Roomex Interactive Memo

Mobility & Transportation ➜ Workforce Travel Management SaaS ➜ Corporate travel and business hotel booking platform purpose-built for workforce travel that saves time and money through simplified booking, payment, and spend management with zero fees.

Corporate travel and business hotel booking platform purpose-built for workforce travel that saves time and money through simplified booking, payment, and spend management with zero fees.

Want a detailed, personalized memo on this company?

Market Sizing

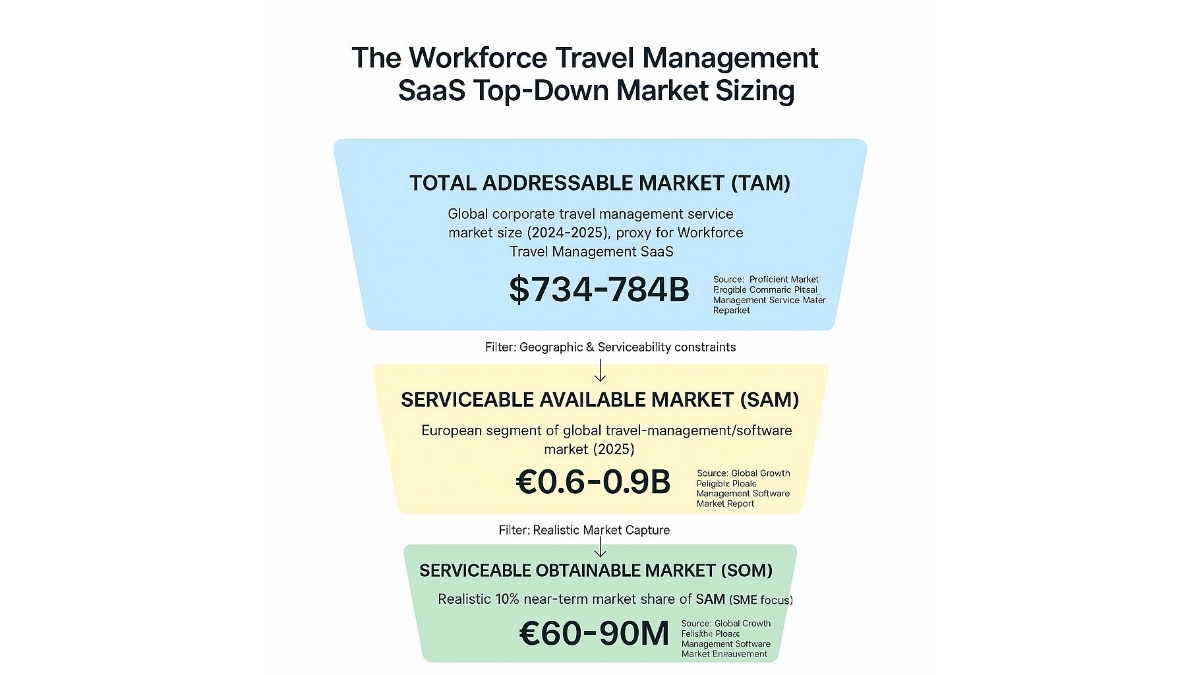

Top-Down Market analysis

Total Addressable Market (TAM): $734-784B

- Perimeter: Global corporate travel management service market size (2024-2025), proxy for Workforce Travel Management SaaS

- Source Data: Proficient Market Insights Corporate Travel Management Service Market Report (proficientmarketinsights.com)

Serviceable Available Market (SAM): €0.6-0.9B

- Perimeter: European segment of global travel-management/software market (2025)

- Logic: Filtered for our specific sector and geography.

- Source Verification: Global Growth Insights Travel Management Software Market Report (globalgrowthinsights.com)

Serviceable Obtainable Market (SOM): €60-90M

- Perimeter: Realistic 10% near-term market share of SAM (SME focus)

- Logic: Realistic near-term target based on competitive landscape.

- Source: Global Growth Insights Travel Management Software Market Report (SAM-based calculation) (globalgrowthinsights.com)

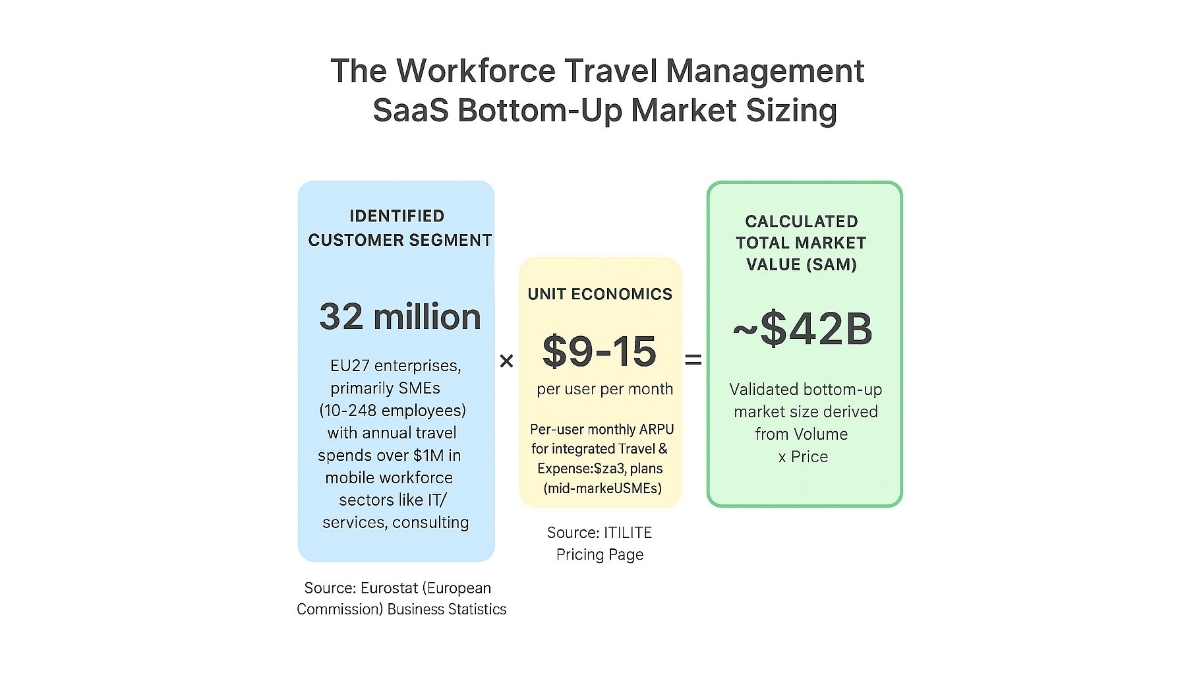

Bottom-Up Market analysis

This approach calculates the total market size by multiplying the validated number of potential customers by a verified average price point.

1. Customer Segment (Volume): 32 million

- Who they are: Primarily SMEs in EU27 with mobile workforce and annual travel spend >$1M (travel-heavy sectors: IT/services, consulting, manufacturing, BFSI)

- Validated Source: Eurostat (European Commission) Business Statistics (ec.europa.eu)

2. Unit Economics (Price): $9-15 per user per month

- What this represents: Per-user monthly ARPU for integrated Travel & Expense SaaS plans (mid-sized teams, tiered add-ons)

- Validated Source: ITILITE Pricing Page (itilite.com)

3. Calculated Result: ~$42B

• This figure represents the mathematically derived Serviceable Available Market based on the specific inputs above.

Triangulation

Top-down provides sourced conservative estimates (TAM $734-784B, SAM €0.6-0.9B, SOM €60-90M), treating broad service market as SaaS proxy. Bottom-up yields larger SAM (~$42B) and TAM (~$168B) from EU enterprise units x ARPU x assumptions (50 users/company, 5yr contracts), directionally validating scale but highlighting proxy discrepancies; top-down prioritized for reliability with bottom-up confirming opportunity.

Market trends

MARKET INTELLIGENCE: SME Travel SaaS Acceleration

1. Market Catalyst & Trajectory

- The Structural Shift: Shift from enterprise-mature services to emerging SME SaaS adoption for travel policy enforcement, expense control, and accommodation in mobile workforces, driven by cloud adoption, AI compliance, duty-of-care, carbon tracking, GDPR, and sustainability reporting. proficientmarketinsights.com globalgrowthinsights.com

- Velocity & Validation: Global TAM $734-784B (2024-2025) forecast to grow to $1,300-1,500B by mid-decade (implied multi-year high double-digit CAGR >50% in segments); European SAM €0.6-0.9B (25-31% of global); 32M EU enterprises (primarily SMEs) as customer units with >$1M travel spend potential. proficientmarketinsights.com globalgrowthinsights.com ec.europa.eu

2. Value Chain & Control Points

- The Scarcity: Stage 2: Supplier Sourcing and Integrations acts as the new bottleneck, enabling real-time policy-compliant access to hotel/accommodation inventory via GDS/API feeds critical for mobile workforce platforms.

- Leverage Dynamics: Highest strategic score (7.25) from high defensibility (7: technical complexity, network effects, switching costs), high margins (7: economies of scale, mixed costs), high growth (8: >20% CAGR proxy); commands pricing power via integration moats over commoditized booking/expense stages. globalgrowthinsights.com en.wikipedia.org

3. Competitive Dislocation

- Incumbent Vulnerability: Mature commoditized incumbents like SAP Concur suffering differentiation erosion (maturity 9, differentiation 3) in fragmented SME/mid-market despite enterprise dominance.

- Mechanism of Displacement: AI-driven innovators (Navan, TravelPerk: differentiation 7) and integrated platforms erode legacy via superior ERP integrations, real-time spend control, policy optimization, and SME-focused UX, commoditizing enterprise-grade features. travelcapitalist.com crunchbase.com

4. Unit Economics & Value Capture

- Margin Profile: Profit pool shifting to high SaaS stages: Expense Capture and Reconciliation (margin 10: 70-85% gross, premium pricing $9-15/user/month, fixed costs) and Booking (9: 75-90% gross); expansion from scale in policy/integrations vs. low-margin analytics/support (2.5).

- The Winning Configuration: Per-user-per-month SaaS ($9-15 ARPU for mid-market SMEs, tiered add-ons) integrated across Stages 2-4 (supplier/policy/booking/expense) targeting 32M EU enterprises, capturing fragmented SME via easy onboarding and compliance. itilite.com ec.europa.eu

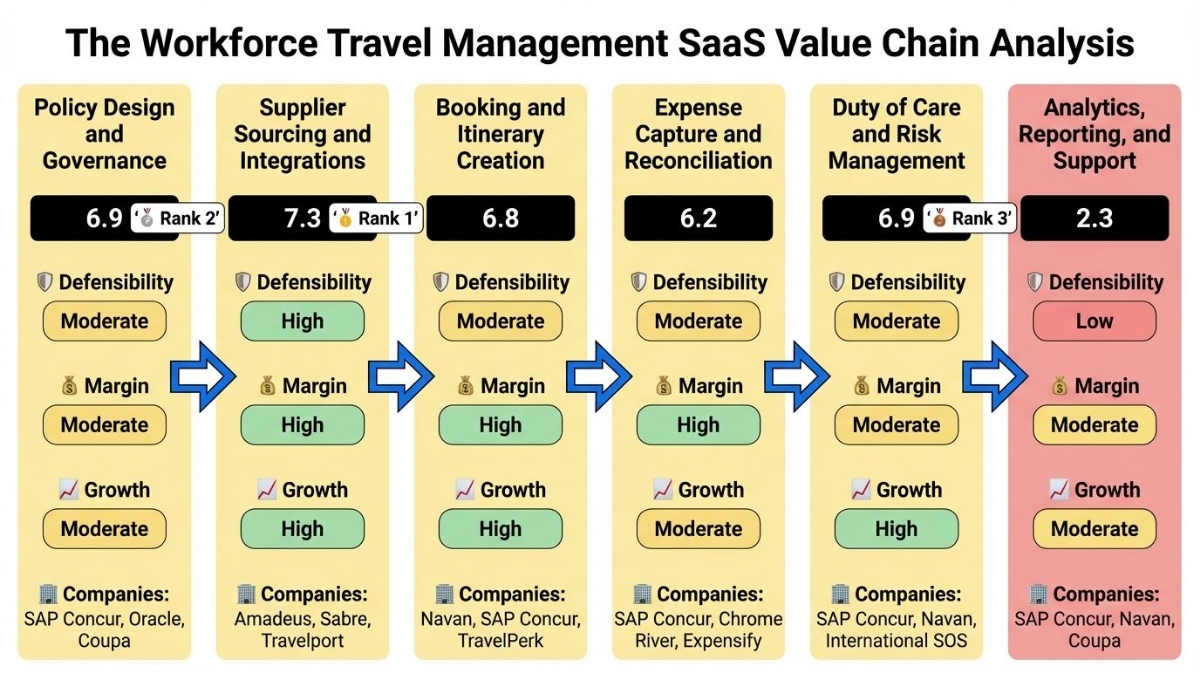

Value Chain Analysis

Value chain stage description

STAGE [1]: Policy Design and Governance

This upstream stage involves defining travel policies, compliance rules (e.g., VAT, duty-of-care standards), approval workflows, and governance frameworks tailored to mobile workforce accommodation/expenses. It adds value by enabling enforceable cost controls and risk alignment before any booking occurs.

🔢 Strategic Score: 6.9 (Strong)

🛡️DEFENSIBILITY (6/10): Moderate barriers.

Key factors: Technical Complexity (High +2) • Capital Requirements (Moderate +1) • Regulatory Barriers (Strong +1).

Source: Workforce Travel Management SaaS value chain analysis (https://www.marketgrowthreports.com/market-reports/corporate-travel-management-ctm-software-market-108731?utm_source=openai)

💰 MARGIN POTENTIAL (8.5/10): Moderate margins, typical range 75-85%.

Key factors: Cost Structure (Fixed-cost +3) • Economies of Scale (Strong +2).

Source: profit margins query (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

📈 GROWTH (6/10): Moderate growth, CAGR ~15-20%.

Key drivers: TAM Expansion (Growing +2) • Adoption Curve (Early majority +2).

Source: Global Growth Insights market report (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

🏢 SPECIALIZED COMPANIES: SAP Concur (policies) • Oracle (governance) • Coupa (spend policy)

💬 STAGE INSIGHT: Stage 1 has moderate-high defensibility from technical policy complexity and regulation, paired with strong SaaS margins from fixed costs. Moderate growth from market digitalization makes it attractive for incumbents building moats early.

STAGE [2]: Supplier Sourcing and Integrations

This stage acquires supplier content (hotels, accommodation for mobile workforce), negotiates rates, and builds integrations (GDS, APIs for expense feeds). Value from enabling real-time policy-compliant access to inventory.

🔢 Strategic Score: 7.3 (Strong)

🛡️DEFENSIBILITY (7/10): High barriers.

Key factors: Technical Complexity (High +2) • Network Effects (Moderate +1) • Switching Costs (High +1).

Source: Wikipedia Amadeus (https://en.wikipedia.org/wiki/Amadeus_IT_Group?utm_source=openai)

💰 MARGIN POTENTIAL (7/10): High margins, typical range 70-85%.

Key factors: Economies of Scale (Strong +2) • Cost Structure (Mixed +1.5).

Source: ITILITE pricing (https://www.itilite.com/pricing/?utm_source=openai)

📈 GROWTH (8/10): High growth, CAGR ~20-30%.

Key drivers: CAGR (>20% +3) • Adoption Curve (Early adopters +3).

Source: Global Growth Insights (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

🏢 SPECIALIZED COMPANIES: Amadeus (GDS) • Sabre (integrations) • Travelport (content)

💬 STAGE INSIGHT: High defensibility from integrations and networks pairs with solid SaaS margins and strong growth from travel rebound/digital adoption, making this a prime moat-building stage.

STAGE [3]: Booking and Itinerary Creation

Core stage for self-service booking of accommodations/expenses with policy checks, real-time availability for mobile workforce. Value in compliant, efficient itinerary fulfillment handoff to expense.

🔢 Strategic Score: 6.8 (Strong)

🛡️DEFENSIBILITY (4/10): Moderate barriers.

Key factors: Switching Costs (High +1) • Network Effects (Moderate +1) • Technical Complexity (Moderate +1).

Source: Market Growth Reports (https://www.marketgrowthreports.com/market-reports/corporate-travel-management-ctm-software-market-108731?utm_source=openai)

💰 MARGIN POTENTIAL (9/10): High margins, typical range 75-90%.

Key factors: Pricing Power (Premium +3) • Cost Structure (Fixed-cost +3).

Source: ITILITE (https://www.itilite.com/pricing/?utm_source=openai)

📈 GROWTH (8/10): High growth, CAGR 26-30%.

Key drivers: TAM Expansion (New market +3) • CAGR (20-30% +3).

Source: Global Growth Insights (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

🏢 SPECIALIZED COMPANIES: Navan (self-serve) • SAP Concur (booking) • TravelPerk (centralized)

💬 STAGE INSIGHT: Core booking stage offers high margins from SaaS pricing but lower defensibility; explosive growth from travel recovery positions it as dynamically attractive for scale-ups.

STAGE [4]: Expense Capture and Reconciliation

Post-booking stage captures receipts, auto-matches itineraries, reconciles with cards/ERP for accommodation/expenses. Critical value in cost control/audit for high-spend mobile firms.

🔢 Strategic Score: 6.2 (Strong)

🛡️DEFENSIBILITY (3/10): Moderate barriers.

Key factors: Switching Costs (High +1) • Technical Complexity (Moderate +1) • Regulatory Barriers (Strong +1).

Source: Global Growth Insights (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

💰 MARGIN POTENTIAL (10/10): High margins, typical range 70-85%.

Key factors: Pricing Power (Premium +3) • Economies of Scale (Strong +2).

Source: ITILITE (https://www.itilite.com/pricing/?utm_source=openai)

📈 GROWTH (6/10): Moderate growth, CAGR double-digit.

Key drivers: TAM Expansion (Growing +2) • Adoption Curve (Mainstream +2).

Source: Global Growth Insights (https://www.globalgrowthinsights.com/market-reports/travel-management-software-market-121386?utm_source=openai)

🏢 SPECIALIZED COMPANIES: SAP Concur (expense mgmt) • Chrome River (automation) • Expensify (receipts)

💬 STAGE INSIGHT: Expense stage excels in margin potential (max score) from SaaS economics but has lower defensibility; steady growth from compliance needs suits specialized players.

STAGE [5]: Duty of Care and Risk Management

Monitors traveler risks post-booking (location tracking, alerts) for mobile workforce safety. Value in liability reduction, handoff to support/analytics.

🔢 Strategic Score: 6.9 (Strong)

🛡️DEFENSIBILITY (6/10): Moderate barriers.

Key factors: Technical Complexity (High +2) • Network Effects (Moderate +1) • Capital Requirements (Moderate +1).

Source: GetMonetizely Procurement Guide (https://www.getmonetizely.com/articles/procurement-guide-how-are-corporate-travel-management-platforms-priced-for-enterprises?utm_source=openai)

💰 MARGIN POTENTIAL (6.5/10): Moderate margins, typical range unknown.

Key factors: Pricing Power (Premium +3) • Cost Structure (Mixed +1.5).

Source: profit margins query (https://www.getmonetizely.com/articles/procurement-guide-how-are-corporate-travel-management-platforms-priced-for-enterprises?utm_source=openai)

📈 GROWTH (9/10): High growth, CAGR high-teens.

Key drivers: TAM Expansion (New market +3) • Adoption Curve (Early adopters +3).

Source: Business Research Co TMS Report (https://www.thebusinessresearchcompany.com/report/corporate-travel-management-software-global-market-report?utm_source=openai)

🏢 SPECIALIZED COMPANIES: SAP Concur (risk add-ons) • Navan (features) • International SOS (response)

💬 STAGE INSIGHT: Strong growth from safety priorities boosts this stage, with solid defensibility from tech/reg; margins moderate due to variable costs but attractive for differentiation.

STAGE [6]: Analytics, Reporting, and Support

Downstream optimization with dashboards, ROI tracking, customer success for accommodation/expense insights. Value in continuous improvement and retention.

🔢 Strategic Score: 2.3 (Low)

🛡️DEFENSIBILITY (1/10): Low barriers.

Key factors: Network Effects (Moderate +1).

Source: Market Growth Reports (https://www.marketgrowthreports.com/market-reports/corporate-travel-management-ctm-software-market-108731?utm_source=openai)

💰 MARGIN POTENTIAL (2.5/10): Moderate margins, typical range 0-15%.

Key factors: Pricing Power (Market-rate +1.5) • Observed Margins (<40% +1).

Source: Rippling blog (https://www.rippling.com/blog/best-travel-management-software?utm_source=openai)

📈 GROWTH (4/10): Moderate growth, CAGR double-digit.

Key drivers: CAGR (10-20% +2) • TAM Expansion (Stable +1).

Source: Business Research Co TMS Report (https://www.thebusinessresearchcompany.com/report/corporate-travel-management-software-global-market-report?utm_source=openai)

🏢 SPECIALIZED COMPANIES: SAP Concur (reporting) • Navan (dashboards) • Coupa (analytics)

💬 STAGE INSIGHT: Low defensibility/margins due to commoditization limit attractiveness; moderate growth for retention but best as bolt-on for upstream moats.

Top 3 Strategic Positions

Best Strategic Positions OverviewBased on the comprehensive value chain analysis using the Strategic Position Score methodology (weighted combination of Defensibility 40%, Margin Potential 35%, and Growth 25%), the following three stages represent the most attractive investment opportunities in the SaaS-based workforce travel management platform for accommodation and expense control targeting mobile workforce companies with annual travel spends over $1M. value chain:

🥇 Rank 1: Stage [2] - Supplier Sourcing and Integrations

🔢 Strategic Score: 7.3

💬 STRATEGIC RATIONALE: Highest balance with strong defensibility (integrations/networks), solid margins (scale advantages), and top growth (travel tech boom); ideal for moats in supplier-dependent sector targeting accommodation.

🔎 KEY SUPPORTING EVIDENCE:

🥈 Rank 2: Stage [1] - Policy Design and Governance

🔢 Strategic Score: 6.9

💬 STRATEGIC RATIONALE: Upstream control yields high margins/technical moats, with regulation aiding defensibility; growth from policy digitalization offsets slightly lower growth score.

🔎 KEY SUPPORTING EVIDENCE:

📈 GROWTH (6/10): Moderate growth, CAGR ~15-20%.

Key drivers: TAM Expansion (Growing +2) • Adoption Curve (Early majority +2).

Source: Global Growth Insights market report (globalgrowthinsights.com)

🥉 Rank 3: Stage [5] - Duty of Care and Risk Management

🔢 Strategic Score: 6.9

💬 STRATEGIC RATIONALE: Explosive growth from safety priorities boosts this stage, with solid defensibility from tech/reg; margins moderate due to variable costs but attractive for differentiation.

🔎 KEY SUPPORTING EVIDENCE:

Value Chain Players

Policy Design and Governance

Oracle

T1

USA

$20B

🟥

Diff: 4

Meta Grid

Founding: Unknown | Funding: N/A | Investors: N/A

Description: Oracle is an enterprise technology company focusing on cloud and AI initiatives, databases, and business applications.

Weak Signals

- Oracle (ORCL) in 2024–2025 focused on cloud and AI initiatives, strategic partnerships, and a significant leadership transition, rather than traditional startup-style funding rounds. Oracle, as an established enterprise, does not typically engage in startup-style "funding rounds." Capital activity during 2024–2025 was channeled into financing large cloud/AI initiatives, debt management, and strategic investments, without new public equity fundraises (https://capital.com/en-int/markets/shares/oracle-share-price/market-cap?utm_source=openai).

- Oracle's market capitalization exhibited notable fluctuations in 2024–2025, peaking around $900+ billion in September 2025, then pulling back to approximately $441 billion by February 13, 2026 (https://capital.com/en-int/markets/shares/oracle-share-price/market-cap?utm_source=openai). Cash and cash equivalents ranged from about $10.7–$11.0 billion in 2024, expanding to approximately $11.0–$19.8 billion in 2025 across quarterly reports, with Q4 2025 values reaching around $19.8 billion in some datasets, indicating strong liquidity (https://www.macrotrends.net/stocks/charts/ORCL/oracle/cash-on-hand?utm_source=openai).

- Oracle's M&A activity in 2024–2025 was characterized by modest, incremental or strategic acquisitions rather than groundbreaking mega-deals. The company prioritized expansion through partnerships and cloud-scale contracts, particularly bolstering Oracle Cloud Infrastructure, AI, and enterprise applications (https://apnews.com/article/69ad588693f0c8de9fe6dcf4632037d3?utm_source=openai). No major blockbuster acquisitions were prominently reported during this period (https://apnews.com/article/69ad588693f0c8de9fe6dcf4632037d3?utm_source=openai).

- Oracle continuously develops and patents technologies across enterprise databases, cloud infrastructure, AI-enabled data services, and security. Specific patent disclosures for 2024–2025 are typically found in quarterly/annual IP disclosures and patent office records, rather than headline news (https://www.macrotrends.net/stocks/charts/ORCL/oracle/cash-on-hand?utm_source=openai).

- In 2025, Oracle announced a significant leadership transition, appointing Clay Magouyrk and Mike Sicilia as co-CEOs, with Safra Catz transitioning to executive vice chair. This move, covered by AP and The Verge, aimed to strategically position Oracle for the AI era and cloud-forward growth (https://apnews.com/article/69ad588693f0c8de9fe6dcf4632037d3?utm_source=openai).

- Public statements from 2024–2025 consistently highlighted Oracle's AI, cloud infrastructure, multicloud strategy, and strategic partnerships, including AI-related initiatives and OpenAI-related cloud use cases, as central to its growth narrative (https://apnews.com/article/69ad588693f0c8de9fe6dcf4632037d3?utm_source=openai).

- T1_Global_Giant; $19B cash AI/cloud Stage 1.

- Co-CEO transition.

- Acquisition Iris.ai: Scientific AI Hunted.

- Acquisition Snowflake Inc. (SNOW): Data cloud tuck-in.

- Snowflake rivalry.

SAP Concur

T1

USA

$20B

🟥

Diff: 3

Meta Grid

Founding: 1993 | Funding: Acquired | Investors: SAP (Acquirer)

Description: SAP Concur is an enterprise-grade travel and expense platform with long-standing integrations and policy enforcement.

Weak Signals

- SAP Concur operates as a subsidiary of SAP SE, and its strategic direction and financial activities in 2024–2025 were integrated within the parent company's broader initiatives. SAP Concur did not conduct independent private fundraising rounds in 2024 or 2025, with funding and capital allocation determined at the SAP group level. SAP SE's corporate funding activities during this period included strategic investments and M&A, particularly for its cloud and AI initiatives (https://news.sap.com/2025/03/celebrating-next-era-of-travel-and-expense-sap-concur-fusion/?utm_source=openai).

- SAP SE achieved a market capitalization in the hundreds of billions of euros range during 2024–2025, becoming one of Europe's most valuable companies by March 24, 2025 (https://www.wsj.com/finance/stocks/germanys-sap-overtakes-wegovy-maker-novo-nordisk-as-europes-most-valuable-company-4bd290bf?utm_source=openai). The company's cash on hand was approximately $12.16 billion (USD) in 2024, maintaining a range of $11–12.5 billion in Q3 2025, reflecting SAP SE-level liquidity, not a Concur-only metric (https://www.macrotrends.net/stocks/charts/SAP/sap-se/cash-on-hand?utm_source=openai).

- SAP's M&A strategy, which indirectly impacts Concur, included the acquisition of WalkMe for approximately $1.5 billion, with closing targeted for 2024. This acquisition was intended to enhance user adoption and AI-enabled capabilities across SAP's software stack, benefiting Concur through improved UX and automation (https://www.marketwatch.com/story/sap-to-acquire-walkme-in-all-cash-deal-valuing-at-about-1-5-billion-f27af972?utm_source=openai).

- SAP Concur Fusion in March 2025 showcased AI-driven innovations and partnerships, such as with Mastercard for automatic expense capture and Amex Global Travel content, indicating a strategy of incremental enhancements and collaborations rather than standalone M&A for Concur itself (https://news.sap.com/2025/03/celebrating-next-era-of-travel-and-expense-sap-concur-fusion/?utm_source=openai).

- SAP Concur leverages a combination of in-house development and SAP's broader IP portfolio. While specific Concur-only patents are not extensively detailed in public press, its capabilities are rooted in travel and expense management workflows, AI-enabled automation, and integrations that align with SAP's overall proprietary tech stack (https://news.sap.com/2025/03/celebrating-next-era-of-travel-and-expense-sap-concur-fusion/?utm_source=openai).

- In 2025, SAP Concur highlighted expanded partnerships, including Mastercard for expense entry and Amex Global Travel for content integration into Concur Travel, enhancing content and automation for customers (https://news.sap.com/2025/03/celebrating-next-era-of-travel-and-expense-sap-concur-fusion/?utm_source=openai).

- CEO Christian Klein’s statements in 2024–2025 emphasized SAP's cloud-first, AI-driven growth strategy, which shapes Concur's roadmap and partnerships (https://time.com/7307213/sap-ceo-christian-klein-interview/?utm_source=openai). The WalkMe acquisition, announced in 2023 and closing in 2024, reflects SAP's broader strategy (https://www.marketwatch.com/story/sap-to-acquire-walkme-in-all-cash-deal-valuing-at-about-1-5-billion-f27af972?utm_source=openai). SAP Concur Fusion 2025 occurred on March 24, 2025, showcasing AI features and partnerships (https://news.sap.com/2025/03/celebrating-next-era-of-travel-and-expense-sap-concur-fusion/?utm_source=openai). By March 24, 2025, SAP was recognized as Europe's most valuable company by market capitalization (https://www.wsj.com/finance/stocks/germanys-sap-overtakes-wegovy-maker-novo-nordisk-as-europes-most-valuable-company-4bd290bf?utm_source=openai).

- T1_Global_Giant; Stage 1 leader, SAP backing, diff 3 but enterprise scale.

- Commoditized legacy (diff 3); SME erosion per macro.

- Acquisition Iris Finance: Acquire Hunted T6 AI CFO ($2M cap) for policy analytics.

- Acquisition Onfly: Bolt-on T5 expense for SME.

- Navan/TravelPerk displacement in SME; low diff vulnerable.

Involved Strategic Scenarios

- SME Innovators Squeeze Legacy SAP Concur Differentiation

- SAP Concur's Iris Finance Grab to Counter SME AI Displacement

Coupa

T3

USA

$5B

🟥

Diff: 7

Meta Grid

Founding: Unknown | Funding: Acquired | Investors: Thoma Bravo (Acquirer)

Description: Coupa, acquired by Thoma Bravo, provides AI-native spend-management solutions and focuses on expanding its supplier network.

Weak Signals

- Coupa, acquired by Thoma Bravo in 2023, focused on strategic acquisitions to expand its AI-native spend-management capabilities and supplier network in 2024–2025. Coupa was acquired by private equity firm Thoma Bravo in a cash deal that closed on February 28, 2023. As a private company, Coupa did not conduct public equity funding rounds during 2024–2025 (https://www.coupa.com/fr/newsroom/thoma-bravo-completes-acquisition-coupa-software/?utm_source=openai).

- Following its privatization, Coupa lacks a current public market capitalization. Information regarding cash on hand and liquidity metrics is proprietary to its owners, Thoma Bravo and co-investors, and is not publicly disclosed (https://companiesmarketcap.com/coupa/cash-on-hand/?utm_source=openai).

- Under Thoma Bravo's ownership, Coupa actively pursued an M&A strategy focused on strengthening AI-native spend management and expanding its supplier network. Key acquisitions included Scoutbee in October 2025, aimed at integrating AI-powered supplier discovery, and Cirtuo (Q1 FY26), to enhance AI-powered category management and sourcing capabilities (https://www.digitalcommerce360.com/2025/10/10/coupa-acquisition-scoutbee-ai-supplier-discovery/?utm_source=openai; https://www.coupa.com/newsroom/coupa-delivers-strong-q1-amid-trade-volatility-fueled-by-ai-and-global-customer-momentum/?utm_source=openai). These acquisitions align with a strategy to deepen AI capabilities and expand network reach (https://www.coupa.com/newsroom/global-trade-complexities-fuel-growth-for-coupas-ai-native-total-spend-management-platform/?utm_source=openai).

- Coupa emphasizes proprietary AI-native capabilities, driven by its "Navi" AI agent and a vast anonymized community data network encompassing trillions of dollars in spend data. This data moat underpins its AI-driven workflows and connects approximately 10 million suppliers and hundreds of customers (https://www.forbes.com/sites/stevebanker/2024/05/01/coupa-leverages-community-intelligence-to-power-ai/?utm_source=openai; https://www.coupa.com/newsroom/global-trade-complexities-fuel-growth-for-coupas-ai-native-total-spend-management-platform/?utm_source=openai).

- Publicly available patenting data for private companies is limited, but Coupa frames Navi and its AI-enabled features as core differentiating technologies (https://www.coupa.com/newsroom/global-trade-complexities-fuel-growth-for-coupas-ai-native-total-spend-management-platform/?utm_source=openai).

- Leagh Turner was appointed CEO on November 13, 2023, leading the company through its private-equity ownership phase (https://www.coupa.com/newsroom/leagh-turner-named-coupa-ceo/?utm_source=openai). Her public commentary, including interviews with Forbes (March 2025, May 2024) and appearances at Thoma Bravo's AI Summit 2024, focused on AI-enabled spend management, supply chain optimization, and the company's community data moat (https://www.forbes.com/sites/meganpoinski/2025/03/10/for-tariffs-those-who-optimize-fastest-will-win-coupa-ceo-says/?utm_source=openai; https://www.forbes.com/sites/stevebanker/2024/05/01/coupa-leverages-community-intelligence-to-power-ai/?utm_source=openai; https://www.thomabravo.com/ideas/ceo-conversations-with-coupas-leagh-turner-at-thoma-bravos-ai-summit-2024?utm_source=openai). The Scoutbee acquisition was announced October 9–10, 2025 (https://www.digitalcommerce360.com/2025/10/10/coupa-acquisition-scoutbee-ai-supplier-discovery/?utm_source=openai), and Cirtuo was mentioned in June 2025 communications as an acquired asset (https://www.coupa.com/newsroom/coupa-delivers-strong-q1-amid-trade-volatility-fueled-by-ai-and-global-customer-momentum/?utm_source=openai).

- T3_Medium PE-backed; Scoutbee/Cirtuo AI acqs.

- N/A.

- Acquisition Iris Finance: AI CFO Hunted.

- Acquisition SAP Ariba: Consolidate procurement market.

- SAP Concur competition.

Supplier Sourcing and Integrations

Booking.com

T1

USA

$20B

🟥

Diff: 7

Meta Grid

Founding: Unknown | Funding: N/A | Investors: N/A

Description: Booking.com is a flagship brand of Booking Holdings Inc., specializing in online travel bookings, particularly accommodation.

Weak Signals

- Booking.com, as a flagship brand of Booking Holdings Inc. (BKNG), engaged in strategic initiatives focusing on technological enhancement and market positioning during 2024–2025, rather than standalone funding rounds. Booking.com, as a subsidiary of Booking Holdings Inc. (BKNG), did not conduct separate external funding rounds in 2024 or 2025. Capital allocation for Booking.com is determined at the parent company level (https://businessquant.com/metrics/bkng/cash-and-equivalents?utm_source=openai).

- Booking Holdings consistently maintained one of the largest market capitalizations in online travel, with figures around tens of billions of USD by mid-2025, and high market cap rankings as of July 2025 (https://www.statista.com/statistics/1039616/leading-online-travel-companies-by-market-cap/?utm_source=openai).

- Cash and cash equivalents for Booking Holdings were approximately $16.2 billion in 2024, rising to an estimated $16.5 billion by mid-2025, reflecting a robust liquidity position for capital expenditure, selective M&A, and share repurchases (https://www.macrotrends.net/stocks/charts/BKNG/booking-holdings/cash-on-hand?utm_source=openai).

- Booking Holdings’ M&A strategy remained selective, prioritizing bolt-on technological enhancements, product scale improvements, and strategic assets aligned with its core OTA platforms. The company's prior proposed $1.8 billion acquisition of Etraveli Group was blocked by the EU in 2023, influencing its subsequent regulatory-aware approach to M&A. No large, cross-border acquisitions were publicly closed in 2024–2025, indicating a conservative stance post-Etraveli (https://apnews.com/article/39ad09d030738473865a1b989f2f72c6?utm_source=openai).

- Booking Holdings invests significantly in proprietary technology, including pricing algorithms, meta-search capabilities, hotel inventory management, and user experience. While specific patent lists for Booking.com are not routinely disclosed, its competitive advantage stems from scale, data, and platform engineering. Patent filings, if any, are typically assigned to Booking Holdings directly (https://businessquant.com/metrics/bkng/cash-and-equivalents?utm_source=openai).

- Booking.com engages in ongoing partnerships with payment providers, OTAs, hotels, and travel-service technology vendors to optimize inventory, payments, and distribution. CEO Glenn Fogel’s public interviews in 2024–2025 consistently emphasized focus on core platforms, profitability, regulatory navigation, and continuous investment in technology to enhance search, pricing, and consumer experience (https://businessquant.com/metrics/bkng/cash-and-equivalents?utm_source=openai). The EU's prior antitrust scrutiny of the Etraveli deal in 2023 continued to shape Booking Holdings' M&A strategy for 2024–2025, particularly regarding large-scale consolidation in the online travel sector (https://apnews.com/article/39ad09d030738473865a1b989f2f72c6?utm_source=openai).

- T1_Global_Giant public; $16B cash, Stage 2 leader in supplier sourcing.

- Regulatory blocks (e.g., Etraveli); legacy focus misses SME nuances.

- Acquisition WorkersStay: Acquire niche housing ($1M cap) for Stage 2 workforce inventory amid SME shift.

- Acquisition hotelkit: Buy T5 Opportunistic for hotel ops integration.

- Amadeus/Sabre GDS rivalry; Navan/TravelPerk SME disruption.

Involved Strategic Scenarios

- SME Housing Race: TravelPerk vs Booking.com for WorkersStay

- Booking.com Roll-Up of Niche Housing Players for Stage 2 Dominance

- Booking.com vs Amadeus War for SME Hotel Inventory Control

Amadeus

T1

ESP

$20B

🟥

Diff: 7

Meta Grid

Founding: 1987 | Funding: N/A | Investors: N/A

Description: Amadeus IT Group is a major provider of GDS and travel content, focusing on IT solutions for the travel industry.

Weak Signals

- Amadeus IT Group (AMS.MC) focused on internal capital management and selective, strategic acquisitions in 2024–2025, rather than external funding rounds. Amadeus did not announce new external funding rounds in 2024 or 2025. Its capital actions included a substantial share buyback program, amounting to approximately €1.3 billion, executed around 2024–2025, to return capital to shareholders (https://cincodias.elpais.com/companias/2025-02-28/amadeus-gano-1258-millones-en-2024-un-196-mas-gracias-al-alza-de-sus-distintos-segmentos-de-ventas.html?utm_source=openai).

- The company reported a net profit of about €1.258 billion (adjusted €1.348 billion) and revenue around €6.142 billion in 2024, supporting this capital-return strategy (https://cincodias.elpais.com/companias/2025-02-28/amadeus-gano-1258-millones-en-2024-un-196-mas-gracias-al-alza-de-sus-distintos-segmentos-de-ventas.html?utm_source=openai). Market capitalization estimates for Amadeus in 2024–2025 ranged from €20–30+ billion, with figures around €21–23 billion reported by Yahoo Finance in late 2025 and approximately €30.7 billion by Disfold in July 2025 (https://fr.finance.yahoo.com/quote/AMS.MC/key-statistics/?utm_source=openai; https://disfold.com/company/amadeus-it-group-sa/financials/?utm_source=openai).

- Cash on hand for Amadeus was reported around €1.24–1.30 billion at the end of 2024, fluctuating to €0.96–1.13 billion by September 2025, reflecting normal quarterly variations (https://www.macrotrends.net/stocks/charts/AMADY/amadeus-it-group-sa/cash-on-hand?utm_source=openai).

- Amadeus’s M&A strategy in 2024–2025 involved selective, strategic tuck-in acquisitions. A notable example was the acquisition of Forward Data S.L. in 2025 for approximately €15–16 million, demonstrating a focus on enhancing niche data/IT capabilities within travel technology (https://cincodias.elpais.com/companias/2025-05-08/amadeus-dispara-su-beneficio-un-12-hasta-los-363-millones-de-euros.html?utm_source=openai).

- Amadeus, a significant technology provider in the travel industry, continuously invests in IT solutions for its core platforms and tech stack. The company's R&D activities in Europe, supported by partnerships with entities like the European Investment Bank (EIB) for a €250 million R&D investment around 2023–2024, underscore its focus on technological advancement (https://www.eib.org/en/press/all/2023-252-eib-and-amadeus-sign-new-eur250-million-partnership-to-support-rd-investments-in-it-solutions-for-the-travel-industry?utm_source=openai). However, specific new patents were not prominently disclosed in 2024–2025 public summaries. The EIB financing partnership from 2023–2024 indicated Amadeus’s commitment to European R&D (https://www.eib.org/en/press/all/2023-252-eib-and-amadeus-sign-new-eur250-million-partnership-to-support-rd-investments-in-it-solutions-for-the-travel-industry?utm_source=openai).

- CEO Luis Maroto's public commentary in 2024–2025 reiterated the company's resilience and growth, particularly regarding strong financial performance (https://cincodias.elpais.com/companias/2025-02-28/amadeus-gano-1258-millones-en-2024-un-196-mas-gracias-al-alza-de-sus-distintos-segmentos-de-ventas.html?utm_source=openai). Key dates include 2024 financial results reporting a net profit of €1.258 billion and a €1.3 billion share buyback program (https://cincodias.elpais.com/companias/2025-02-28/amadeus-gano-1258-millones-en-2024-un-196-mas-gracias-al-alza-de-sus-distintos-segmentos-de-ventas.html?utm_source=openai), the 2025 acquisition of Forward Data S.L. for approximately €15.3 million (https://cincodias.elpais.com/companias/2025-05-08/amadeus-dispara-su-beneficio-un-12-hasta-los-363-millones-de-euros.html?utm_source=openai), and the 2023–2024 EIB financing partnership (https://www.eib.org/en/press/all/2023-252-eib-and-amadeus-sign-new-eur250-million-partnership-to-support-rd-investments-in-it-solutions-for-the-travel-industry?utm_source=openai).

- T1_Global_Giant; Stage 2 GDS leader €1.3B buyback.

- Selective M&A post-reg.

- Acquisition Stay22: Acquire Hunted maps ($2M) for Stage 2 content.

- Acquisition Acai Travel: AI TMC bolt-on.

- Sabre/Travelport GDS wars; SME SaaS bypass.

Involved Strategic Scenarios

- Amadeus GDS Controls Squeeze TravelPerk vs Navan

- Booking.com vs Amadeus War for SME Hotel Inventory Control

Sabre

T2

USA

$5B

🟦

Diff: 4

Meta Grid

Founding: Unknown | Funding: N/A | Investors: N/A

Description: Sabre is a major provider of GDS content and IT solutions to the travel industry, refocusing on airline IT and travel marketplace platforms.

Weak Signals

- Sabre (SABR) underwent a significant strategic divestiture in 2025, refocusing its core business on airline IT and travel marketplace platforms. Sabre announced a definitive agreement on April 28, 2025, to divest its Hospitality Solutions business to TPG for $1.1 billion in cash, with expected net proceeds of approximately $960 million aimed at debt reduction. The transaction closed on July 7, 2025, as part of Sabre's portfolio optimization and deleveraging strategy (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai).

- Sabre's market capitalization fluctuated in the low hundreds of millions of dollars during 2024–2025, with figures around $0.6–0.7 billion in late 2025 (https://uk.finance.yahoo.com/quote/SABR/key-statistics/?utm_source=openai). Cash on hand (cash and cash equivalents) ranged between approximately $0.66–0.75 billion in 2024–2025, with $746 million at year-end 2024 and $660–670 million in late 2025, according to Macrotrends and market data (https://www.macrotrends.net/stocks/charts/SABR/sabre/cash-on-hand?utm_source=openai). The 2025 divestiture to TPG significantly improved Sabre’s balance sheet by reducing debt and influences future market capitalization and leverage metrics (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai).

- Post-2024, Sabre's strategic focus shifted to core airline IT and travel marketplace platforms. The divestiture of Hospitality Solutions to TPG in July 2025 was aimed at deleveraging and reinvesting in strategic software assets (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai). While past acquisitions included Nuvola (2022) and Techsembly (2023) to bolster hospitality, the 2025 sale marked a shift away from this unit (https://www.hospitality.today/article/sabre-completes-hospitality-solutions-sale?utm_source=openai).

- Sabre's primary proprietary technology assets and growth focus reside in Sabre Travel Solutions and its airline IT/travel marketplace platforms. While the SynXis-based Hospitality Solutions were historically foundational, they were sold in 2025. The company emphasizes continuous product modernization and cloud-native offerings (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai). Specific patent numbers are not prominently disclosed in 2024–2025 filings, with strategic materials highlighting platform architecture and data capabilities (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai).

- President and CEO Kurt Ekert publicly articulated the Hospitality Solutions divestiture as a transformative step toward focusing on core airline IT and travel marketplace platforms and improving the balance sheet (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai). The transaction with private equity firm TPG was positioned to enable a stronger capital structure and strategic focus (https://investors.sabre.com/news-releases/news-release-details/sabre-enters-definitive-agreement-sell-its-hospitality-solutions?utm_source=openai).

- December 2024 saw debt refinancings and 2025 debt maturity management, complemented by the 2025 Hospitality Solutions sale (https://investors.sabre.com/node/19101/html?utm_source=openai). The closing of the Hospitality Solutions sale on July 7, 2025, solidified Sabre’s strategic shift toward debt reduction and portfolio refocus (https://investors.sabre.com/news-releases/news-release-details/sabre-announces-closing-sale-hospitality-solutions-business-tpg?utm_source=openai).

- T2_Large; $1.1B divestment/debt reduction.

- Market cap low $600M.

- Acquisition Hopper: Mobile-first OTA.

- Amadeus GDS rivalry.

Travelport

T3

Unknown

$5B

🟦

Diff: 4

Meta Grid

Founding: Unknown | Funding: Equity Financing | Investors: Elliott Investment Management, Davidson Kempner Capital Management, Canyon Partners, Siris Capital

Description: Travelport is a global distribution system (GDS) provider that focuses on travel technology platforms and content.

Weak Signals

- Travelport, operating as a private entity, completed a substantial equity financing round in early 2024 and strategically optimized its portfolio, including a notable divestiture. Travelport completed a new equity financing round in early January 2024, raising approximately $570 million from existing equity holders and lenders. This financing aimed to deleverage the balance sheet and support investments in technology platforms. Key investors included Elliott Investment Management, Davidson Kempner Capital Management, Canyon Partners, and Siris Capital (https://www.travelport.com/press-release/travelport-completes-new-equity-financing?utm_source=openai).

- The eNett business was subsequently sold to Wex in 2024, reflecting portfolio optimization under private ownership (https://bradkruse.com/wex-to-acquire-travelports-enett-for-1-7-billion/?utm_source=openai).

- As a private company since 2019, Travelport does not have a publicly announced market capitalization for 2024–2025 (https://www.businesstravelnews.com/Procurement/Travelport-Investors-Complete-Equity-Financing?utm_source=openai). While exact cash-on-hand figures for a private entity are not routinely disclosed, the 2024 financing explicitly aimed to strengthen liquidity and balance-sheet resilience (https://skift.com/2023/12/04/travelport-raises-570-million-and-adds-new-owners/?utm_source=openai).

- Travelport's strategy in 2024–2025 focused on investing in technology platforms (Travelport+ and AI-enabled content) and opportunistic divestitures, rather than large public M&A. The eNett sale to Wex in 2024 is illustrative of this asset-level optimization strategy (https://www.travelport.com/press-release/travelport-completes-new-equity-financing?utm_source=openai). Although Travelport previously pursued acquisitions to enhance its platform (e.g., Deem), no new large, transformative deals were publicly announced in 2024–2025 (https://www.businesstravelnews.com/Procurement/Travelport-Investors-Complete-Equity-Financing?utm_source=openai).

- Travelport has historically invested in proprietary search and retailing technology, including ML-powered search and data/AI-enabled content curation for Travelport+. Past patents included innovations in airline data management and analytics (e.g., the "Alchemy" engine) around 2015 (https://www.travolution.com/news/technology/travelport-patents-database-analysis-tech/?utm_source=openai). However, public-facing patent activity for 2024–2025 is less visible due to private ownership, though continued investment in AI, ML, and content layers suggests ongoing proprietary tech development (https://www.travolution.com/news/technology/travelport-patents-database-analysis-tech/?utm_source=openai).

- CEO Greg Webb emphasized the 2024 equity financing, deleveraging, and continuous investment in Travelport+ and the Content Curation Layer, aiming for faster, AI-enabled retailing and improved agency tools (https://www.travelport.com/press-release/travelport-completes-new-equity-financing?utm_source=openai). A 2025 Skift profile highlighted the appointment of a new Chief Product and Technology Officer, Andrew Jordan, and a focus on modernizing agency booking tools and AI investments, signaling a continued emphasis on technology modernization (https://skift.com/2025/07/11/travelports-new-tech-chief-aims-to-modernize-how-agencies-book-trips/?utm_source=openai). The latest funding news reports Travelport completed a $570 million equity financing in January 2024 (https://www.travelport.com/press-release/travelport-completes-new-equity-financing?utm_source=openai). Market capitalization is not public due to private status, and cash on hand figures are not publicly disclosed (https://www.businesstravelnews.com/Procurement/Travelport-Investors-Complete-Equity-Financing?utm_source=openai). The sale of eNett to Wex in 2024 marked a notable divestiture (https://bradkruse.com/wex-to-acquire-travelports-enett-for-1-7-billion/?utm_source=openai). Greg Webb's communications in 2024 and news of a new CTO appointment in 2025 highlighted ongoing AI/retail modernization efforts (https://www.travelport.com/press-release/travelport-completes-new-equity-financing?utm_source=openai).

- T3_Medium PE-backed; $570M equity financing.

- Private, no market cap.

- Acquisition Cvent: Event tech synergy.

- Amadeus/Sabre GDS competition.

Booking and Itinerary Creation

TravelPerk

T4

ESP

$120M

🟥

Diff: 7

Meta Grid

Founding: 2015 | Funding: Series E | Investors: Atomico, EQT Growth, Sequoia Capital, General Catalyst, Kinnevik, SoftBank Vision Fund 2

Description: TravelPerk provides an integrated spend management platform evolving to end-to-end travel with policy controls for workforce mobility.

Weak Signals

- TravelPerk, rebranded as Perk, executed significant financing and strategic moves during 2024–2025. On January 23/28, 2024, the company secured a $104 million extension to its Series D-1 round, led by SoftBank Vision Fund 2, achieving a post-money valuation of approximately $1.4 billion. Existing investors, including Kinnevik and Felix Capital, also participated (https://www.cnbc.com/2024/01/23/softbank-leads-104-million-investment-in-travel-startup-travelperk.html?utm_source=openai).

- By January 28, 2025, TravelPerk completed a $200 million Series E round, led by Atomico with participation from EQT Growth, Sequoia Capital, General Catalyst, and Kinnevik, which doubled its valuation to approximately $2.7 billion. This round coincided with the acquisition of Yokoy (https://www.cnbc.com/2025/01/28/softbank-backed-travelperk-doubles-valuation-plans-fintech-push.html?utm_source=openai; https://sifted.eu/articles/general-catalyst-travelperk-200m-raise-news?utm_source=openai).

- In 2024, TravelPerk acquired U.S.-based travel platform AmTrav to expand its U.S. market presence, enhancing content, distribution, and customer reach (https://www.travelperk.com/fr/press-release/travelperk-leve-200-millions-de-dollars-et-fait-lacquisition-de-yokoy/?utm_source=openai). In January 2025, the company acquired Yokoy, a Swiss spend-management platform, to broaden its spend and expense capabilities and accelerate international expansion (https://www.travelperk.com/fr/press-release/travelperk-leve-200-millions-de-dollars-et-fait-lacquisition-de-yokoy/?utm_source=openai).

- TravelPerk’s M&A strategy for 2024–2025 focused on reinforcing core business travel management with integrated spend/expense capabilities, accelerating U.S. expansion, and leveraging acquisitions to broaden spend automation, AI-driven features, and financial workflow capabilities, with public statements emphasizing content expansion, spend automation, and cross-sell opportunities (https://www.travelperk.com/fr/press-release/travelperk-leve-200-millions-de-dollars-et-fait-lacquisition-de-yokoy/?utm_source=openai).

- Public sources do not indicate a disclosed patent portfolio for TravelPerk, with the company emphasizing platform automation, AI features, and open API integrations as its technological advantages (https://www.travelperk.com/press-release/travelperk-secures-over-100m-in-funding-to-expand-hypergrowth-platform/?utm_source=openai).

- TravelPerk expanded its distribution partnership with Amadeus on October 9, 2025, to include broader NDC content, reaching 25 NDC connections, signaling enhanced access to airline content (https://www.perk.com/fr/press-release/travelperk-hits-25-ndc-connections-as-it-strengthens-amadeus-partnership/?utm_source=openai; https://www.travelperk.com/press-release/travelperk-hits-25-ndc-connections-as-it-strengthens-amadeus-partnership/?utm_source=openai). The company maintains an ongoing open API/platform strategy to facilitate third-party integrations and marketplace partnerships (https://www.travelperk.com/partners/?utm_source=openai).

- CEO Avi Meir's public statements during January 2024 funding coverage underscored AI investments and product expansion as central to TravelPerk's strategy (https://www.cnbc.com/2024/01/23/softbank-leads-104-million-investment-in-travel-startup-travelperk.html?utm_source=openai). Subsequent coverage in January 2025 highlighted the company's valuation milestone and strategic emphasis on U.S. expansion (https://www.cnbc.com/2025/01/28/softbank-backed-travelperk-doubles-valuation-plans-fintech-push.html?utm_source=openai).

- T4_ScaleUp VC-backed with $120M capacity and diff score 7. Recent $200M Series E and acquisitions (AmTrav, Yokoy) position strongly in Stage 3 booking.

- Dependencies on Stage 2 suppliers and Stage 4 expense; European HQ limits global scale vs. giants.

- Acquisition BuildNStay: Acquire micro/distressed BuildNStay for cheap Stage-unknown expansion in SME workforce travel.

- Acquisition hotelkit: Buy niche T5 hotelkit ($1M cap, Opportunistic) to bolster Stage 2 integrations amid supplier bottleneck.

- Rivals Navan and Booking.com racing for SME share; macro SME acceleration favors integrated platforms over pure bookers.

Involved Strategic Scenarios

- TravelPerk Bolsters Stage 2 Bottleneck via hotelkit Acquisition

- SME Housing Race: TravelPerk vs Booking.com for WorkersStay

- TravelPerk-Roomex Alliance for Zero-Fee SME Workforce Capture

- SME Innovators Squeeze Legacy SAP Concur Differentiation

- Amadeus GDS Controls Squeeze TravelPerk vs Navan

- Navan/TravelPerk Siege Roomex Workforce Moat

American Express GBT

T1

Unknown

$20B

🟥

Diff: 4

Meta Grid

Founding: Unknown | Funding: N/A | Investors: N/A

Description: American Express Global Business Travel (Amex GBT) is a global business travel management company.

Weak Signals

- American Express Global Business Travel (Amex GBT), operating as Global Business Travel Group, Inc. (GBTG), executed a major strategic acquisition of CWT in 2024–2025, which significantly consolidated its market position and influenced its financial and operational focus. Amex GBT announced the acquisition of CWT in March 2024 for approximately $570 million (cash-free, debt-free), funded through a mix of stock and cash, with an expected close in H2 2024 (https://investors.amexglobalbusinesstravel.com/investors/news/news-details/2024/Amex-GBT-to-Acquire-CWT/default.aspx?utm_source=openai). The deal finalized around September 2, 2025, for approximately $540 million, integrating two large travel management platforms (https://www.paxnouvelles.com/nouvelles/regroupements-et-agences-hotes/amex-gbt-finalise-lacquisition-de-cwt/?utm_source=openai). Corporate communications emphasized continued cash generation and value creation from CWT integration, including synergy expectations (https://www.businesswire.com/news/home/20250506421727/en/American-Express-Global-Business-Travel-Reports-Strong-Profit-Growth-and-Margin-Expansion-in-Q1-2025-and-Issues-Q2-and-Updated-Full-Year-2025-Guidance?utm_source=openai).

- Amex GBT consistently reported strong cash generation and a flexible balance sheet, driven by Q1 2025 profit growth and margin expansion, supporting ongoing investments and acquisitions, notably the CWT deal (https://www.businesswire.com/news/home/20250506421727/en/American-Express-Global-Business-Travel-Reports-Strong-Profit-Growth-and-Margin-Expansion-in-Q1-2025-and-Issues-Q2-and-Updated-Full-Year-2025-Guidance?utm_source=openai). Market capitalization for GBTG is available for a smaller, post-IPO travel-tech firm; however, it is not as straightforward as for large consumer-facing companies.

- The high-level M&A strategy for 2024–2025 focused on market consolidation to gain scale, expand its software-enabled marketplace, and accelerate technology investments in AI, data analytics, and NDC content across its platforms (Neo, Neo+, Egencia). The CWT acquisition was central to this strategy, expected to yield over $150 million in annual synergies (https://investors.amexglobalbusinesstravel.com/investors/news/news-details/2024/Amex-GBT-to-Acquire-CWT/default.aspx?utm_source=openai). Regulatory scrutiny, such as from the UK CMA, was part of the process, with provisional clearance occurring in 2025 (https://www.ft.com/content/dfe6386d-0e2c-4c48-9898-08370381bf2b?utm_source=openai).

- Amex GBT acquired CWT, a major rival, with the announcement on March 25, 2024, and closing around September 2, 2025, for an estimated $540 million, significantly expanding its client base and scale (https://investors.amexglobalbusinesstravel.com/investors/news/news-details/2024/Amex-GBT-to-Acquire-CWT/default.aspx?utm_source=openai; https://www.paxnouvelles.com/nouvelles/regroupements-et-agences-hotes/amex-gbt-finalise-lacquisition-de-cwt/?utm_source=openai). Previous acquisitions, such as Egencia, highlight a consistent M&A playbook for building scale (https://investors.amexglobalbusinesstravel.com/investors/news/news-details/2024/Amex-GBT-to-Acquire-CWT/default.aspx?utm_source=openai).

- Amex GBT actively pursues intellectual property protection, exemplified by a US patent awarded in 2023 for an AI-powered customer-satisfaction engine, showcasing its investment in proprietary AI technology (https://www.amexglobalbusinesstravel.com/press-releases/american-express-global-business-travel-to-be-awarded-us-patent-for-ai-powered-customer-satisfaction-engine/?utm_source=openai). The company also markets proprietary platforms (Neo, Neo+, Egencia) and a marketplace with reinforced NDC content initiatives, such as with Air France-KLM (https://www.amexglobalbusinesstravel.com/press-releases/american-express-global-business-travel-launches-ndc-content-from-air-france-and-klm/?utm_source=openai).

- CEO Paul Abbott publicly emphasized how bringing CWT into Amex GBT's software and services model would enhance choice, value, and shareholder returns (https://investors.amexglobalbusinesstravel.com/investors/news/news-details/2024/Amex-GBT-to-Acquire-CWT/default.aspx?utm_source=openai). Partnerships included an expanded NDC collaboration with Air France-KLM on November 5, 2024 (https://www.gbta.org/fr/amex-gbt-announces-expanded-collaboration-withair-france-and-klm-to-scale-up-ndc-content/?utm_source=openai) and re-emphasized integrations with SAP Concur for a joint travel-and-expense solution (Oct 2025) (https://www.businesstravelnews.com/Management/Amex-GBT-Concur-Partner-for-Integrated-Travel-and-Expense-Offering?utm_source=openai). CEO Paul Abbott and CFO Karen Williams provided commentary on Q1 2025 earnings, emphasizing margins and cash generation (https://www.businesswire.com/news/home/20250506421727/en/American-Express-Global-Business-Travel-Reports-Strong-Profit-Growth-and-Margin-Expansion-in-Q1-2025-and-Issues-Q2-and-Updated-Full-Year-2025-Guidance?utm_source=openai).

- T1_Global_Giant; CWT $540M acq Stage 3.

- Reg scrutiny.

- Acquisition FCM Travel: TMC consolidation.

- Acquisition Navan: SaaS scale-up.

- Navan SME.

Navan

T2

USA

$5B

🟥

Diff: 7

Meta Grid

Founding: 2015 | Funding: Series G | Investors: Lightspeed Venture Partners

Description: Navan, the Palo Alto-based all-in-one travel, payments, and expense platform, provides tools for booking, expense management, corporate cards, and real-time spend control.

Weak Signals

- Navan, the Palo Alto-based all-in-one travel, payments, and expense platform, completed a significant funding round in 2024 and pursued an IPO in 2025, alongside strategic acquisitions. On October 28, 2024, Navan secured a $400 million Series G funding round, led by Lightspeed Venture Partners, achieving a reported valuation of $9.2 billion (https://aicurator.io/navan-funding/?utm_source=openai).

- In 2025, the company filed for and proceeded with a U.S. IPO, with market-facing actions for its Nasdaq listing (NAVN) extending into late 2025 (https://www.cnbc.com/2025/06/10/navan-cnbc-disruptor-50.html?utm_source=openai). The public debut valuation differed from the private rounds, reflecting a down-round-type environment in analyses (https://www.wsj.com/articles/navan-debut-is-the-latest-down-round-ipo-6fb4f002?utm_source=openai).

- As a publicly listed company post-IPO in October 2025, Navan's market capitalization fluctuated; by February 2026, third-party trackers indicated a market cap around €2.3 billion in Europe-tracked metrics (https://www.barrons.com/articles/government-shutdown-ipo-market-navan-stock-valuation-2c14bd34?utm_source=openai). Prior to its IPO, private valuations around 2022–2024 hovered near $9.2 billion (https://www.cnbc.com/2025/06/10/navan-cnbc-disruptor-50.html?utm_source=openai).

- Navan's M&A strategy for 2024–2025 involved expansion through acquisitions to broaden its travel and expense platform. Notable activities included acquiring Green Mackay (a UK travel agency) and Contravo (a Germany-based travel-tech firm) to strengthen inventory, distribution, and expense-management capabilities (https://www.forbes.com/sites/brandonkochkodin/2025/02/18/the-future-of-business-to-business-banking-fintech-50-2025/?utm_source=openai). These acquisitions illustrate Navan's strategy to expand its international footprint and integrate capabilities within its broader platform (https://www.forbes.com/sites/brandonkochkodin/2025/02/18/the-future-of-business-to-business-banking-fintech-50-2025/?utm_source=openai). Leadership appointments within the Navan Group (e.g., Reed & Mackay) also signaled ongoing inorganic and organizational expansion (https://reedmackay.com/fr/the-navan-group-announces-leadership-appointments?utm_source=openai).

- Navan has developed proprietary AI-centric platform components, including "Navan Cognition" (an AI framework) and "Ava" (an AI-powered virtual agent), designed to enhance support and automation across its platform, as detailed in its SEC filing materials for fiscal 2024–2025 (https://www.sec.gov/Archives/edgar/data/1639723/000162827925000476/filename1.htm?utm_source=openai).

- Navan's leadership, including CEO Ariel Cohen, was featured prominently in the 2025 CNBC Disruptor 50 profile, highlighting the company's growth as a leading travel-tech platform (https://www.cnbc.com/2025/06/10/navan-cnbc-disruptor-50.html?utm_source=openai). Public communications underscored the focus on core platforms, profitability, and regulatory navigation (https://www.forbes.com/sites/brandonkochkodin/2025/02/18/the-future-of-business-to-business-banking-fintech-50-2025/?utm_source=openai).

- T2_Large public post-IPO; $400M Series G, diff 7, Stage 3 leader with acquisitions.

- Dependencies across chain; down-round IPO valuation.

- Acquisition Acai Travel: Acquire Hunted T6 AI TMC ($2M cap) for Stage 3 optimization.

- Acquisition Onfly: Buy T5 Hunted ($15M cap) for LatAm expense expansion.

- TravelPerk/Amex GBT SME race; Stage 2 bottleneck from Amadeus.

Involved Strategic Scenarios

- Navan Expands LatAm via Onfly Bolt-On in Expense Dominance

- SME Innovators Squeeze Legacy SAP Concur Differentiation

- Amadeus GDS Controls Squeeze TravelPerk vs Navan

- Navan-Roomex Partnership for ESG Duty-of-Care in SMEs

- Navan/TravelPerk Siege Roomex Workforce Moat

Roomex

T4

IRL

$5B

🟦

Diff: 6

Meta Grid

Founding: 2010 | Funding: Acquired | Investors: Corpay (Acquirer), Frontline Ventures

Description: Roomex is a corporate lodging and payments platform integrated into Corpay's ecosystem, targeting workforce mobility in Europe.

Weak Signals

- Roomex, acquired by Fleetcor in 2022, continued to enhance its business travel booking platform through strategic partnerships and product feature extensions in 2024–2025, operating within Fleetcor's corporate strategy. Roomex raised a €3.5 million Series A round on September 28, 2016, led by Frontline Ventures (https://roomex.com/roomex-raises-%C2%803-5m-to-help-simplify-business-travel/?utm_source=openai). A reported Series A raise of €9.6 million also occurred around 2018 (https://app.welcometothejungle.com/companies/Roomex?utm_source=openai). The most significant financing and ownership event was its acquisition by Fleetcor Technologies in 2022 (https://app.welcometothejungle.com/companies/Roomex?utm_source=openai).

- Following its acquisition by Fleetcor in 2022, Roomex's independent M&A strategy ceased, with any subsequent strategic moves aligning with Fleetcor's corporate objectives. No standalone Roomex-led M&A targets or deals were publicly reported post-2022 (https://renatus.ie/renatus-weekly-ma-newsletter-23-10-2022/?utm_source=openai).

- Roomex's platform focuses on centralized corporate travel booking, single invoicing, policy controls, and reporting. While intellectual property is evident in its platform, no widely publicized patents or standalone IP registrations were found in public databases for Roomex for 2024–2025 (https://roomex.com/roomex-raises-%C2%808-million-to-build-business-travel-tech-platform/?utm_source=openai).

- Roomex partnered with SQUAKE in July 2024 to provide carbon-emissions reporting for bookings, using SQUAKE's API, aligning with sustainability goals (https://thebusinesstravelmag.com/roomex-leverages-api-for-carbon-reporting-tool/?utm_source=openai). The company also launched a rail engine through a partnership with Vibe, offering enhanced rail booking capabilities with features like split-save and post-purchase changes (https://www.vibe.travel/news/roomex-goes-live/?utm_source=openai). An earlier integration with Booking.com in 2019 expanded property supply (https://www.onlinemarketplaces.com/articles/roomex-adds-over-300k-properties-with-new-booking-com-partnership/?utm_source=openai).

- Leadership transitions occurred in the late 2010s, with Garry Moroney becoming CEO. Public reporting confirms this change and Roomex's status as a Fleetcor-owned subsidiary (https://www.onlinemarketplaces.com/articles/roomex-finally-replaces-ceo-after-co-founder-left-earlier-this-year/?utm_source=openai). There were no widely cited, independent CEO-level interviews for Roomex in 2024–2025, with recent material focusing on product news and Fleetcor integration. Key dates include September 28, 2016, for the €3.5 million Series A (https://roomex.com/roomex-raises-%C2%803-5m-to-help-simplify-business-travel/?utm_source=openai), 2022 for the acquisition by Fleetcor (https://app.welcometothejungle.com/companies/Roomex?utm_source=openai), and July 2024 for the partnership with SQUAKE for carbon reporting (https://thebusinesstravelmag.com/roomex-leverages-api-for-carbon-reporting-tool/?utm_source=openai).

- Proven scale: 1000+ clients including Allianz, Central Bank; 20yr ops since 2004 pivot.

- Acquisition validation: FleetCor buyout 2022 unlocks US/global resources post-€8M Series A.

- Zero-fee model: 12-32% savings via commissions resonates in cost-conscious workforce travel.

- Full-stack moat: RoomexStay/Pay/Rail/Analytics; 2M properties, Azure APIs, duty-of-care tracking.

- lacks tech innovator DNA.

- Post-acquisition limbo: No indep funding since 2018; growth tied to FleetCor integration.

- Commission dependency: Revenue from hotels erodes margins vs pure SaaS peers.

- Pivot recency: B2C to B2X in 2018; execution risk in unproven workforce niche.

- Opaque team: Headcount unknown; finance-led, thin on named product/sales talent.

- SOM €60-90M: 10% EU SME capture in €0.6-0.9B SAM; mobile workforce underserved.

- Tailwinds: ESG carbon reporting, duty-of-care mandates fuel analytics/policy upsell.

- Geographic runway: Dublin/London/Germany/US offices; FleetCor accelerates global.

- Value chain edge: Stage 3 booking (6.8 score) + expense (6.2); integrations beat incumbents.

- Bottom-up scale: 32M EU enterprises x $9-15 ARPU; SME digitalization gap.

- Incumbent crush: Concur/Navan/TravelPerk dominate booking/expense with deeper moats.

- Cyclical travel: Recession hits workforce spend; post-COVID rebound fragile.

- Integration failure: FleetCor synergies flop, stalling post-2022 momentum.

- Margin commoditization: Zero-fee attracts but supplier commissions vulnerable to disintermediation.

- Reg/tech shift: GDPR/ESG rules, AI rivals erode switching costs in low-defensibility stages.

Involved Strategic Scenarios

- TravelPerk-Roomex Alliance for Zero-Fee SME Workforce Capture

- Navan-Roomex Partnership for ESG Duty-of-Care in SMEs

- Navan/TravelPerk Siege Roomex Workforce Moat

- Roomex Fills Policy Gap with Inntel Alliance for UK SMEs

Acai Travel

T6

USA

$2M

🟨

Diff: 7

Meta Grid

Founding: 2023 | Funding: Seed | Investors: Nauta Capital, DraperB1, One Travel Ventures, Amadeus (Strategic)

Description: Acai Travel offers AI-enabled travel management for TMC ecosystems, focusing on booking optimization for workforce mobility.

Weak Signals

- Acai Travel secured seed funding in 2024 and strategic investment in 2025, gaining industry recognition for its AI-driven travel solutions. Acai Travel raised a $4 million seed round in 2024, with Nauta Capital identified as the lead investor. DraperB1 and One Travel Ventures also provided support (https://travelcapitalist.com/travel-startup-funding-report-past-7-days-nov-26-dec-3-2025/?utm_source=openai).

- In 2025, Amadeus Ventures participated in ongoing funding discussions, signaling continued investor interest (https://nordic9.com/news/acai-travel-to-raise-an-additional-equity-financing-round-with-amadeus-ventures/?utm_source=openai). Crunchbase lists Amadeus as an early investor (https://www.crunchbase.com/organization/acai-travel-inc?utm_source=openai).

- As a private company, Acai Travel does not have a publicly reported market capitalization or cash-on-hand figures for 2024-2025. Acai Travel received the Trailblazer Award at the 2025 TravelTech Show, recognizing its AI-driven approach to travel operations (https://traveltech-show.com/latest-news/acai-crowned-winner-2025-traveltech-show-trailblazer-awards?utm_source=openai).

- In early 2026, its AI automation solutions were highlighted for automating Nautalia Empresas’ back-office processes in Spain, indicating active real-world deployments (https://www.businesstravelnews.com/management/acai-to-automate-nautalia-empresas-back-office-processes?utm_source=openai). While reports hint at ongoing fundraising, no widely publicized M&A deals or explicit acquisition targets were announced by Acai Travel through 2025–early 2026 (https://nordic9.com/news/acai-travel-to-raise-an-additional-equity-financing-round-with-amadeus-ventures/?utm_source=openai).

- Acai Travel focuses on AI-driven back-office and front-office automation for travel agencies, OTAs, and TMCs, emphasizing solutions like AI Supervisor and AI Front-Office Agent. Specific patent filings are not prominently disclosed in reviewed sources, with emphasis placed on AI-enabled process automation (https://travelcapitalist.com/travel-startup-funding-report-past-7-days-nov-26-dec-3-2025/?utm_source=openai).

- The investment by Amadeus Ventures indicates a strategic alignment with a leading travel tech platform. Founders Riccardo Vittoria and Pavel Pratyush (CTO) are frequently cited in industry roundups (https://travelcapitalist.com/travel-startup-funding-report-past-7-days-nov-26-dec-3-2025/?utm_source=openai). Public commentary, often tied to industry events and awards, reinforces Acai Travel’s AI-driven automation narrative (https://traveltech-show.com/latest-news/acai-crowned-winner-2025-traveltech-show-trailblazer-awards?utm_source=openai).

- $4M seed + Amadeus; T6 AI TMC diff 7 Stage 3.

- $2M cap Hunted early.

- Exit/Sale Navan: AI to Hunter for TMC automation.

- Exit/Sale Amadeus: Ventures integration.

- TravelPerk AI push.

Expense Capture and Reconciliation

Rydoo

T4

Belgium

$5B

🟥

Diff: 4

Meta Grid

Founding: Unknown | Funding: Acquisition (Majority Stake) | Investors: Eurazeo PME IV, Marlin Equity Partners

Description: Rydoo provides AI-powered expense management, acquired by Eurazeo, and focuses on end-to-end spend management capabilities.

Weak Signals

- Rydoo underwent a significant ownership change in 2024 with Eurazeo acquiring a majority stake, followed by a strategic acquisition in 2025 to enhance its AI-powered expense management capabilities. On June 19, 2024, Eurazeo PME IV invested in Rydoo NV, becoming the majority shareholder, while Marlin Equity Partners reinvested. This transaction established Eurazeo as a controlling investor, marking the principal public funding/ownership event for Rydoo in 2024 (https://www.eurazeo.com/en/newsroom/press-releases/eurazeo-invests-rydoo-fast-growing-international-expense-management?utm_source=openai; https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/6/deal-wrap-eurazeo-to-buy-majority-stake-in-rydoo-main-capital-exits-textkernel-82138138?utm_source=openai).

- Rydoo announced the strategic acquisition of Semine, a Norwegian AI-powered accounts payable automation provider, on July 25, 2025. This acquisition was positioned as a major European and US expansion, strengthening Rydoo’s end-to-end spend-management capabilities (https://www.fusacq.com/buzz/semine-rejoint-le-portefeuille-de-solutions-de-rydoo-a254301_fr_?utm_source=openai). The Eurazeo deal and subsequent corporate actions positioned Rydoo for growth via add-on acquisitions and international expansion (https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/6/deal-wrap-eurazeo-to-buy-majority-stake-in-rydoo-main-capital-exits-textkernel-82138138?utm_source=openai).

- Rydoo remains a private company, lacking a publicly traded market capitalization or consistently disclosed cash-on-hand figures for 2024–2025. Its financial trajectory is primarily indicated by investor disclosures and corporate updates (https://www.eurazeo.com/en/newsroom/press-releases/eurazeo-invests-rydoo-fast-growing-international-expense-management?utm_source=openai; https://www.rydoo.com/inside-rydoo/rydoo-wrapped-2024/?utm_source=openai).

- Rydoo actively expanded its product offerings with AI features, launching Rydoo Smart Audit in 2024, an AI-powered expense monitoring assistant that automatically flags non-compliant expenses (https://www.rydoo.com/inside-rydoo/rydoo-wrapped-2024/?utm_source=openai). The company also integrates Rydoo Cards for end-to-end spend management and maintains an extensive integrations marketplace with ERP/Accounting, HR, and tax partners, including Microsoft Dynamics 365, NetSuite, and SAP S/4HANA (https://www.rydoo.com/partners/?utm_source=openai).

- Rydoo operates a global partner network encompassing Finance/Accounting, Travel, HR, VAT recovery, Card transactions, and Technology partners, exemplified by its Microsoft Co-Sell status (https://www.rydoo.com/de/unternehmen/partners/?utm_source=openai).

- CEO Sebastien Marchon and the leadership team publicly discussed the company's growth strategy, profitability, and AI investments, emphasizing AI's role in spend management (https://www.rydoo.com/inside-rydoo/rydoo-turns-5-journey/?utm_source=openai). Key dates include June 19, 2024, for Eurazeo's majority stake investment (https://www.eurazeo.com/en/newsroom/press-releases/eurazeo-invests-rydoo-fast-growing-international-expense-management?utm_source=openai), July 25, 2025, for the acquisition of Semine (https://www.fusacq.com/buzz/semine-rejoint-le-portefeuille-de-solutions-de-rydoo-a254301_fr_?utm_source=openai), and a December 20, 2024, wrap-up report highlighting product milestones like Rydoo Smart Audit (https://www.rydoo.com/inside-rydoo/rydoo-wrapped-2024/?utm_source=openai).

- T4_ScaleUp PE Eurazeo; Semine acq AI expense.

- Integration.

- Acquisition Onfly: LatAm Hunted expense.

- Acquisition Spendesk: Profitable scale-up.

- Coupa tuck-ins.

Chrome River

T4

Unknown

$5B

🟦

Diff: 4

Meta Grid

Founding: Unknown | Funding: Unknown | Investors: Argentum, First Analysis (prior)

Description: Chrome River provides cloud-based expense management solutions, now operating as a product under Emburse.

Weak Signals

- Chrome River, now operating as a product under Emburse, maintained no independent funding rounds, market capitalization, or dedicated M&A strategy for 2024–2025 due to its integration within a private company structure. Chrome River's last documented standalone funding event was on May 11, 2012, when Argentum and First Analysis invested to support its growth (https://argentumgroup.com/argentum-fac-invest-in-chrome-river/?utm_source=openai).

- As Chrome River is now a product within Emburse, a private company, no independent 2024 or 2025 funding rounds, market capitalization, or cash-on-hand figures are publicly disclosed for Chrome River itself (https://argentumgroup.com/argentum-fac-invest-in-chrome-river/?utm_source=openai).

- No publicly documented M&A targets or an explicit "Chrome River M&A strategy" were found for 2024–2025. Any strategic moves at this product level would be integrated into Emburse's broader corporate activities, which are typically not publicly disclosed due to its private status (https://argentumgroup.com/argentum-fac-invest-in-chrome-river/?utm_source=openai).

- Chrome River, initially focused on cloud-based expense management, does not have widely publicized, Chrome River–specific patent grants for 2024–2025. While intellectual property likely exists under the Emburse umbrella, no standalone patent portfolio for Chrome River is readily accessible in public sources (https://argentumgroup.com/argentum-fac-invest-in-chrome-river/?utm_source=openai).

- No verifiable, public Chrome River–specific CEO interviews or partner announcements from 2024–2025 were identified. Any such communications would typically fall under Emburse's overarching corporate messaging (https://argentumgroup.com/argentum-fac-invest-in-chrome-river/?utm_source=openai).

- T4_ScaleUp Emburse product.

- No independent strategy.

- Acquisition Medius: AP automation.

- Expensify/Rydoo.

Expensify

T2

USA

$5B

🟦

Diff: 4

Meta Grid

Founding: Unknown | Funding: N/A | Investors: N/A

Description: Expensify is a public corporate expense management software company.

Weak Signals

- Expensify (EXFY) focused on internal cash flow and strategic investments in 2024–2025, becoming debt-free, with a market capitalization fluctuating in the low hundreds of millions of USD. Expensify did not conduct new equity funding rounds in 2024 or 2025, instead focusing on internal cash flow and strategic investments. The company reportedly became debt-free in 2024, emphasizing a cash-focused balance sheet (https://www.beyondspx.com/quote/EXFY/analysis/expensify-s-ai-first-turnaround-why-the-chat-centric-strategy-could-redefine-expense-management-nasdaq-exfy?utm_source=openai).

- Public disclosures centered on quarterly results, free cash flow, and strategic marketing initiatives (https://investors.expensify.com/news-releases/news-release-details/expensify-announces-q2-2025-results?utm_source=openai). As of early 2026, Expensify's market capitalization was estimated in the low hundreds of millions USD, ranging from approximately $118–$129 million (February 2026), with late 2025 estimates placing it around $140–$180 million (https://stockanalysis.com/stocks/exfy/market-cap/?utm_source=openai; https://www.marketcapwatch.com/company/expensify-marketcap?utm_source=openai). Cash and equivalents were in the tens of millions through 2024–2025, with Q3 2025 figures around $60 million, consistent with an operation prioritizing cash usage over debt (https://businessquant.com/metrics/exfy/cash-and-equivalents?utm_source=openai).

- No widely publicized, finalized M&A deals involving Expensify were reported in 2024–2025. The company's communications prioritized product evolution (AI/chat-centric enhancements), partnerships, and strategic brand initiatives over acquisitions (https://investors.expensify.com/news-releases/news-release-details/expensify-announces-q2-2025-results?utm_source=openai).

- Expensify maintains an active patent portfolio, including patents issued in 2025 related to chat management and voice-interactive systems, indicating ongoing intellectual property development in its AI-enabled expense management stack (https://patents.justia.com/assignee/expensify-inc?utm_source=openai). A broader IP and trademark portfolio exists across its software domain (https://www.crunchbase.com/organization/expensify-com/tech_details?utm_source=openai).

- Expensify’s investor communications in 2024–2025 highlighted strategic marketing investments (e.g., Expensify Travel, card programs, F1 sponsorship) as growth drivers. CEO commentary emphasized AI-first development, unit economics, and a long-term approach to profitability and share repurchases, rather than M&A activity (https://investors.expensify.com/news-releases/news-release-details/expensify-announces-q2-2025-results?utm_source=openai). No definitive CEO statements named specific acquisition targets or M&A roadmaps in this period (https://investors.expensify.com/news-releases/news-release-details/expensify-announces-q2-2025-results?utm_source=openai).

- T2_Large public; debt-free AI expense patents.

- Market cap low $100M.

- Acquisition Zoho Expense: Integrate into larger suite.

- Rydoo/SAP Concur.

Onfly

T5

BRA

$15M

🟨