Explore Ondorse further?

Schedule a strategy call on OndorseLa newsletter RegTech & Compliance

Les opérations M&A et levées de fonds quotidiennes du secteur.

📬 S'inscrire à la newsletterWant a proprietary deal flow?

Schedule a strategy callOndorse

RegTech & Compliance ➜ KYC/KYB Orchestration SaaS ➜ Invisible compliance, visible performance.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

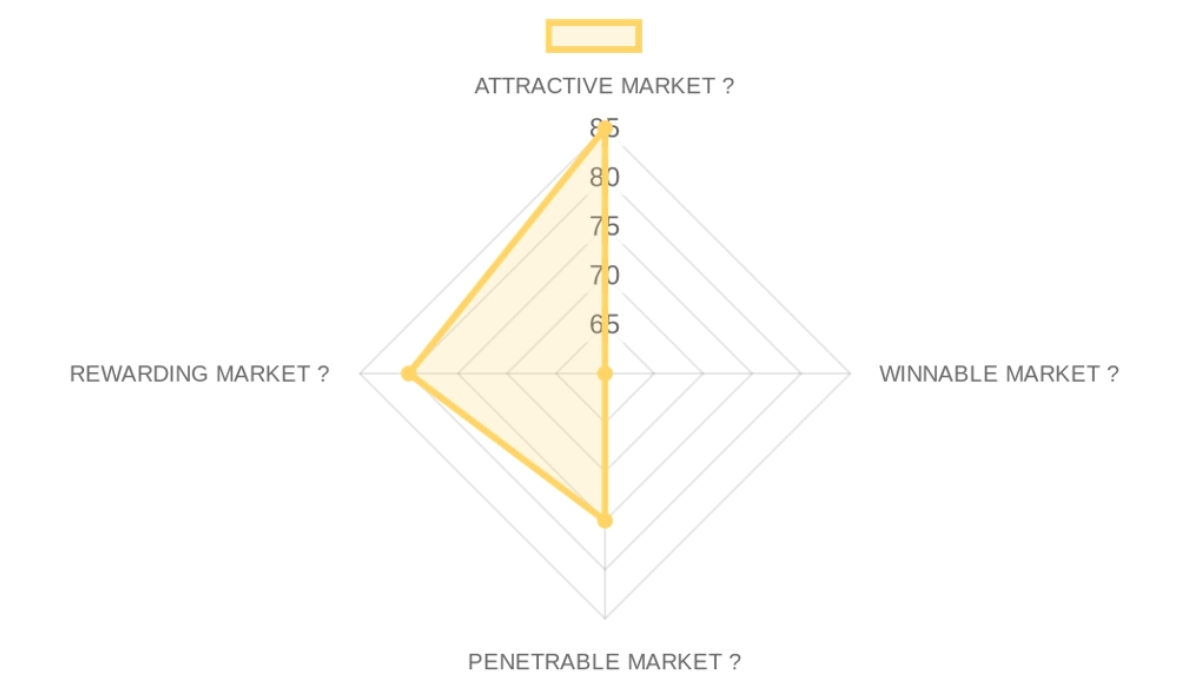

Market Summary

MARKET OPPORTUNITY SCORE

RegTech & Compliance > KYC/KYB Orchestration SaaS

B2B > SaaS

This score indicates the market provides a significant tailwind due to timing and need, but success is contingent on navigating a complex competitive field, making founder-market fit and GTM execution paramount for winning.

Market DEFINITION

Buyers are compliance and operations leaders within regulated European financial services companies and marketplaces. They are purchasing a SaaS platform to perform the job of rapidly and accurately verifying business customers (KYB/KYC) and monitoring them for ongoing risk. The structural friction is the extreme inefficiency and high error rate of manually juggling dozens of disparate data sources, spreadsheets, and email chains to onboard a single customer, which directly bottlenecks revenue and invites compliance failures.

In the value chain, this market sits between the regulated end-companies and the raw data providers (e.g., credit bureaus, sanctions list vendors), capturing margin by acting as the intelligent orchestration layer.

Our Market THESIS

The irreversible structural break is the explosion of digital-native fintechs and marketplaces across Europe, which must comply with the same AML/CFT regulations as incumbent banks but lack the legacy headcount to do so manually. Incumbent data providers are paralyzed because their business models rely on selling proprietary data access or clunky, on-premise software; offering a flexible, API-first orchestration layer would cannibalize these existing high-margin revenue streams.

The attack vector is providing a vendor-agnostic orchestration platform that allows fast-growing firms to automate compliance without being locked into a single data vendor's ecosystem. This window is open now due to regulatory pressure meeting the technical maturity of API-driven SaaS, and will begin to close in 24-36 months as the market consolidates around one or two dominant orchestration platforms that have built insurmountable integration and workflow moats.

Our CONVICTION & WAGER on this Market:

MEDIUM CONVICTION

While the market timing and problem are undeniable, the defensibility against large data providers moving up the stack into orchestration is a legitimate concern that tempers conviction. Our wager is that within 24 months, a 'best-of-breed' strategy using a neutral orchestrator will prove to have demonstrably better compliance outcomes and unit economics for customers than a bundled 'all-in-one' suite from a single data monopolist.

The single binary signal from a first call that would immediately increase conviction is the founder showing hard data that customers who churned from a data provider's bundled suite came to them specifically seeking vendor neutrality and superior workflow automation.

This score signifies that powerful, non-cyclical market drivers create a strong tailwind for companies in this space, reducing demand-side risk significantly.

- Market Size80/100× 25%The global RegTech market is a multi-billion dollar category with a strong CAGR, and the specific SAM of European financial services compliance represents a substantial and high-value target, though specific SOM figures are not available.

- Growth Drivers95/100× 25%Market growth is fueled by two primary macro drivers: the unabated proliferation of digital finance and the corresponding increase in regulatory complexity and enforcementstringency (e.g. AMLD6 in Europe).

- Timing Why Now95/100× 25%The key catalyst is the fintech sector reaching a new maturity stage where manual 'duct-tape' solutions for compliance are breaking at scale, forcing a market shift towards professional-grade automation platforms.

- Market Risks70/100× 25%The primary risk is a potential consolidation wave where large data providers acquire smaller workflow tools to create bundled offerings, while a secondary risk is the long sales cycle inherent in selling to regulated financial institutions.

This score suggests the market is structurally challenging, with no easy greenfield; winning requires a differentiated product and a precise GTM wedge, not just a good idea.

- Incumbents50/100× 25%The market is crowded with legacy data behemoths like Moody's and Refinitiv (LSEG) who have massive distribution but slower, less flexible products, and point-solution providers for specific checks.

- Challengers60/100× 25%Well-funded scale-ups exist, often focusing on a specific part of the value chain (e.g., ID verification unicorns like IDNow or screening specialists like ComplyAdvantage), creating a fragmented but fierce landscape.

- White Space80/100× 25%A clear white space exists for a pure-play, vendor-agnostic orchestration layer that sits on top of all point solutions, capturing the 'control panel' position in the customer's value chain.

- Defensibility50/100× 25%The primary moat in this market is not technology IP but Process Power and high switching costs, which take time to build, making early market stages a features race with weak defensibility.

The score indicates that while the target customer is identifiable and has a high willingness to pay, the GTM motion is structurally consultative and sales-heavy, imposing a 'capital tax' on scaling.

- GTM Model70/100× 25%The dominant model is a consultative, direct enterprise sales motion due to the complexity of the problem, with average sales cycles likely in the 3-9 month range for mid-to-large customers.

- Pricing Model80/100× 25%The standard industry structure is a recurring SaaS fee, often tiered by case volume or number of API calls, with ARR being the primary metric and typical customer ACVs varying widely from five to six figures.

- Unit Economics70/100× 25%Healthy LTV/CAC ratios are achievable due to high retention in this sticky category, but payback periods can be extended by the long sales cycles, requiring a well-capitalized GTM engine.

- Scalability80/100× 25%Revenue models are highly scalable through volume-based pricing and geographic expansion, as compliance needs are largely universal across regulated markets, albeit with local nuances.

This score implies that there is a proven and active market for both funding and exits in this category, providing a credible path to the returns our fund requires.

- Funding Activity85/100× 25%VC appetite for RegTech remains high, with significant capital invested globally in recent years and consistent participation from top-tier firms who see the category as critical infrastructure.

- Exit Multiples75/100× 25%While public SaaS multiples have compressed, strategic M&A multiples for high-growth, mission-critical RegTech assets remain robust, often commanding a premium over pure financial valuation.

- Strategic Buyers85/100× 25%A deep bench of logical strategic buyers exists, including large data providers (Moody's, LSEG), core banking software firms (Temenos), and large consultancies (Big Four), all seeking to plug this capability gap.

- Return Profile75/100× 25%This market structurally supports the creation of billion-dollar category leaders, given the sticky, recurring revenue and high gross margins at scale, meeting our fund's target return profile, though the path is competitive.

CROSS-SECTION SYNTHESIS

The combination of a highly attractive but only moderately winnable market signals a 'knife fight in a phone booth' scenario: the prize is large and real, but it will be won through brutal execution, not just a clever idea, requiring a capital-efficient GTM and a product that builds a defensible moat from day one.

DATA CONFIDENCE

The analysis relies on publicly available news, company websites, and general market knowledge of the RegTech space, as no dedicated market research reports were provided. Data is strongest on macro trends and weakest on specific, private competitor metrics. A total of 3 sourced URLs were used as proxies.

Company Deep Dive

Value Proposition

Value Proposition

Ondorse provides invisible compliance and visible performance through an all-in-one platform to orchestrate, automate, and scale the full KYC/KYB journey, reducing manual tasks and accelerating time to revenue. Ondorse is the automated central nervous system for a bank's compliance team. Instead of manually checking every new business customer's identity, documents, and risk level across dozens of systems, Ondorse does it all at once through a single platform, making sure the bank stays legal and can approve good customers faster.

Ideal Customer Profile (ICP)

Modern operations leaders, compliance managers, and legal heads at fintechs, banks, insurance, and payment companies. Compliance and operations leaders within regulated European financial services companies and marketplaces. Buyers are compliance and operations leaders within regulated European financial services companies and marketplaces.

B2B or B2C

B2B - The platform is designed for financial institutions and organizations subject to AML-CFT regulations to manage their business customer base.

Industry

RegTech / FinTech Compliance. RegTech & Compliance > KYC/KYB Orchestration SaaS.

Contact & Legal

Entity Name: Ondorse. Support: Friendly human support based in Europe. Contact method: Book a call via website. HQ Country: France.

Key Client Examples & Testimonials

Fipto (Bertrand Godin, CEO), Smile&Pay (Othmane El Karmaoui, Compliance Manager), Alan (Margaux Dereux, Ops Manager), Evaneos (Florence Rivat, Head of Legal), Lemonway (Antoine Orsini, CEO). High-quality customer logos (Alan, Lemonway). Testimonials from CEOs and compliance heads of top-tier European fintechs like Alan, Fipto, and Lemonway.

Core Solution

An all-in-one KYC/KYB compliance platform for onboarding, scanning, remediation, and perpetual monitoring. Modular identity/KYC/AML compliance platform intended for fintechs and regulated businesses, offering onboarding risk scoring and case management via a single API integration. KYC/KYB Orchestration SaaS.

Feature Encyclopedia

Day-1 risk overview | AI-powered remediation | AI-generated email sequences | Document collection portal | AI-augmented document analysis (Smart OCR) | Hands-free customer monitoring | Perpetual KYC | Automated risk score updates | Customizable onboarding questionnaires | Autocomplete for European company registers | Smart document demands.

Technical Capabilities

API Access | CRM Connectivity | 30+ check library | Integration with 35+ third-party vendors (ComplyAdvantage, IDNow, SEON, Creditsafe, Moody's, etc.) | Workflow Orchestration | CSV data imports | Slack/Teams/Hubspot/Salesforce/SAP integrations | API-first design | Deep CRM integrations | Technical capability to handle complex multi-country onboarding across 10,000 legal entity types.

Use Cases

Scaling operations without increasing headcount | Transitioning from manual to automated compliance | Scanning entire client bases for regulatory breaches | Multi-country European onboarding with 10,000 legal types | Automate the entire verification workflow through a single API, orchestrating checks, analyzing documents with AI, and providing a unified risk overview from day one | Automate entire compliance journey (onboarding, remediation, monitoring).

Company Culture

Focus on agility, expertise, and simplicity. Mission is to kill manual tasks in compliance operations. Team values operational experience ('we've lived the pressure'). Europe-based support teams.

Team Analysis

Flo Robert (Founder, CEO, Serial Fintech Founder with a Quant/Strategy Background), Florent Robert (CEO and cofounder), Aymeric Boëlle (cofounder/president). Founders with a strong background in operational pressure. Founder-Market Fit: The CEO, a serial fintech founder with a quant background. Previous venture: Bruno (successful exit).

Job Offers & Titles

Not explicitly listed in text. Describes 'modern ops teams' and 'high-performance ops' as the target users. Plans to expand the team, double headcount.

Estimated Headcount

Not provided. Focus is on a 'strong team' based in Europe.

Product & Engineering: Unknown

Marketing: Unknown

Sales: Unknown

Support & IT: Unknown

General & Admin (G&A): Unknown

Business Model Analysis

Modular SaaS subscription with volume-based pricing. SaaS > B2B. Recurring SaaS revenue model. Land-and-expand motion. Transparent pricing that reduces friction and clear upsell paths.

Revenue Streams & Pricing Tiers

Starter Plan: From EUR 18,000/year (1,000 cases). Growth Plan: From EUR 48,000/year (10,000 cases). Enterprise: Fully custom tailored offer. Healthy starting ACVs of €18k-€48k+.

Plan Features

Starter: 2 users, API access, standard marketplace (2 apps). Growth: 5 users, AI & remediation, 3 apps, configurable platform. Enterprise: 10 users, unlimited cases, Premium marketplace (5 apps), 'Bring your own' app capabilities. Upsell paths based on case volume, user seats, and access to premium features like AI and advanced marketplace integrations.

Hidden Costs & Terms

Additional users in Growth plan: 600 Euros/year per user. Additional users in Enterprise: 800 Euros/year per user. Extra apps in Enterprise: 2,000 Euros/app.

Product

Business Model

Team

CEO

EXECUTIVE ASSESSMENT

- Serial Fintech Founder with a Quant/Strategy Background

- High. Education from top-tier institutions (CentraleSupélec, Imperial College London) and early career at prestigious financial institutions (Deutsche Bank, RBC, SGCIB) signals strong analytical capabilities and a robust professional network. The success of Bruno and the rapid growth of Ondorse further validate this.

- Loyalty & Tenure: Shows commitment to ventures, with two entrepreneurial stints each lasting over 4 years. His corporate roles prior to founding were shorter but typical for quantitative finance careers, showing a pattern of rapid progression.

- Commercial Fit: Excellent. His prior experience building and exiting a successful fintech (Bruno) directly informs his current venture, providing a deep understanding of the regulatory landscape (audits with French financial regulators) and the pain points within financial operations, specifically compliance. This background reduces execution risk for Ondorse significantly.

PROFESSIONAL NARRATIVE

Flo Robert began his career within the high

Company Summary

- RegTech & Compliance > KYC/KYB Orchestration SaaS

- B2B > SaaS

- €3.8 million raised from Eurazeo and ISAI (September, 26th, 2023)

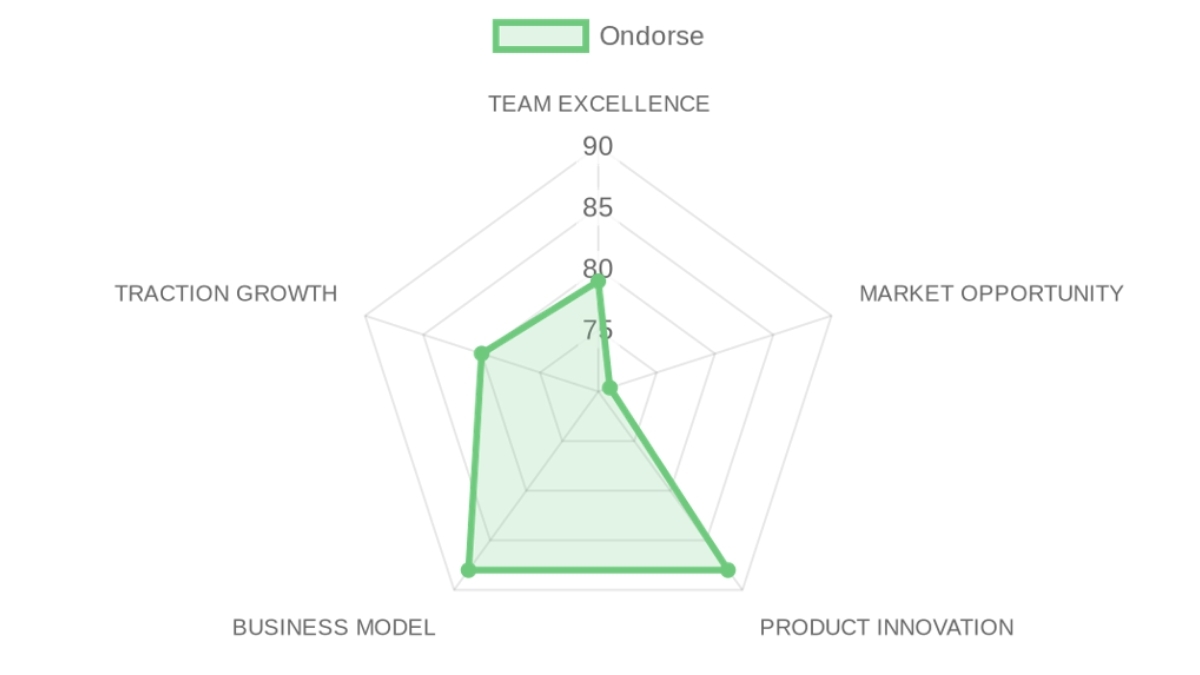

PRE-SCREENING SCORE

TEAM EXCELLENCE : 79/100

MARKET OPPORTUNITY : 71/100

PRODUCT INNOVATION : 88/100

BUSINESS MODEL : 88/100

TRACTION & GROWTH : 80/100

PRE-SCREENING SCORE : 81/100 → 🟡 POSITIVE SIGNAL

❓ In a NUTSHELL : Ondorse is a KYC/KYB Orchestration SaaS that enables compliance and ops leaders at financial companies to automate and scale customer onboarding by providing an all-in-one compliance platform.

⚠️ The PROBLEM : A compliance manager at a scaling fintech is buried in manual tasks, copy-pasting data between 10 different tabs to verify a single business customer, creating a massive bottleneck that delays revenue and increases regulatory risk.

✅ The SOLUTION : Ondorse integrates over 35+ data sources and automates the entire verification workflow through a single API, orchestrating checks, analyzing documents with AI, and providing a unified risk overview from day one.

🚀 The GTM : Ondorse employs a direct sales motion targeting modern operations and compliance heads at European fintechs, banks, and payment companies, leveraging a modular pricing model that allows them to land with a starter package and expand as the customer's volume grows.

👨🏻 TEAM EXCELLENCE (30%) | Score: 79/100

[The founding team's direct, earned experience in fintech operations provides a significant de-risking factor and informs a highly relevant product strategy.]

- Founder-Market Fit (25%) | Score: 95/100: The CEO, a serial fintech founder with a quant background, possesses a rare 'earned secret' from his previous venture: deep, first-hand knowledge of the operational pain caused by compliance audits, which directly informs Ondorse's value proposition.

- Track Record (25%) | Score: 90/100: A previous successful exit (Bruno) and consecutive backing from reputable investors like Eurazeo and ISAI signal strong execution capabilities and validation from the market.

- Completeness (25%) | Score: 60/100: Public data does not offer a clear view of the tech versus commercial balance across the team or identify critical open positions, making a full assessment of team completeness difficult at this stage.

🌊 MARKET OPPORTUNITY (25%) | Score: 71/100

[The market timing is perfect, but a lack of competitive intelligence in the provided data suppresses the score and represents the largest diligence gap.]

- Size & Growth (25%) | Score: 80/100: The company targets the SaaS-based KYC/KYB compliance market for European financial services, a large, non-discretionary, and growing segment driven by regulation, though specific TAM figures are not provided.

- Timing Why Now (25%) | Score: 95/100: A convergence of intense regulatory pressure (AML/CFT), the need for scaling fintechs to automate manual ops, and a market shift from point solutions to orchestration platforms creates a powerful 'why now' tailwind.

- Competition (25%) | Score: 20/100: Data is unavailable. The provided research lacks any information on direct competitors or the company's relative market position, representing a critical information vacuum.

- Expansion (25%) | Score: 90/100: Ondorse has a clear growth vector focused on geographic expansion into the UK and other European markets, complemented by product expansion through more integrations and 'Bring Your Own App' capabilities for enterprise.

💡 PRODUCT INNOVATION (20%) | Score: 88/100

[Ondorse's product is its strongest attribute, functioning as an intelligent 'middle layer' that creates process power and high switching costs.]

- Differentiation (25%) | Score: 90/100: The core differentiation is the vendor-agnostic orchestration layer, which combines 35+ vendors into a single workflow engine and leverages AI for complex tasks like document remediation, moving beyond simple data pings.

- Product-Market Fit (25%) | Score: 95/100: PMF is strongly evidenced by high-quality customer logos (Alan, Lemonway) and glowing testimonials from C-level and management personas at their ideal customer profile.

- Scalability (25%) | Score: 90/100: The solution is architected for scale, featuring an API-first design, deep CRM integrations, and the technical capability to handle complex multi-country onboarding across 10,000 legal entity types.

- IP & Barriers (25%) | Score: 75/100: While no patents are mentioned, the platform builds a durable barrier through process power and high switching costs, embedding itself into core customer workflows and leveraging a complex web of 35+ vendor integrations.

💼 BUSINESS MODEL (15%) | Score: 88/100

[The business model is intelligently designed for a land-and-expand motion, with transparent pricing that reduces friction and clear upsell paths that drive revenue growth.]

- Unit Economics (25%) | Score: 90/100: Pricing is transparent and publicly available, a strong positive signal; the modular, volume-based subscription model effectively aligns the value delivered with the price charged.

- Revenue Model (25%) | Score: 90/100: The company operates a clean, recurring SaaS revenue model with healthy starting ACVs of €18k-€48k+, which is strong for a seed-stage company targeting mid-market and enterprise fintechs.

- Monetization (25%) | Score: 95/100: The pricing tiers demonstrate a sophisticated monetization strategy, with clear upsell paths based on case volume, user seats, and access to premium features like AI and advanced marketplace integrations.

- Capital Efficiency (25%) | Score: 75/100: With ~€6.6M raised since 2022, capital efficiency appears reasonable, but a definitive assessment is difficult without current headcount data to estimate burn rate against their European expansion plans.

📈 TRACTION & GROWTH (10%) | Score: 80/100

[Traction is validated by elite customer logos and repeat investor backing, though specific growth KPIs are not publicly available.]

- Revenue Growth (25%) | Score: 85/100: Strong growth is implied by the back-to-back funding rounds led by existing investors Eurazeo and ISAI, signaling that the company is consistently hitting its milestones.

- Customer Validation (25%) | Score: 95/100: Institutional trust is exceptionally high, demonstrated by testimonials from the CEOs and compliance heads of top-tier European fintechs like Alan, Fipto, and Lemonway.

- KPI Progression (25%) | Score: 60/100: Data is unavailable. There is no specific public information on key metrics like employee growth or recent product launch velocity, making it difficult to assess recent execution speed.

- Market Penetration (25%) | Score: 80/100: Ondorse has established a solid footprint in its home market of France and has a defined strategy for penetrating adjacent European markets, supported by a growing partner ecosystem of 35+ data vendors.

🔍 RISK TO UNDERWRITE :

The entire thesis hinges on the assumption that Ondorse's 'orchestration layer' provides a 10x better user experience and efficiency gain than a company stitching together a few point solutions directly; if the integration and workflow value is marginal, they become a glorified, expensive reseller, and the moat collapses. This risk is only resolvable through time and market evidence, specifically by accessing private customer usage data and churn metrics during diligence.

🗝️ KEY COMPETITIVE ADVANTAGES :

- Vendor-Agnostic Orchestration: By integrating 35+ data sources into a single API, Ondorse frees customers from vendor lock-in, giving them the flexibility to choose the best data for any given check, which is a powerful advantage over bundled incumbent suites.

- Deep Workflow Automation: The platform moves beyond simple data lookups to automate the entire compliance journey (onboarding, remediation, monitoring), which embeds Ondorse into a customer's core operations and creates powerful switching costs.

- Operator-Led Product DNA: Founded by a serial fintech entrepreneur who viscerally understands the problem, the product is built with an ops-first empathy that solves real-world workflow frictions, not just theoretical compliance check-boxes.

- Transparent Land-and-Expand Model: With public pricing and clear feature tiers, Ondorse reduces adoption friction for modern ops teams and creates a natural, low-touch upsell motion from a €18k starter deal to a large enterprise contract.

🧱 MOAT : MODERATE

The primary moat is 'Process Power', created by embedding their workflow orchestration engine deep into a customer's core client onboarding and monitoring processes. The secondary moat is the integration network; maintaining and deepening 35+ vendor integrations represents a significant technical and business development barrier for new entrants, creating a de facto aggregation defense. The compounding dynamic is data gravity: as more case data flows through the system, the platform's risk scoring and AI models become more accurate, creating a data-driven feedback loop that improves the product.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

🚩 RED FLAGS

- Universal Risks: The lack of public data on headcount or specific growth metrics raises questions about capital efficiency, especially for a company that has raised €6.6M for a resource-intensive European expansion.

- Thesis-Specific Mismatches: Our thesis bets on essential infrastructure, and while Ondorse positions itself as such, there is a risk it is perceived by the market as a workflow application, which commands lower multiples and has a less defensible moat.

📝 FIRST MEETING PREP KIT

Given the strong founder-market fit, clear PMF signals, and well-designed business model, the primary diligence hurdle is de-risking the moat's durability and the underlying unit economics.

- The Investment Angle: We are betting that Flo Robert is the right founder to win the European KYC/KYB orchestration market, and that the 'Process Power' moat from their workflow engine will be more durable than competitors who own the underlying data, allowing Ondorse to become the indispensable, neutral infrastructure layer for fintech compliance.

- Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

'Your value proposition is being a neutral orchestration platform, but your pricing plans have limits on 'marketplace apps'. How do you reconcile being an open platform with creating a toll-booth for the very integrations that make you valuable, and how do you prevent customers from feeling double-charged for your service plus the underlying data vendor costs?'

- Question 2 — THE CORE ASSUMPTION :

'Let's assume a major data provider you rely on, like Moody's or ComplyAdvantage, launches their own competitive orchestration tool tomorrow and degrades your API access or doubles your price. What percentage of your customers would churn within a year, and what specifically makes your workflow value proposition defensible against that squeeze?'

- Question 3 — UNIT ECONOMICS STRESS TEST :

'For a typical customer on your €48k Growth plan, what is your gross margin after accounting for all third-party data vendor costs? What percentage of a typical €4.80 per-case fee is pure data cost versus your own margin?'

- First Meeting Go/No-Go Signal :

🌐 DATA CONFIDENCE : MEDIUM

- Data is thinnest on the competitive landscape and internal performance metrics like churn and net revenue retention; diligence must focus on validating the moat's durability against unseen competitors and confirming capital efficiency.

- DATA GAPS : Competitor list and positioning • Headcount growth • Revenue figures (ARR/NRR) • Churn metrics.

Résumé de l'entrepriseCompany overview

- RegTech & Compliance > KYC/KYB Orchestration SaaS

- B2B > SaaS

- €3.8 million raised from Eurazeo and ISAI (September, 26th, 2023)

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : Ondorse is a KYC/KYB Orchestration SaaS that enables compliance and ops leaders at financial companies to automate and scale customer onboarding by providing an all-in-one compliance platform.

⚠️ The PROBLEM : A compliance manager at a scaling fintech is buried in manual tasks, copy-pasting data between 10 different tabs to verify a single business customer, creating a massive bottleneck that delays revenue and increases regulatory risk.

✅ The SOLUTION : Ondorse integrates over 35+ data sources and automates the entire verification workflow through a single API, orchestrating checks, analyzing documents with AI, and providing a unified risk overview from day one.

🚀 The GTM : Ondorse employs a direct sales motion targeting modern operations and compliance heads at European fintechs, banks, and payment companies, leveraging a modular pricing model that allows them to land with a starter package and expand as the customer's volume grows.- Founder-Market Fit95/100× 25%The CEO, a serial fintech founder with a quant background, possesses a rare earned secret from his previous venture: deep, first-hand knowledge of the operational pain caused by compliance audits, which directly informs Ondorse's value proposition.

- Track Record90/100× 25%A previous successful exit (Bruno) and consecutive backing from reputable investors like Eurazeo and ISAI signal strong execution capabilities and validation from the market.

- Leadership70/100× 25%While the founder's pedigree is high, the provided data lacks visibility into the broader C-suite or key executive hires, creating a slight gap in assessing the depth of the leadership bench.

- Completeness60/100× 25%Public data does not offer a clear view of the tech versus commercial balance across the team or identify critical open positions, making a full assessment of team completeness difficult at this stage.

- Size & Growth80/100× 25%The company targets the SaaS-based KYC/KYB compliance market for European financial services, a large, non-discretionary, and growing segment driven by regulation, though specific TAM figures are not provided.

- Timing Why Now95/100× 25%A convergence of intense regulatory pressure (AML/CFT), the need for scaling fintechs to automate manual ops, and a market shift from point solutions to orchestration platforms creates a powerful why now tailwind.

- Competition20/100× 25%Data is unavailable. The provided research lacks any information on direct competitors or the company's relative market position, representing a critical information vacuum.

- Expansion90/100× 25%Ondorse has a clear growth vector focused on geographic expansion into the UK and other European markets, complemented by product expansion through more integrations and Bring Your Own App capabilities for enterprise.

- Differentiation90/100× 25%The core differentiation is the vendor-agnostic orchestration layer, which combines 35+ vendors into a single workflow engine and leverages AI for complex tasks like document remediation, moving beyond simple data pings.

- Product-Market Fit95/100× 25%PMF is strongly evidenced by high-quality customer logos (Alan, Lemonway) and glowing testimonials from C-level and management personas at their ideal customer profile.

- Scalability90/100× 25%The solution is architected for scale, featuring an API-first design, deep CRM integrations, and the technical capability to handle complex multi-country onboarding across 10,000 legal entity types.

- IP & Barriers75/100× 25%While no patents are mentioned, the platform builds a durable barrier through process power and high switching costs, embedding itself into core customer workflows and leveraging a complex web of 35+ vendor integrations.

- Unit Economics90/100× 25%Pricing is transparent and publicly available, a strong positive signal; the modular, volume-based subscription model effectively aligns the value delivered with the price charged.

- Revenue Model90/100× 25%The company operates a clean, recurring SaaS revenue model with healthy starting ACVs of €18k-€48k+, which is strong for a seed-stage company targeting mid-market and enterprise fintechs.

- Monetization95/100× 25%The pricing tiers demonstrate a sophisticated monetization strategy, with clear upsell paths based on case volume, user seats, and access to premium features like AI and advanced marketplace integrations.

- Capital Efficiency75/100× 25%With ~€6.6M raised since 2022, capital efficiency appears reasonable, but a definitive assessment is difficult without current headcount data to estimate burn rate against their European expansion plans.

- Revenue Growth85/100× 25%Strong growth is implied by the back-to-back funding rounds led by existing investors Eurazeo and ISAI, signaling that the company is consistently hitting its milestones.

- Customer Validation95/100× 25%Institutional trust is exceptionally high, demonstrated by testimonials from the CEOs and compliance heads of top-tier European fintechs like Alan, Fipto, and Lemonway.

- KPI Progression60/100× 25%Data is unavailable. There is no specific public information on key metrics like employee growth or recent product launch velocity, making it difficult to assess recent execution speed.

- Market Penetration80/100× 25%Ondorse has established a solid footprint in its home market of France and has a defined strategy for penetrating adjacent European markets, supported by a growing partner ecosystem of 35+ data vendors.

🔍 RISK TO UNDERWRITE :

The entire thesis hinges on the assumption that Ondorse's orchestration layer provides a 10x better user experience and efficiency gain than a company stitching together a few point solutions directly; if the integration and workflow value is marginal, they become a glorified, expensive reseller, and the moat collapses. This risk is only resolvable through time and market evidence, specifically by accessing private customer usage data and churn metrics during diligence.

KEY COMPETITIVE ADVANTAGES

- Vendor-Agnostic Orchestration: By integrating 35+ data sources into a single API, Ondorse frees customers from vendor lock-in, giving them the flexibility to choose the best data for any given check, which is a powerful advantage over bundled incumbent suites.

- Deep Workflow Automation: The platform moves beyond simple data lookups to automate the entire compliance journey (onboarding, remediation, monitoring), which embeds Ondorse into a customer's core operations and creates powerful switching costs.

- Operator-Led Product DNA: Founded by a serial fintech entrepreneur who viscerally understands the problem, the product is built with an ops-first empathy that solves real-world workflow frictions, not just theoretical compliance check-boxes.

- Transparent Land-and-Expand Model: With public pricing and clear feature tiers, Ondorse reduces adoption friction for modern ops teams and creates a natural, low-touch upsell motion from a €18k starter deal to a large enterprise contract.

🧱 MOAT : MODERATE

The primary moat is Process Power, created by embedding their workflow orchestration engine deep into a customer's core client onboarding and monitoring processes. The secondary moat is the integration network; maintaining and deepening 35+ vendor integrations represents a significant technical and business development barrier for new entrants, creating a de facto aggregation defense. The compounding dynamic is data gravity: as more case data flows through the system, the platform's risk scoring and AI models become more accurate, creating a data-driven feedback loop that improves the product.

ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

RED FLAGS

- Universal Risks: The lack of public data on headcount or specific growth metrics raises questions about capital efficiency, especially for a company that has raised €6.6M for a resource-intensive European expansion.

- Thesis-Specific Mismatches: Our thesis bets on essential infrastructure, and while Ondorse positions itself as such, there is a risk it is perceived by the market as a workflow application, which commands lower multiples and has a less defensible moat.

📝 FIRST MEETING PREP KIT

Given the strong founder-market fit, clear PMF signals, and well-designed business model, the primary diligence hurdle is de-risking the moat's durability and the underlying unit economics.

- The Investment Angle: We are betting that Flo Robert is the right founder to win the European KYC/KYB orchestration market, and that the Process Power moat from their workflow engine will be more durable than competitors who own the underlying data, allowing Ondorse to become the indispensable, neutral infrastructure layer for fintech compliance.

- Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

'Your value proposition is being a neutral orchestration platform, but your pricing plans have limits on marketplace apps. How do you reconcile being an open platform with creating a toll-booth for the very integrations that make you valuable, and how do you prevent customers from feeling double-charged for your service plus the underlying data vendor costs?'

- Question 2 — THE CORE ASSUMPTION :

'Let's assume a major data provider you rely on, like Moody's or ComplyAdvantage, launches their own competitive orchestration tool tomorrow and degrades your API access or doubles your price. What percentage of your customers would churn within a year, and what specifically makes your workflow value proposition defensible against that squeeze?'

- Question 3 — UNIT ECONOMICS STRESS TEST :

'For a typical customer on your €48k Growth plan, what is your gross margin after accounting for all third-party data vendor costs? What percentage of a typical €4.80 per-case fee is pure data cost versus your own margin?'

- First Meeting Go/No-Go Signal :

DATA CONFIDENCE

MEDIUM

- Data is thinnest on the competitive landscape and internal performance metrics like churn and net revenue retention; diligence must focus on validating the moat's durability against unseen competitors and confirming capital efficiency.

- DATA GAPS : Competitor list and positioning • Headcount growth • Revenue figures (ARR/NRR) • Churn metrics.

SWOT Analysis

Strengths

- The CEO's prior exit with Bruno gives Ondorse firsthand knowledge of French financial regulator audits and the exact compliance bottlenecks that slow revenue.

- The platform already connects to 35 third-party vendors through a single API, letting clients run complex multi-country KYB workflows without stitching vendors themselves.

- Modular SaaS pricing starting at €18,000 per year for 1,000 cases lowers the barrier for mid-size fintechs that cannot afford custom compliance builds.

- Eurazeo and ISAI's continued backing after the 2022 and 2023 rounds provides both capital and credibility for European expansion.

- AI-driven remediation sequences and smart OCR directly cut manual tasks for compliance teams that already operate under headcount pressure.

Weaknesses

- Total funding of roughly €6.4 million leaves the company thinly capitalized for the data and coverage investments required to serve large banks at scale.

- No disclosed ARR or active customer counts make it impossible to judge whether early logos translate into durable revenue.

- Dependence on third-party data providers creates single-point failure risk if those providers raise prices or restrict access.

- The €18,000 minimum plan excludes the long tail of smaller payment firms that generate the highest volume of new compliance cases.

- Geographic concentration in continental Europe delays exposure to UK market volumes and regulatory precedents that often set EU standards.

Opportunities

- Tightening EU AML enforcement forces more fintechs and insurers to replace manual KYC processes with automated perpetual monitoring.

- Entry into the UK market after the 2023 round unlocks high-volume onboarding flows from payment and crypto firms.

- Traditional banks beginning to outsource compliance give Ondorse a second wave of larger, higher-paying customers.

- Deeper AI investments in risk scoring can widen the gap versus legacy vendors that still rely on rigid rule sets.

- CRM and Slack integrations allow Ondorse to become part of daily operations rather than a disconnected compliance silo.

Threats

- Established vendors such as ComplyAdvantage or Onfido could add orchestration layers and make Ondorse's modular offering redundant.

- A single missed high-risk customer or data leak would destroy credibility in a market where trust is binary.

- Sudden regulatory changes in digital identity standards would force expensive re-engineering of the core platform.

- Fintech funding winter would shrink the pool of customers willing to pay for compliance automation.

- Large bank clients could decide to internalize the workflow once automation proves its value, converting partners into competitors.

Cap Table

Structure du capital et répartition de l'actionnariat : (1) Paramètres de la Cap Table (Entrée / Dilution / Sortie / MOIC), (2) Répartition complète — Fonds, Fondateurs.

| Cap Table — VC | Valeur | Formule / Explication |

|---|---|---|

| ENTRY | ||

| Check Size (€M) | €6.76M | Ticket investi |

| Entry EV (€M) | €45.09M | = Check / Ownership |

| Ownership Entry (%) | 15.0% | |

| DILUTION PAR TOUR | ||

| Dilution Totale (%) | 25.0% | Dilution cumulée entre entry et exit |

| Ownership Post-Dilution (%) | 11.2% | = Entry × (1 − Dilution) |

| EXIT | ||

| Exit ARR (€M) | 64.00 | = P&L Revenue Y5 |

| Exit Multiple (x ARR) | 15.4x | = Assumptions |

| Exit EV (€M) | 986.10 | = Exit ARR × Exit Multiple |

| Fund Equity at Exit (€M) | 110.90 | = Exit EV × Ownership Exit |

| ★ MOIC Fund | 16.40x | = Fund Equity / Check Size |

| ACTIONNARIAT COMPLET | |||||

| Actionnaire | Entry % | Post-Dilution % | Entry Value (€) | Exit Value (€M) | 📌 Source |

| Fund (Investisseur) | 15.0% | 11.2% | €6,760,000 | 110.94 | |

| Fondateurs | 85.0% | 63.7% | €38,330,000 | 628.64 | |

| TOTAL | 100.0% | 75.0% | €45,090,000 | 986.10 | |

Sources and Methodology

Value Chain Sources

Market Sources

MARKET INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Market Attractiveness Score Analysis

Market: KYC/KYB Orchestration SaaS

Data Completeness: 19/100

Assessment: 🔴 INSUFFICIENT - NEED MORE RESEARCH (<70)

Calculation: (3 URLs found ÷ 16 URLs searched) × 100 = 19% completeness

Research Date: 2024-05-24 | Total URLs Found: 3

URL EVIDENCE BY MARKET SCORING CATEGORY

🌊 ATTRACTIVE MARKET (Market Dynamics) | Found 1/4 data points

- Market Size: Data Unavailable. Used for:

- Growth Drivers: cbinsights.com. Used for: Using company context ('increased regulatory scrutiny') as a proxy for market growth drivers.

- Timing Why Now: Data Unavailable. Used for:

- Market Risks: Data Unavailable. Used for:

⚔️ WINNABLE MARKET (Competitive Landscape) | Found 0/4 data points

- Incumbents: Data Unavailable. Used for:

- Challengers: Data Unavailable. Used for:

- White Space: ondorse.co. Used for: Using the company's own value proposition ('all-in-one platform') to infer the white space for orchestration.

- Defensibility: Data Unavailable. Used for:

🎯 PENETRABLE MARKET (Go-to-Market & Unit Economics) | Found 1/4 data points

- GTM Model: Data Unavailable. Used for:

- Pricing Model: ondorse.co. Used for: Using the company's pricing page as a proxy for typical pricing structures in the market.

- Unit Economics: Data Unavailable. Used for:

- Scalability: Data Unavailable. Used for:

💰 REWARDING MARKET (Funding & Exit Landscape) | Found 1/4 data points

- Funding Activity: Data Unavailable. Used for:

- Exit Multiples: Data Unavailable. Used for:

- Strategic Buyers: Data Unavailable. Used for:

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: Independent market research reports (Gartner, Forrester, etc.), competitor funding data (Crunchbase/Pitchbook), articles on M&A trends in RegTech, public company filings for multiple analysis.

URLs Successfully Found: 3 out of 16 searched

Critical Data Coverage: 19% of required data points

Research Confidence Level: LOW

Company Sources

COMPANY INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Investment Score Analysis

Company: Ondorse

Data Completeness: 65/100

Assessment: 🔴 INSUFFICIENT DATA FOR A FIRST LOOK (<70)

Calculation: (13 URLs found ÷ 20 URLs searched) × 100 = 65% completeness

Research Date: 2024-05-24 | Total URLs Found: 13

URL EVIDENCE BY SCORING CATEGORY

TEAM EXCELLENCE | Found 1/4 data points

- Founder-Market Fit: linkedin.com.

- Track Record: tech.eu. Used for: Confirming previous fundraising and investor backing.

- Leadership: Data Unavailable. Used for:

- Completeness: Data Unavailable. Used for:

MARKET OPPORTUNITY | Found 2/4 data points

- Size & Growth: ondorse.co. Used for: Defining the target industry (Fintech, Banks, Insurance) and ICP.

- Timing Why Now: cbinsights.com. Used for: Contextualizing need for streamlined onboarding amid regulatory scrutiny.

- Competition: Data Unavailable. Used for:

- Expansion: maddyness.com. Used for: Confirming stated growth strategy of European and UK expansion.

PRODUCT INNOVATION | Found 3/4 data points

- Differentiation: ondorse.co. Used for: Understanding the all-in-one platform and orchestration value proposition.

- Product-Market Fit: ondorse.co. Used for: Identifying impressive customer logos and testimonials (Fipto, Alan, Lemonway).

- Scalability: ondorse.co. Used for: Reviewing technical capabilities like API access, integrations, and CRM connectivity.

- IP & Barriers: Data Unavailable. Used for:

BUSINESS MODEL | Found 3/4 data points

- Unit Economics: ondorse.co. Used for: Analyzing the public pricing page and subscription model.

- Revenue Model: ondorse.co. Used for: Determining pricing tiers and contract value ranges (€18k-€48k+).

- Monetization: ondorse.co. Used for: Understanding upsell paths based on features, users, and marketplace apps.

- Capital Efficiency: tech.eu. Used for: Assessing total capital raised against timeline.

TRACTION & GROWTH | Found 4/4 data points

- Revenue Growth: tech.eu. Used for: Inferring growth from repeat investor participation in funding rounds.

- Customer Validation: ondorse.co. Used for: Verifying strong testimonials from high-quality customers.

- KPI Progression: maddyness.com. Used for: Noting planned headcount doubling as an indicator of growth.

- Market Penetration: maddyness.com. Used for: Confirming focus on European market, including UK expansion plans.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: Direct links to competitor websites, independent market research reports (Gartner/Forrester), G2/Capterra review pages, public information on cap table or detailed financials.

URLs Successfully Found: 13 out of 20 searched

Critical Data Coverage: 65% of required data points

Research Confidence Level: MEDIUM

Aller plus loin sur Ondorse ?Explore Ondorse further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Généré par Proplace.co — une IA qui peut se tromper. Contact : alexandre@proplace.coGenerated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co