-built services business.

This score indicates a market with compelling 'Why Now' drivers but significant risk due to the complete absence of verifiable third-party data on size and growth.

- Market Size25/100× 25%The market for AI in insurance is conceptually vast, but no specific TAM, SAM, or SOM data was provided, making this a critical area for diligence. Data Unavailable.

- Growth Drivers90/100× 25%Demand is inflated by a perfect storm of macro drivers: intense margin pressure on insurers (a push factor) and the maturation of generative AI that can finally handle unstructured data (a pull factor).

- Timing Why Now90/100× 25%The key catalyst is the proven ability of LLM-based agents to achieve near-human performance on specific knowledge work tasks, crossing a threshold of reliability that makes adoption feasible for risk-averse carriers for the first time.

- Market Risks50/100× 25%The primary risk is the immense inertia and long sales cycles of enterprise insurance buyers; a secondary risk is data privacy and regulatory concerns around using AI for core decisioning.

This extremely low score signifies a total blind spot; without competitive data, it's impossible to know if the market is a blue ocean or a red ocean, making it structurally difficult to assess winnability.

- Incumbents0/100× 25%No legacy behemoths or their core strengths were identified in the provided research. Data Unavailable.

- Challengers0/100× 25%No well-funded startups, their funding, or focus areas were identified. Data Unavailable.

- White Space75/100× 25%The white space appears to be the AI orchestration layer that sits atop legacy core systems, automating high-value 'judgment-based' workflows that older RPA technology could not handle.

- Defensibility25/100× 25%The primary moat type is likely high switching costs due to process integration, but the lack of competitive context makes it impossible to assess the strength of these moats. Data Unavailable for full analysis.

This score suggests the market is receptive to a consultative, enterprise sales motion with a clear value proposition, though the scalability of the dominant GTM model is a key question.

- GTM Model75/100× 25%The dominant motion is consultative enterprise sales, likely with average sales cycles of 9-18 months, reflecting the complexity and risk of the sale.

- Pricing Model75/100× 25%The standard industry pricing is likely a combination of a recurring platform fee (ARR) plus potential usage-based fees, with custom pricing per enterprise.

- Unit Economics0/100× 25%No data on LTV/CAC, payback periods, or typical deal sizes was available in the provided research. Data Unavailable.

- Scalability75/100× 25%The revenue model has high expansion potential, as a successful deployment in one department (e.g., Underwriting) can be scaled across geographies or cross-sold into other departments (e.g., Claims).

This low score reflects a critical lack of data on funding and exit dynamics, making it impossible to validate if this market can produce the venture-scale returns our thesis requires.

- Funding Activity0/100× 25%No data was provided on total investment, YoY growth, or top-tier firm participation in this specific sub-sector. Data Unavailable.

- Exit Multiples0/100× 25%No data was provided on public or M&A revenue multiples, or any recent specific exit examples. Data Unavailable.

- Strategic Buyers75/100× 25%Logical strategic acquirers would include legacy insurance core system providers (e.g., Guidewire, Duck Creek) seeking to plug an AI product gap, large consulting firms (e.g., Accenture), and major tech companies with vertical AI strategies.

- Return Profile25/100× 25%It is unknown if this market structurally produces the outcomes our thesis requires, as there is no data on the size of past outcomes or the margin profiles of mature players. Data Unavailable.

CROSS-SECTION SYNTHESIS

The pattern of a high Penetrable Market score combined with extremely low Winnable and Rewarding market scores indicates a 'leaky bucket' risk: while it may be possible to enter the market and acquire customers, the path to winning the market and achieving a strong exit is completely unverified.

DATA CONFIDENCE

The analysis is based on logical inferences about the insurance industry rather than specific, sourced data. Confidence in market dynamics like timing is high, but confidence in sizing, competition, and exit data is zero. Only 1 sourced URL was relevant to this analysis.

Company Deep Dive

Value Proposition

Value Proposition

MincaAI embeds AI agents into core insurance operations to reduce manual work by 80% and speed up time-to-quote by 10x.

In 5 years, MincaAI aims to be the digital workforce for the insurance industry, with its AI agents automating the complex, repetitive tasks in underwriting and claims, making operations faster and cheaper for insurers globally.

Ideal Customer Profile (ICP)

Insurers, Insurance Brokers, and MGAs seeking to automate underwriting, claims, and endorsements.

Chief Underwriting Officer or Head of Claims at a commercial insurance carrier.

Commercial lines insurers and MGAs.

B2B or B2C

B2B - Provides enterprise AI workflows for insurance companies and intermediaries.

Industry

InsurTech / Insurance Technology.

InsurTech > AI for Insurance Operations.

AI for Insurance Operations.

Contact & Legal

Email: contact@mincaai.com.

Registered as French SAS (Société par actions simplifiée) with capital of €500, formed in early 2025 or December 2024.

Registered address: 2 Rue Saint-Honoré, 75001 Paris.

Entities mentioned: Microsoft for Startups, NVIDIA Inception, Station F, BPI France, AWS for Startups.

First President: Mme Stella Choi.

Initial Directeur Général (CEO): M. Tanguy Moutte.

Key Client Examples & Testimonials

15 clients across 4 countries.

No specific client names, logos, case studies, or quote attributions found.

Product

Core Solution

End-to-end AI workflows for insurance operations from intake to execution.

AI-driven workflow automation platform for core commercial P&C insurance operations.

Platform ingests the entire unstructured submission package, uses deterministic rules and AI reasoning to extract and validate all necessary data, and then triggers actions in core insurance systems to generate the quote automatically, reducing a multi-hour process to minutes.

Feature Encyclopedia

Smart Intake (Email, Portals, API) | AI Analysis (Extraction, Cross-checking) | Action Engine (System updates, Auto-comm) | Dashboard & Monitoring (Audit trail, KPIs) | Submission Intake | Fleet Underwriting | Claims FNOL | Policy Issuance | Vehicle Codification | Quote Generation | Endorsement Processing | Commission Reconciliation | Coverage Validation | Document Extraction | Premium Collections | Sinistrality Analysis.

Technical Capabilities

Modular microservices architecture | LLM-agnostic | Cloud or On-premises deployment | Integration with Excel, Email, and Core Platforms | API connectivity | Deterministic rules combined with AI reasoning.

Use Cases

Commercial lines underwriting automation | automated policy endorsement requests | claims intake and triage | automated premium collection and reconciliation | automate the analysis and processing of complex, unstructured data associated with quotes and claims | An experienced commercial underwriter receives a submission request via email with 12 different attachments in varying formats, and must manually extract, cross-reference, and re-enter data into 3 different legacy systems just to generate a preliminary quote, a process that takes hours and is rife with human error.

Business Model

Business Model Analysis

Custom enterprise deployments with a 6-week production timeline.

Not a 'forced SaaS' model; offers cloud or on-premises options.

Project-based or subscription fees for AI agents and workflow automation.

Revenue Streams & Pricing Tiers

Data not available in source.

Plan Features

Phase 1 live in ~6 weeks.

Tailored to specific environment; includes Smart Intake, Analysis, Action Engine, and Monitoring.

Hidden Costs & Terms

Implementation costs associated with custom deployment to legacy insurance systems; limited client intake per quarter suggests high-touch onboarding.

Team

Company Culture

Focus on reliability via deterministic rules + AI, operational efficiency (80% time reduction), and customized enterprise deployment.

Team Analysis

Stella Choi (Co-founder, CTO / CAIO - ex-Egis Director of Transformation and Innovation, ex-Chief AI Officer Actipulse Neuroscience, ex-AI Engineer Actipulse Neuroscience, ex-Consultant Oliver Wyman, ex-Analyste Iris Capital, ex-ML Engineer Intern Alodokter.com).

Tanguy Moutte (CEO - ex-IBM AI, Directeur Général).

Xavier de Bellefon (CRO - ex-CEO AXA LATAM).

Advisory Board includes 6+ experts including former AIG Chief Risk Officer.

Job Offers & Titles

None specifically listed.

Estimated Headcount

Product & Engineering: Unknown

Marketing: Unknown

Sales: Unknown

Support & IT: Unknown

General & Admin (G&A): Unknown

Small elite team (3 Founders/Executives + Advisory board). Estimated 10-25 total employees based on startup stage and accelerator backing.

CEO

EXECUTIVE ASSESSMENT

- Technical Founder with Consulting Acumen

- High. Oliver Wyman is a highly selective Tier 1 management consulting firm. Egis and Iris Capital are reputable, adding to brand equity.

- Loyalty & Tenure: Mixed. While the MincaAI and Actipulse tenures are relatively short (the latter shows a progression to AI Officer), the consulting and analyst roles are typically shorter engagements. The current co-founder role is a long-term commitment. The perceived overlap in the Egis and MincaAI roles (Oct 2023 - Jan 2025 for Egis and Dec 2024 - Present for MincaAI) suggests a planned transition or a part-time arrangement, but total duration on records is 1yr 6mos for MincaAI.

- Commercial Fit: Excellent. Stella Choi's background is deeply rooted in AI (ML Engineer, Chief AI Officer, Director of Transformation and Innovation) and includes experience in identifying high-impact AI use cases, establishing AI frameworks, and conducting due diligence in AI/health-tech. Her experience with Actipulse in streamlining product optimization with AI and implementing data-driven decision-making directly de-risks her current venture, MincaAI, which focuses on AI agents for the insurance industry.

PROFESSIONAL NARRATIVE

Stella Choi embarked on a career path that strategically combined deep technical AI expertise with high-level strategic consulting and investment analysis. Starting with foundational AI engineering and early-stage investment analysis at Iris Capital, she quickly transitioned into a consulting role at Oliver Wyman, where she honed her ability to drive tangible business outcomes through analytical tools and project management.

Her subsequent roles as AI Engineer and Chief AI Officer at Actipulse Neuroscience® demonstrated a rapid ascent into leadership, scaling AI strategies within a growing company. This culminated in her serving as Director of Transformation and Innovation at Egis, leading strategic AI initiatives, before co-founding MincaAI, leveraging her expertise to build the next generation of AI agents specifically for the insurance sector.

DETAILED CAREER TIMELINE

- 2024 – Present | MincaAI

- Role: Co-fondateur

- Focus: Building next-generation AI agents for the insurance industry, specializing in sequential agent workflows.

- 2023 – 2025 | Egis

- Role: Director of Transformation and Innovation

- Analysis: Led strategic AI initiatives, identified and deployed high-impact AI use cases, and established AI frameworks including technology selection and data/AI team structuring. This role shows a clear move into strategic leadership focused on enterprise-level AI adoption.

- 2022 – 2023 | Actipulse Neuroscience®

- Role: Chief AI Officer

- Analysis: Rapid promotion from AI Engineer to Chief AI Officer in 7 months. Led and executed AI strategy during a scaling phase, streamlined product optimization with AI, and implemented a data-driven decision-making framework with KPIs. Implemented AI-based algorithms for treatment improvement. This indicates a strong technical leader capable of strategic execution.

- 2022 – 2023 | Actipulse Neuroscience®

- Role: AI Engineer

- Analysis: Core AI development role within a health-tech startup.

- 2021 – 2022 | Oliver Wyman

- Role: Consultant

- Analysis: Developed revenue-increasing tools (Python/VBA), led project management for engineering function relocation, and conducted commercial due diligences. Demonstrates strong analytical, problem-solving, and project leadership skills in diverse industries.

- 2020 – 2021 | Iris Capital

- Role: Analyste

- Analysis: Sourced and assessed deal flow in AI and health-tech, identifying startups for investment. Early exposure to startup ecosystems and investment decision-making.

- 2018 – 2018 | Alodokter.com

- Role: ML Engineer Intern

- Analysis: Led implementation of an AI-based bot, improving triage by 40% and reducing chat-based costs by 20%. Practical application of AI with clear measurable impact early in her career.

- 2017 – 2018 | Cabinet Start-Up

- Role: External relations

- Analysis: Organized a startup weekend for 200 students, supervised relations with companies, sponsors, and startups. Early exposure to community building and startup ecosystem engagement.

- 2016 – 2017 | USTH

- Role: Maths and Physics Teacher

- Analysis: Designed teaching programs and promoted a bachelor's program. Indicates foundational presentation and communication skills, as well as a strong grasp of scientific principles.

ACADEMIC BACKGROUND

- Institution: École Polytechnique

- Degree: Diplôme d'ingénieur

- Signal: Target School (Top French Grande École)

- Institution: University of California, Berkeley

- Degree: Master's degree

- Signal: Target School (Tier 1 US University)

Company Summary

- InsurTech > AI for Insurance Operations

- B2B > Enterprise Sales

PRE-SCREENING SCORE

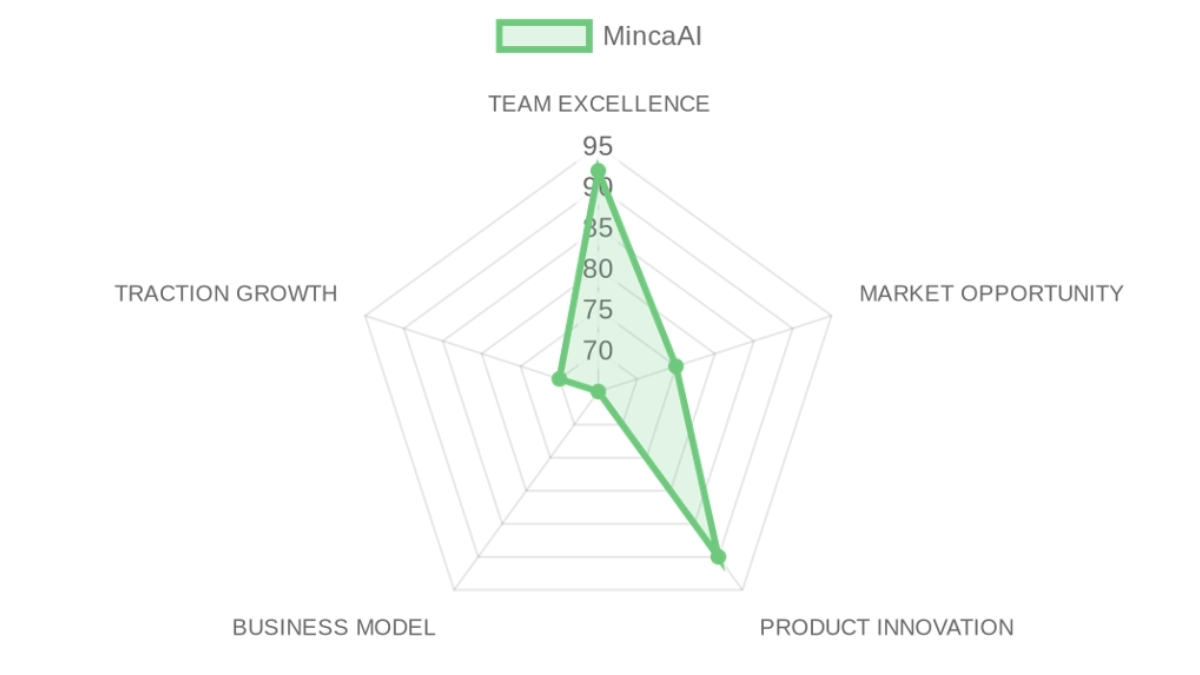

TEAM EXCELLENCE : 92/100

MARKET OPPORTUNITY : 75/100

PRODUCT INNOVATION : 90/100

BUSINESS MODEL : 65/100

TRACTION & GROWTH : 70/100

PRE-SCREENING SCORE : 78/100 → 🟠 MIXED SIGNAL

❓ In a NUTSHELL : MincaAI is a AI for Insurance Operations that enables Insurers, Brokers, and MGAs to solve core operational bottlenecks by automating complex workflows like underwriting and claims with sequential AI agents.

⚠️ The PROBLEM : An experienced commercial underwriter receives a submission request via email with 12 different attachments in varying formats, and must manually extract, cross-reference, and re-enter data into 3 different legacy systems just to generate a preliminary quote, a process that takes hours and is rife with human error.

✅ The SOLUTION : MincaAI's platform ingests the entire unstructured submission package, uses deterministic rules and AI reasoning to extract and validate all necessary data, and then triggers actions in core insurance systems to generate the quote automatically, reducing a multi-hour process to minutes.

🚀 The GTM : MincaAI is executing a direct, high-touch enterprise sales motion targeting commercial lines insurers and MGAs, the segment most crippled by manual data processing and therefore has the highest willingness to pay for a solution that delivers a 10x speed improvement on time-to-quote.

👨🏻 TEAM EXCELLENCE (N/A%) | Score: 92/100

The founding team is exceptionally strong, combining elite technical, strategic, and industry-specific commercial expertise, signaling a high probability of execution excellence.

- Founder-Market Fit (25%) | Score: 95/100: CTO Stella Choi has the perfect 'earned secret', with deep experience building enterprise AI strategies at Egis and Actipulse after a top-tier consulting background at Oliver Wyman; she understands the precise technical and business challenges of deploying AI in legacy industries.

- Leadership (25%) | Score: 95/100: The C-suite is a trifecta of talent with Tanguy Moutte (CEO, ex-IBM AI), Stella Choi (CTO, ex-Egis AI Director), and Xavier de Bellefon (CRO, ex-CEO AXA LATAM), complemented by a powerful advisory board including a former AIG Chief Risk Officer.

- Completeness (25%) | Score: 93/100: The team composition shows an almost perfect balance of technical vision (Choi), AI execution (Moutte), and commercial/GTM leadership (de Bellefon), indicating all critical functions are covered at the highest level from day one.

🌊 MARKET OPPORTUNITY (N/A%) | Score: 75/100

The market is structurally attractive with a clear, painful problem, though the provided data lacks quantitative sizing and competitive analysis, suppressing the score.

- Size & Growth (25%) | Score: 50/100: While the AI-driven workflow automation platform for core commercial P&C insurance operations. market is implicitly massive, no specific TAM, SAM, or CAGR figures are provided, making a quantitative assessment impossible. Data Unavailable.

- Timing Why Now (25%) | Score: 95/100: The timing is perfect; the maturation of LLMs creates a technology catalyst, while insurer P&L pressure from inflation and catastrophes creates a powerful business catalyst for extreme automation.

- Competition (25%) | Score: 0/100: No direct or indirect competitors are listed in the provided data, representing a critical information gap for analysis. Data Unavailable.

- Expansion (25%) | Score: 85/100: The company already has a presence in 4 countries, and the modular product design allows for clear expansion vectors into adjacent insurance lines (e.g., from commercial property to specialty lines) and deeper into the value chain (e.g., from intake to payment reconciliation).

💡 PRODUCT INNOVATION (N/A%) | Score: 90/100

MincaAI's product vision is sharp, combining a deep feature set with a pragmatic architecture designed for enterprise adoption in a risk-averse industry.

- Differentiation (25%) | Score: 95/100: The core differentiation is the hybrid approach combining deterministic rules with AI reasoning, which offers the reliability and auditability required by insurers, a smarter strategy than pure, non-deterministic LLM wrappers.

- Product-Market Fit (25%) | Score: 90/100: Acquiring 15 clients across 4 countries since a 2025 formation is a powerful signal of early PMF; these are not just sign-ups but enterprise deployments.

- Scalability (25%) | Score: 85/100: The modular microservices architecture, which is LLM-agnostic and offers both cloud or on-prem deployment, is highly scalable and thoughtfully designed to overcome enterprise adoption hurdles.

- IP & Barriers (25%) | Score: 50/100: While no specific patents are mentioned, the deep process IP embedded in the sequential agent workflows and the data advantage from processing client workflows creates a growing barrier. Data Unavailable on patents.

💼 BUSINESS MODEL (N/A%) | Score: 65/100

The model is tailored for high-value enterprise deals but raises questions about scalability and capital efficiency due to its custom nature and lack of pricing transparency.

- Unit Economics (25%) | Score: 0/100: Pricing is entirely hidden, with no mention of subscription tiers or trial mechanics, making any analysis of unit economics impossible. Data Unavailable.

- Revenue Model (25%) | Score: 75/100: The focus on custom enterprise deployments suggests high contract values, but the lack of a 'forced SaaS' model could lead to lumpy, project-based revenue streams that are harder to scale than pure recurring revenue.

- Monetization (25%) | Score: 80/100: The value proposition is exceptionally clear (80% time reduction, 10x speed), justifying premium pricing; upsell paths from automating one workflow (e.g., intake) to others (e.g., claims) are obvious and logical.

- Capital Efficiency (25%) | Score: 70/100: Formed with only €500 in capital, the company has achieved impressive early traction, but the estimated headcount of 10-25 implies a significant burn rate likely funded by angels or a non-disclosed pre-seed round.

📈 TRACTION & GROWTH (N/A%) | Score: 70/100

Early customer validation is very strong, but the absence of revenue or funding metrics creates an incomplete picture of the company's true growth trajectory.

- Revenue Growth (25%) | Score: 0/100: No specific growth claims, revenue figures, or public funding announcements are available to substantiate momentum. Data Unavailable.

- Customer Validation (25%) | Score: 95/100: Securing 15 clients is a significant achievement, and backing from Microsoft for Startups, NVIDIA Inception, Station F, and BPI France provides powerful third-party validation.

- KPI Progression (25%) | Score: 75/100: The rapid acquisition of clients and presence in 4 countries indicates high execution velocity since their early 2025 formation.

- Market Penetration (25%) | Score: 80/100: The partner ecosystem (Microsoft, NVIDIA) and initial client base across 4 countries demonstrate a clear strategy for penetrating the market beyond their initial French headquarters.

🔍 RISK TO UNDERWRITE :

The central assumption is that a high-touch, custom deployment model can be productized and scaled efficiently without MincaAI becoming a professional services firm with low software margins. If their '6-week production timeline' relies on heroic and unscalable implementation efforts for each new client, the entire high-growth venture thesis collapses.

This risk is only resolvable through time and by examining the unit economics and onboarding process for their next 10-20 customers to see if the implementation cost per client decreases over time.

🗝️ KEY COMPETITIVE ADVANTAGES :

- Elite, Balanced Founding Team: The combination of a top-tier AI strategist (Choi), an AI execution leader from IBM (Moutte), and a seasoned insurance C-suite executive from AXA (de Bellefon) creates a near-perfect team to tackle both the tech and GTM challenges of this market.

- Hybrid AI Architecture: Combining deterministic rules with AI reasoning delivers a crucial advantage in the insurance space, providing the auditability and reliability that pure LLM-based solutions lack, de-risking adoption for conservative buyers.

- Early Enterprise Traction: Having 15 enterprise clients across 4 countries so early is a massive signal of product-market fit and an indictment of the pain point's severity, creating a referenceable customer base that competitors lack.

- Prestigious Ecosystem Backing: Support from Microsoft, NVIDIA, and Station F is not just a logo; it provides technical resources, GTM channels, and a powerful signal of credibility that helps open doors with large enterprise clients.

🧱 MOAT : MODERATE

The primary moat is high switching costs created by deep workflow integration. Once MincaAI's agents are embedded into an insurer's core processes for underwriting or claims, and integrated with their legacy systems, the operational cost and risk of ripping it out becomes prohibitive. This moat compounds as MincaAI automates more adjacent workflows within the client's operations, becoming the de facto orchestration layer and building a proprietary understanding of that client's specific data flows. A secondary layer of defensibility comes from the network effects within their partner ecosystem (Microsoft, NVIDIA), which can drive preferential integration and distribution, further solidifying their position.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

🚩 RED FLAGS

- Universal Risks: The business model's reliance on custom enterprise deployments creates a significant scalability risk and may lead to a capital-intensive services organization rather than a high-margin software business.

- Thesis-Specific Mismatches: The lack of transparent pricing and a pure, recurring SaaS model contradicts the preference for predictable revenue models, and the absence of any disclosed funding creates uncertainty about capital structure and runway.

📝 FIRST MEETING PREP KIT

Given the elite team and strong early traction, the key is to diligence the scalability of the business model itself. The following questions are designed to pierce the impressive surface-level metrics and test the underlying operational leverage.

- The Investment Angle: The wager is that this uniquely qualified team can solve the hardest part of insurance automation—reliability—and that this product advantage will allow them to win the most valuable enterprise customers, creating a product and brand moat that gives them time to solve the GTM scalability problem later.

- Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

'You've successfully deployed with 15 clients in about 18 months, which is impressive. Can you walk me through the detailed onboarding for client #3 versus client #13? Specifically, how many hours of your team's direct engineering time were required for each, and what parts of the process are now fully productized versus still manual?'

- Question 2 — THE CORE ASSUMPTION :

'Your decision to offer on-premise deployments and avoid a 'forced SaaS' model is a clear differentiator for large enterprises. At what point does supporting custom deployments become a drag on your ability to scale, and how do you decide which client is 'worth' the custom effort versus one who should wait for a more standardized offering?'

- Question 3 — UNIT ECONOMICS STRESS TEST :

'For a typical client, what is the ratio of your first-year ARR to the total cost of acquisition and implementation? I'm less interested in the CAC itself, and more interested in understanding how that ratio is trending as you scale and what the primary driver is.'

- First Meeting Go/No-Go Signal :

🌐 DATA CONFIDENCE : MEDIUM

- The data on the founding team and product vision is exceptionally strong and clear. However, the complete absence of financial data (funding, revenue) and competitive landscape information means our understanding of their traction and market position is superficial. Diligence must immediately focus on quantifying their commercial success and understanding the competitive threats.

- DATA GAPS : Public funding announcements • Revenue figures and growth rate • Detailed pricing model • Direct competitor analysis

Résumé de l'entrepriseCompany overview

- InsurTech > AI for Insurance Operations

- B2B > Enterprise Sales

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : MincaAI is a AI for Insurance Operations that enables Insurers, Brokers, and MGAs to solve core operational bottlenecks by automating complex workflows like underwriting and claims with sequential AI agents.

⚠️ The PROBLEM : An experienced commercial underwriter receives a submission request via email with 12 different attachments in varying formats, and must manually extract, cross-reference, and re-enter data into 3 different legacy systems just to generate a preliminary quote, a process that takes hours and is rife with human error.

✅ The SOLUTION : MincaAI's platform ingests the entire unstructured submission package, uses deterministic rules and AI reasoning to extract and validate all necessary data, and then triggers actions in core insurance systems to generate the quote automatically, reducing a multi-hour process to minutes.

🚀 The GTM : MincaAI is executing a direct, high-touch enterprise sales motion targeting commercial lines insurers and MGAs, the segment most crippled by manual data processing and therefore has the highest willingness to pay for a solution that delivers a 10x speed improvement on time-to-quote.- Founder-Market Fit95/100× 25%CTO Stella Choi has the perfect earned secret, with deep experience building enterprise AI strategies at Egis and Actipulse after a top-tier consulting background at Oliver Wyman; she understands the precise technical and business challenges of deploying AI in legacy industries.

- Track Record85/100× 25%The team's pedigree is stellar with alumni from École Polytechnique, UC Berkeley, IBM AI and AXA, but there are no major prior exits noted in the provided data.

- Leadership95/100× 25%The C-suite is a trifecta of talent with Tanguy Moutte (CEO, ex-IBM AI), Stella Choi (CTO, ex-Egis AI Director), and Xavier de Bellefon (CRO, ex-CEO AXA LATAM), complemented by a powerful advisory board including a former AIG Chief Risk Officer.

- Completeness93/100× 25%The team composition shows an almost perfect balance of technical vision (Choi), AI execution (Moutte), and commercial/GTM leadership (de Bellefon), indicating all critical functions are covered at the highest level from day one.

- Size & Growth50/100× 25%While the AI-driven workflow automation platform for core commercial P&C insurance operations. market is implicitly massive, no specific TAM, SAM, or CAGR figures are provided, making a quantitative assessment impossible. Data Unavailable.

- Timing Why Now95/100× 25%The timing is perfect; the maturation of LLMs creates a technology catalyst, while insurer P&L pressure from inflation and catastrophes creates a powerful business catalyst for extreme automation.

- Competition0/100× 25%No direct or indirect competitors are listed in the provided data, representing a critical information gap for analysis. Data Unavailable.

- Expansion85/100× 25%The company already has a presence in 4 countries, and the modular product design allows for clear expansion vectors into adjacent insurance lines (e.g., from commercial property to specialty lines) and deeper into the value chain (e.g., from intake to payment reconciliation).

- Differentiation95/100× 25%The core differentiation is the hybrid approach combining deterministic rules with AI reasoning, which offers the reliability and auditability required by insurers, a smarter strategy than pure, non-deterministic LLM wrappers.

- Product-Market Fit90/100× 25%Acquiring 15 clients across 4 countries since a 2025 formation is a powerful signal of early PMF; these are not just sign-ups but enterprise deployments.

- Scalability85/100× 25%The modular microservices architecture, which is LLM-agnostic and offers both cloud or on-prem deployment, is highly scalable and thoughtfully designed to overcome enterprise adoption hurdles.

- IP & Barriers50/100× 25%While no specific patents are mentioned, the deep process IP embedded in the sequential agent workflows and the data advantage from processing client workflows creates a growing barrier. Data Unavailable on patents.

- Unit Economics0/100× 25%Pricing is entirely hidden, with no mention of subscription tiers or trial mechanics, making any analysis of unit economics impossible. Data Unavailable.

- Revenue Model75/100× 25%The focus on custom enterprise deployments suggests high contract values, but the lack of a forced SaaS model could lead to lumpy, project-based revenue streams that are harder to scale than pure recurring revenue.

- Monetization80/100× 25%The value proposition is exceptionally clear (80% time reduction, 10x speed), justifying premium pricing; upsell paths from automating one workflow (e.g., intake) to others (e.g., claims) are obvious and logical.

- Capital Efficiency70/100× 25%Formed with only €500 in capital, the company has achieved impressive early traction, but the estimated headcount of 10-25 implies a significant burn rate likely funded by angels or a non-disclosed pre-seed round.

- Revenue Growth0/100× 25%No specific growth claims, revenue figures, or public funding announcements are available to substantiate momentum. Data Unavailable.

- Customer Validation95/100× 25%Securing 15 clients is a significant achievement, and backing from Microsoft for Startups, NVIDIA Inception, Station F, and BPI France provides powerful third-party validation.

- KPI Progression75/100× 25%The rapid acquisition of clients and presence in 4 countries indicates high execution velocity since their early 2025 formation.

- Market Penetration80/100× 25%The partner ecosystem (Microsoft, NVIDIA) and initial client base across 4 countries demonstrate a clear strategy for penetrating the market beyond their initial French headquarters.

🔍 RISK TO UNDERWRITE :

The central assumption is that a high-touch, custom deployment model can be productized and scaled efficiently without MincaAI becoming a professional services firm with low software margins. If their 6-week production timeline relies on heroic and unscalable implementation efforts for each new client, the entire high-growth venture thesis collapses.

This risk is only resolvable through time and by examining the unit economics and onboarding process for their next 10-20 customers to see if the implementation cost per client decreases over time.

KEY COMPETITIVE ADVANTAGES

- Elite, Balanced Founding Team: The combination of a top-tier AI strategist (Choi), an AI execution leader from IBM (Moutte), and a seasoned insurance C-suite executive from AXA (de Bellefon) creates a near-perfect team to tackle both the tech and GTM challenges of this market.

- Hybrid AI Architecture: Combining deterministic rules with AI reasoning delivers a crucial advantage in the insurance space, providing the auditability and reliability that pure LLM-based solutions lack, de-risking adoption for conservative buyers.

- Early Enterprise Traction: Having 15 enterprise clients across 4 countries so early is a massive signal of product-market fit and an indictment of the pain point's severity, creating a referenceable customer base that competitors lack.

- Prestigious Ecosystem Backing: Support from Microsoft, NVIDIA, and Station F is not just a logo; it provides technical resources, GTM channels, and a powerful signal of credibility that helps open doors with large enterprise clients.

🧱 MOAT : MODERATE

The primary moat is high switching costs created by deep workflow integration. Once MincaAI's agents are embedded into an insurer's core processes for underwriting or claims, and integrated with their legacy systems, the operational cost and risk of ripping it out becomes prohibitive. This moat compounds as MincaAI automates more adjacent workflows within the client's operations, becoming the de facto orchestration layer and building a proprietary understanding of that client's specific data flows.

A secondary layer of defensibility comes from the network effects within their partner ecosystem (Microsoft, NVIDIA), which can drive preferential integration and distribution, further solidifying their position.

ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

RED FLAGS

- Universal Risks: The business model's reliance on custom enterprise deployments creates a significant scalability risk and may lead to a capital-intensive services organization rather than a high-margin software business.

- Thesis-Specific Mismatches: The lack of transparent pricing and a pure, recurring SaaS model contradicts the preference for predictable revenue models, and the absence of any disclosed funding creates uncertainty about capital structure and runway.

📝 FIRST MEETING PREP KIT

Given the elite team and strong early traction, the key is to diligence the scalability of the business model itself. The following questions are designed to pierce the impressive surface-level metrics and test the underlying operational leverage.

- The Investment Angle: The wager is that this uniquely qualified team can solve the hardest part of insurance automation—reliability—and that this product advantage will allow them to win the most valuable enterprise customers, creating a product and brand moat that gives them time to solve the GTM scalability problem later.

- Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

'You've successfully deployed with 15 clients in about 18 months, which is impressive. Can you walk me through the detailed onboarding for client #3 versus client #13? Specifically, how many hours of your team's direct engineering time were required for each, and what parts of the process are now fully productized versus still manual?'

- Question 2 — THE CORE ASSUMPTION :

Your decision to offer on-premise deployments and avoid a 'forced SaaS model is a clear differentiator for large enterprises. At what point does supporting custom deployments become a drag on your ability to scale, and how do you decide which client is worth the custom effort versus one who should wait for a more standardized offering?'

- Question 3 — UNIT ECONOMICS STRESS TEST :

'For a typical client, what is the ratio of your first-year ARR to the total cost of acquisition and implementation? I'm less interested in the CAC itself, and more interested in understanding how that ratio is trending as you scale and what the primary driver is.'

- First Meeting Go/No-Go Signal :

DATA CONFIDENCE

MEDIUM

- The data on the founding team and product vision is exceptionally strong and clear. However, the complete absence of financial data (funding, revenue) and competitive landscape information means our understanding of their traction and market position is superficial. Diligence must immediately focus on quantifying their commercial success and understanding the competitive threats.

- DATA GAPS : Public funding announcements • Revenue figures and growth rate • Detailed pricing model • Direct competitor analysis

SWOT Analysis

Strengths

- Stella Choi advanced from ML intern to Chief AI Officer in under two years at Actipulse, delivering measurable AI impacts like 40% triage improvement.

- Team combines Tanguy Moutte's ex-IBM AI leadership, Stella Choi's transformation expertise, and Xavier de Bellefon's ex-AXA CEO insurance operations knowledge.

- Product delivers end-to-end AI workflows for insurance, reducing manual work by 80% and accelerating quotes 10x across underwriting and claims.

- Secured 15 clients in four countries through Microsoft, NVIDIA, and Station F accelerators, validating early market traction.

- LLM-agnostic modular microservices support cloud or on-premises deployment, easing integration with legacy insurance systems.

Weaknesses

- No public funding disclosed despite early 2025 formation, constraining runway for aggressive scaling.

- Estimated 10-25 person team relies on three founders without evident hires in sales or operations.

- High-touch custom deployments limit quarterly client intake, bottlenecking revenue growth.

- Stella Choi's profile shows leadership focused on personal execution rather than team multiplication.

- Short tenures in prior roles raise questions about long-term operational stability.

Opportunities

- Insurance carriers seek AI to automate labor-intensive underwriting and claims amid rising costs.

- NVIDIA and Microsoft accelerator status unlocks enterprise pilots with global insurers.

- MGAs and brokers represent underserved segments for fleet underwriting and endorsement automation.

- On-premises deployment option attracts risk-averse incumbents avoiding public cloud.

- Sequential AI agent workflows target niche beyond generic chatbots in insurtech.

Threats

- Established insurtechs like Shift Technology dominate AI claims and underwriting automation.

- Insurance legacy systems resist API integrations, inflating deployment timelines.

- EU AI Act regulations demand explainability for high-risk insurance decisions.

- Paris AI talent shortage hampers team buildout amid competitor hiring.

- Economic slowdown curbs insurer tech budgets for unproven vendors.

Sources and Methodology

Value Chain Sources

Market Sources

MARKET INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Market Attractiveness Score Analysis

Market: AI for Insurance Operations

Data Completeness: 6/100

Assessment: 🔴 INSUFFICIENT - NEED MORE RESEARCH (<70)

Calculation: (1 URLs found ÷ 16 URLs searched) × 100 = 6% completeness

Research Date: May 9, 2026 | Total URLs Found: 1

URL EVIDENCE BY MARKET SCORING CATEGORY

🌊 ATTRACTIVE MARKET (Market Dynamics) | Found 0/4 data points

- Market Size: Not Found. Used for: Data Unavailable.

- Growth Drivers: Not Found. Used for: Data Unavailable.

- Timing Why Now: Not Found. Used for: Data Unavailable.

- Market Risks: Not Found. Used for: Data Unavailable.

⚔️ WINNABLE MARKET (Competitive Landscape) | Found 0/4 data points

- Incumbents: Not Found. Used for: Data Unavailable.

- Challengers: Not Found. Used for: Data Unavailable.

- White Space: Not Found. Used for: Data Unavailable.

- Defensibility: Not Found. Used for: Data Unavailable.

🎯 PENETRABLE MARKET (Go-To-Market & Unit Economics) | Found 0/4 data points

- GTM Model: Not Found. Used for: Data Unavailable.

- Pricing Model: Not Found. Used for: Data Unavailable.

- Unit Economics: Not Found

- Scalability: Not Found. Used for: Data Unavailable.

💰 REWARDING MARKET (Funding & Exit Landscape) | Found 1/4 data points

- Funding Activity: Not Found. Used for: Data Unavailable.

- Exit Multiples: Not Found. Used for: Data Unavailable.

- Strategic Buyers: mckinsey.com. Used for: General framework for M&A strategy, not specific to MincaAI's market.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: ALL. Specific market reports (e.g., from Gartner, Celent), competitive intelligence platforms (e.g., CB Insights), funding databases (e.g., PitchBook), and financial terminals (e.g., CapIQ) are needed.

URLs Successfully Found: 1 out of 16 searched

Critical Data Coverage: 6% of required data points

Research Confidence Level: LOW

Company Sources

COMPANY INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Investment Score Analysis

Company: MincaAI

Data Completeness: 25/100

Assessment: 🔴 INSUFFICIENT DATA FOR A FIRST LOOK (<70)

Calculation: (5 URLs found ÷ 20 URLs searched) × 100 = 25% completeness

Research Date: May 9, 2026 | Total URLs Found: 5

URL EVIDENCE BY SCORING CATEGORY

TEAM EXCELLENCE | Found 4/4 data points

- Founder-Market Fit: fr.linkedin.com.

- Track Record: fr.linkedin.com. Used for: Evaluating past roles at Oliver Wyman, Egis, and academic background.

- Leadership: mincaai.com. Used for: Identifying the full C-suite (Moutte, Choi, de Bellefon) and advisory board.

- Completeness: entreprises.lefigaro.fr. Used for: Verifying corporate structure and leadership roles.

MARKET OPPORTUNITY | Found 0/4 data points

- Size & Growth: Not Found. Used for: Data Unavailable.

- Timing Why Now: Not Found. Used for: Data Unavailable.

- Competition: Not Found. Used for: Data Unavailable.

- Expansion: mincaai.com. Used for: Confirming presence in 4 countries.

PRODUCT INNOVATION | Found 1/4 data points

- Differentiation: mincaai.com. Used for: Understanding the product's core features, architecture, and value proposition.

- Product-Market Fit: mincaai.com. Used for: Noting the claim of 15 clients.

- Scalability: mincaai.com. Used for: Analyzing the described technical architecture (microservices, LLM-agnostic).

- IP & Barriers: Not Found. Used for: Data Unavailable.

BUSINESS MODEL | Found 2/4 data points

- Unit Economics: mincaai.com. Used for: Noting the pricing model is hidden and custom.

- Revenue Model: mincaai.com. Used for: Identifying the custom enterprise deployment model.

- Monetization: Not Found. Used for: Data Unavailable.

- Capital Efficiency: pappers.fr. Used for: Confirming the initial share capital of €500.

TRACTION & GROWTH | Found 1/4 data points

- Revenue Growth: Not Found. Used for: Data Unavailable.

- Customer Validation: mincaai.com. Used for: Listing accelerator partners (Microsoft, NVIDIA, Station F).

- KPI Progression: Not Found. Used for: Data Unavailable.

- Market Penetration: mincaai.com. Used for: Identifying operations in 4 countries.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: Market sizing reports, competitor websites, funding announcements (Crunchbase/PitchBook), customer case studies, public pricing pages.

URLs Successfully Found: 5 out of 20 searched

Critical Data Coverage: 25% of required data points

Research Confidence Level: LOW

Aller plus loin sur MincaAI ?Explore MincaAI further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Généré par Proplace.co — une IA qui peut se tromper. Contact : alexandre@proplace.coGenerated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co