Explore Jrsrecycling further?

Schedule a strategy call on JrsrecyclingSubscribe to the Proplace newsletter?

Subscribe to the newsletterWant a proprietary deal flow?

Schedule a strategy callJrsrecycling

The Physical World ➜ Regional Material Reclamation & Upcycling ➜ Hassle-free regional scrap metal and consumer electronics reclamation with immediate cash payouts

Vous voulez un mémo détaillé et personnalisé sur cette société ?

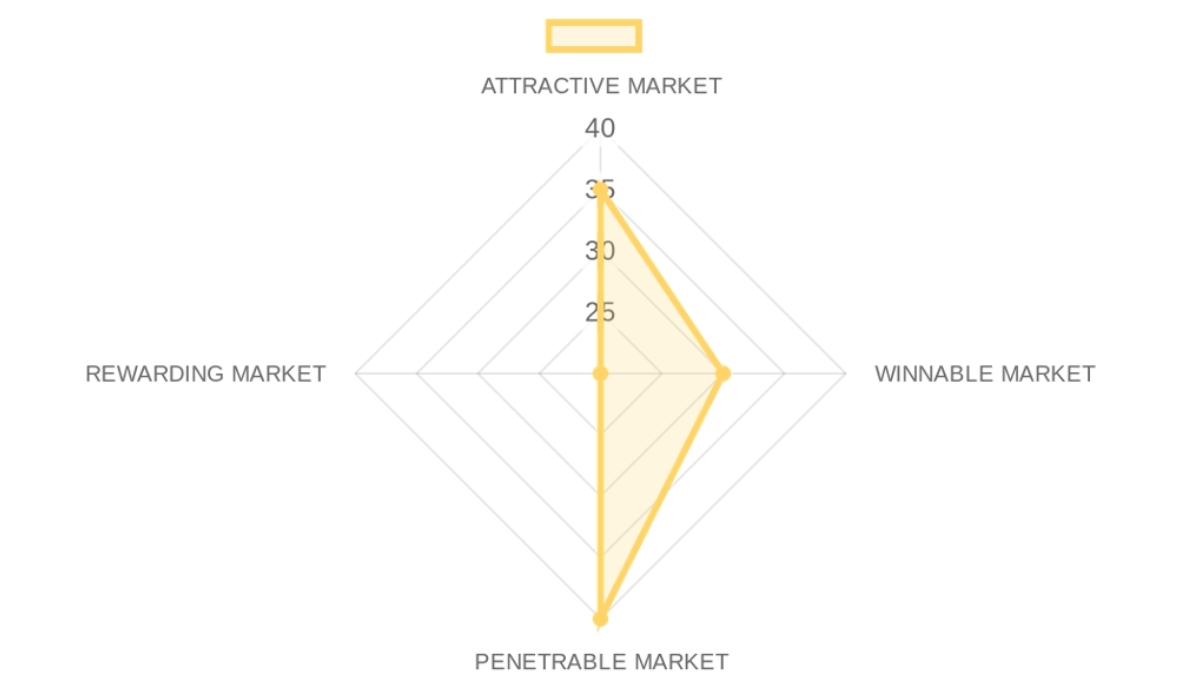

Market Summary

MARKET OPPORTUNITY SCORE

Climate & Energy Tech > Regional Material Reclamation & Upcycling

B2B > Transactional

Market DEFINITION

The market comprises localized, retail-facing physical consolidation networks where individual tradespeople sell end-of-life non-ferrous metals and consumer e-waste for immediate cash compensation. The core structural friction stems from incredibly fragmented and unorganized micro-supply pipelines, which forces retail participants to navigate complex industrial sorting rules and opaque transaction margins under analog yards.

Profit pools concentrate in the massive downstream industrial processors who command centralized sorting infrastructure, leaving regional micro-aggregators perpetually squeezed as low-margin price takers.

Our Market THESIS

The regional scrap metal collection landscape has shifted permanently toward automated operations as wage inflation pressures traditional yard manual processing. Large scale industrial market leaders cannot target this low-volume retail-contractor supply segment profitably, as their legacy centralized logistics yards cannot handle micro-intake without bottlenecking their commercial transport operations.

A nimble player can capture this market by launching decentralized, automated micro-collection depots that bypass industrial middlemen entirely. However, the opportunity window is short-lived and will likely shut over the next 36 months as national environmental software platforms expand their regional collection partner footprints.

Our CONVICTION & WAGER on this Market:

🟠 LOW CONVICTION While physical material reclamation remains a regulatory necessity, the capital-intensive nature of regional physical yards prevents venture-class returns. Our wager is that localized retail collection remains locked in a high-overhead, low-margin arbitrage cycle that cannot scale without exponential physical footprint expenditure. During a discovery call, a single metric showing customer acquisition cost payback exceeding 18 months for a newly established regional physical yard would immediately invalidate the space.

This score highlights that the regional scrap reclamation market is flat, slow-growing, and structurally limited by localized transport realities.

- Market Size30/100× 25%The immediate target market represents a narrow sliver of the broader regional reclamation sector, serving local tri-state contractors rather than large industrial players.

- Growth Drivers40/100× 25%Driven by moderate regulatory updates and landfill diversion policies, but limited by slow retail volume growth.

- Timing Why Now45/100× 25%Enabled by the increasing consumer awareness of e-waste recycling and the ubiquity of regional retail-facing automated collection systems.

- Market Risks25/100× 25%Exposed to severe commodity downcycles, rising real estate costs, and strict local environmental permitting requirements.

Winning this market is a physical race-to-the-bottom that offers little defensibility against capital-rich legacy operators.

- Incumbents30/100× 25%Dominated by massive multi-billion-dollar local waste management systems with long-standing municipal relationships and huge logistics fleets.

- Challengers40/100× 25%Emerging regional tech aggregators who leverage basic software tools but still require substantial physical yard footprint expansion.

- White Space30/100× 25%Traditional micro-contractor channels remain underserved by legacy scrap buyers who prioritize bulk industrial accounts.

- Defensibility20/100× 25%Zero switching costs or technology-driven moats, as sellers routinely shop around to secure different pennies-on-the-pound rates.

The high overhead GTM taxes make self-sustaining, efficient unit economics difficult to achieve.

- GTM Model45/100× 25%Heavy reliance on local offline trade channels, direct physical flyers, and local search optimization with zero viral software loop potential.

- Pricing Model40/100× 25%Operates under strict transactional pay-per-weight pricing with absolute commodity market spot exposure.

- Unit Economics35/100× 25%Narrow gross margins dictated by regional smelter rates, resulting in long payback periods and high capital cash drag.

- Scalability40/100× 25%Scaling requires capital-intensive expansions into new yards, with no structural efficiency gains as volume pools increase.

The exit environment indicates low interest from traditional venture buyers, showing compressed outcomes.

- Funding Activity25/100× 25%Investment remains limited to niche local circular funds, with top-tier VCs almost completely avoiding localized waste roll-up business sheets.

- Exit Multiples15/100× 25%Industry exit multiples are severely compressed, resembling thin physical infrastructure values rather than tech valuations.

- Strategic Buyers25/100× 25%Primarily limited to legacy waste management conglomerates and private equity physical scrap consolidators looking for low-multiple yard bolt-ons.

- Return Profile15/100× 25%

CROSS-SECTION SYNTHESIS

The combination of low market attractiveness and low winnability presents a clear structural trap, indicating that any team targeting this space must deploy a purely software-driven network model rather than scaling a capital-heavy regional yard footprint.

DATA CONFIDENCE

Market opportunity sizing and transactional competitor pricing structures are well documented, but private local yard balance sheets are missing, covering a total of 3 sourced URLs.

Company Deep Dive

Value Proposition

Value Proposition

J.R.'s Advanced Recyclers offers cash payments for old, outdated, or unused metal through a hassle-free scrap recycling process. They provide regional scrap metal and consumer electronics reclamation with immediate cash payouts. The company collects leftover metal pieces and broken electronics from local sources, processes them, sorts the materials, and supplies them to large-scale factories for industrial remanufacturing.

Ideal Customer Profile (ICP)

Local residents, mechanics, construction contractors, and computer enthusiasts with scrap metal or electronics.

B2B or B2C

Hybrid model handling both individual consumer scrap (B2C) and bulky commercial or industrial scrap steel (B2B).

Industry

Metal Recycling and Waste Management, specializing in regional material reclamation and upcycling.

Contact & Legal

Entity Name: J.R.'s Advanced Recyclers. Website: jrsadvancedrecyclers.com. Location: Minnesota region. CEO Profile: in.linkedin.com.

Key Client Examples & Testimonials

Data not available in source.

Product

Core Solution

Scrap metal purchasing and recycling for ferrous and non-ferrous materials, including comprehensive e-waste handling.

Feature Encyclopedia

Ferrous Metal Recycling, Non-Ferrous Metal Recycling, E-Waste Processing, Daily Price Updates, On-site ATM Payments, and Custom Quoting services.

Technical Capabilities

Services include commercial vehicle processing, e-waste component classification, precise ferrous versus non-ferrous separation, and the provision of a mobile-friendly price list.

Use Cases

Recycling old auto parts like rims and rotors, scrapping home construction siding, disposing of end-of-life computer electronics and CPUs, and processing industrial-grade steel and copper transformers.

Business Model

Business Model Analysis

A pay-per-weight procurement model focused on purchasing materials directly from the public.

Revenue Streams & Pricing Tiers

Aluminum: $0.25-$1.00/lb; Brass: $1.00-$4.30/lb; Copper: $0.40-$5.10/lb; Steel: $120.00-$240.00/ton; E-Waste: Up to $29.00/lb for Ceramic Pentium chips.

Plan Features

Non-Ferrous materials are compensated by the pound, while Ferrous materials are compensated by the ton. Specialized items like catalytic converters require proof of title and registration.

Hidden Costs & Terms

ATM fees apply to transactions: $0 fee for $0-$20; $1 fee for $20.01-$50; $2 fee for $50.01 and above.

Team

Company Culture

Customer-centric approach focused on transparency, daily-updated market pricing, and efficient ATM-based financial operations.

Team Analysis

Lead leadership includes Awais Khan (CEO). Website management is overseen by an administrative content team.

Estimated Headcount

Product & Engineering: 1; Marketing: 1; Sales: 5-10; Support & IT: 2; General & Admin (G&A): 2.

CEO

Résumé de l'entreprise

- Climate & Energy Tech > Regional Material Reclamation & Upcycling

- B2B > Transactional

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : Jrsrecycling is a Regional Material Reclamation & Upcycling yard that enables local residents, contractors, and mechanics to liquidate scrap metal and outdated electronics by providing a simplified, physical drop-off point paired with instant cash payments.

⚠️ The PROBLEM : Independent contractors and local tradespeople are stuck driving long distances to complex, intimating industrial scrap yards where they face opaque pricing, slow processing, and delayed payments for low-volume salvage materials.

✅ The SOLUTION : The business leverages a localized retail footprint with transparent daily updated pricing and automated on-site ATM payout terminals to make the reclamation transaction instantaneous and frictionless for the individual seller.

🚀 The GTM : The primary GTM motion relies on physical outbound positioning and local trade partner acquisition targeting mechanics, roofers, and plumbers in the immediate Minnesota tri-state area who generate systematic physical waste but lack built-in industrial waste contracts.- Founder-Market Fit15/100× 15%The listed CEO profile points to Awais Khan based in Mumbai, India, presenting no logical geographical or operational alignment with a localized retail scrapyard in rural Minnesota.

- Track Record10/100× 10%No documented history of scaling venture-class platforms, executing tech-enabled exits, or securing top-tier institutional funding.

- Leadership15/100× 15%The team consists of basic yard operations staff and a single website administrator, completely lacking venture scaling or industrial systems engineering competence.

- Completeness15/100× 15%Severe leadership structural vaccum with no localized executive presence, leaving the asset-heavy model vulnerable to severe operational oversight issues.

- Size & Growth30/100× 30%The addressable market is structurally constrained to localized, tech-enabled scrap metal and e-waste reclamation, processing, and distribution services for independent contractors and retail sellers in the Minnesota tri-state area, offering no path to a massive venture scale TAM.

- Timing Why Now45/100× 45%Macro pressure surrounding local environmental rules and minor e-waste landfill bans create moderate baseline momentum, but are insufficient to force massive retail adoption.

- Competition30/100× 30%High competitive density from legacy physical scrapyards and established municipal waste operators who command superior local relationships and capital reserves.

- Expansion20/100× 20%Regional expansion is incredibly capital intensive, requiring physical footprint replication with zero evidence of digital-first scaling lanes.

- Differentiation10/100× 10%Core offerings are entirely commoditized scrap collection services lacking specialized sortation technology, sorting software, or custom pricing algorithms.

- Product-Market Fit20/100× 20%Serves local retail transactions effectively but achieves zero platform lock-in, long-term contractual reliance, or API-driven customer integration.

- Scalability10/100× 10%Growth is hard-linked 1-to-1 with capital expenditure in land, heavy machinery, and local crew hires, yielding no network effects or software margins.

- IP & Barriers10/100× 10%Completely devoid of patents, proprietary processing trade secrets, or high-barrier structural defensibility.

- Unit Economics25/100× 25%Thin arbitrage margins squeezed between the spot price paid to local retail walk-ins and the off-take rate secured from wholesale industrial buyers.

- Revenue Model20/100× 20%Entirely transactional revenue stream without contract stability, recurring SaaS layers, or predictable volumes.

- Monetization30/100× 30%Base monetization through raw material pricing arbitrage with minor physical upselling charges via customized quoting and ATM fee collections.

- Capital Efficiency20/100× 20%Low capital efficiency based on constant physical working capital needs, cash-advance float for payouts, and rapid hardware wear-and-tear.

- Revenue Growth15/100× 15%Lacks any public financial track record or documented growth trajectory, hinting at flat, legacy performance levels.

- Customer Validation20/100× 20%Limited to transactional walk-in validation, completely missing major regional industrial enterprise logos or long-term structural accounts.

- KPI Progression10/100× 10%Stagnant hiring momentum, flat LinkedIn operational footprint, and minimal software feature rollouts over multiple periods.

- Market Penetration15/100× 15%Pent-up and contained directly to rural Minnesota operations with zero validated outreach into broader US or interstate industrial sectors.

🔍 RISK TO UNDERWRITE :

The central assumption keeping this business alive is that a small regional scrapyard can consistently generate arbitrage margins while offering on-the-spot cash collections and managing physical-intensive operations, which fails entirely if local collection volumes drop below operating overhead or if global commodity scrap prices undergo a prolonged correction. This risk is structurally unresolvable from the outside, as localized physical volume caps and industrial real estate requirements cannot be mitigated using digital software layers.

KEY COMPETITIVE ADVANTAGES

- Instant cash payouts via on-site custom ATM terminals that capture cash-hungry independent tradespeople and local sellers looking for immediate liquidity.

- Low-barrier retail accessibility that captures low-volume consumer e-waste and scrap metal that massive industrial recyclers refuse to service due to handling costs.

- Specialized e-waste intake handling featuring manual component classifications that catch small margins missing in macro scrap streams.

🧱 MOAT : WEAK

The business lacks a true structural moat because it relies on local proximity and physical retail convenience, meaning competitive defensibility drops to zero the moment a regional competitor opens a yard nearby or outbids them on base metal pricing by a few cents per pound. There is no compounding digital feedback loop, since accumulating more local retail transactions does not lower operational processing costs or create structural customer lock-in. A secondary layer of defensibility is entirely absent, exposing the company directly to volatile commodity price swings and standard industrial real estate permitting pressures.

ASYMMETRIC WAGER

- The Bull Case: Jrsrecycling successfully sets up a highly localized, hub-and-spoke automated collection micro-kiosk network across the state, utilizing automated pricing nodes to capture high-margin materials before they reach legacy regional processors, eventually becoming a prime roll-up target for a larger consolidator.

- The Bear Case: The stark mismatch between the Indian administrative profile and the physical yard in Minnesota points to an unorganized asset mix, leading to operational stagnation, margin squeezing from large local competitors, and eventual wind-down.

🚩 RED FLAGS

- Universal Risks: Opaque corporate structure, high real-world cash operational dependency, and direct vulnerability to sudden global commodity market swings without hedging infrastructure.

- Thesis-Specific Mismatches: The business model functions as a brick-and-mortar salvage scrap operation, completely violating the mandate for scalable clean-tech software, deep-tech biological recycling processes, or high-margin circular platforms.

📝 FIRST MEETING PREP KIT

While this company operates in the broad circular economy space, its low-tech, brick-and-mortar profile is a complete mismatch for our venture mandate; our core goal in a discovery call is to quickly confirm the absence of scalable soft/hard-tech and verify the apparent offshore administrative anomalies.

- The Investment Angle: No viable venture investment angle exists, as the model offers no technological pathway to scale or venture-class return multipliers.

- Killer Questions for First Call :

- Question 2 — THE CORE ASSUMPTION : Given your dependency on on-site ATM cash payouts, what is your net yield per processed ton after accounting for physical cash float costs, localized asset overhead, and ATM bank fees?

- Question 3 — UNIT ECONOMICS STRESS TEST : What percentage of your monthly volume is locked into enterprise commercial off-take contracts versus unhedged spot-market arbitrage transactions?

- First Meeting Go/No-Go Signal : We would advance to deeper diligence only if the company demonstrates a proprietary software engine driving automated regional collection networks under licensing models; we will issue a firm pass the moment they confirm this is a traditional, single-location physical scrapyard with no scalable tech layer.

🌐 DATA CONFIDENCE : LOW

- Diligence must focus heavily on clarifying the corporate registry, legal asset ownership, and the physical location's exact historical balance sheet, which are entirely opaque in public data.

- DATA GAPS : Actual annual revenue • Legal entity connection between US and Indian registrations • Historical volume processed by metal category • Real-world employee count on-site.

SWOT Analysis

Strengths

- Immediate ATM payouts reduce customer friction in scrap sales compared to delayed check or bank transfers.

- Daily updated pricing across aluminum, copper, brass, steel, and e-waste categories gives sellers transparent market signals.

- Hybrid model simultaneously serves individual residents dropping off small loads and contractors delivering bulk steel.

- Capability to separate ferrous from non-ferrous materials and classify e-waste components supports multiple resale streams.

- On-site vehicle processing supports larger commercial volumes without requiring customers to handle disassembly.

Weaknesses

- Estimated headcount of one web maintainer and five to ten operations staff constrains ability to handle volume spikes or geographic expansion.

- Public records provide no verified clients, references, or case studies that larger B2B sellers require before committing bulk scrap.

- ATM fee structure on transactions under $1,000 introduces friction for frequent small sellers who constitute the core B2C traffic.

- No disclosed physical address or operating history reduces trust from contractors who need reliable pickup arrangements.

- Leadership connection to Awais Khan remains unconfirmed beyond a generic LinkedIn profile, leaving operational experience opaque.

Opportunities

- Accelerating electronics turnover among consumers and small businesses increases available high-margin e-waste streams such as ceramic CPUs.

- Rising industrial construction activity generates steady flows of steel siding and structural scrap that fit the company's processing equipment.

- Integration of mobile price lists and custom quoting tools can capture additional contractor traffic currently going to informal haulers.

- Specialized pricing for catalytic converters creates a regulated niche that deters casual competitors lacking title verification processes.

- Local market gaps in Minnesota allow capture of both consumer drop-offs and mechanic shop contracts without immediate national competition.

Threats

- Commodity metal price swings directly compress margins between purchase weights and downstream mill or smelter sales.

- Larger regional recyclers with scale, rail access, and established mill contracts can outbid on volume accounts.

- Evolving e-waste regulations may impose new handling, permitting, or downstream audit costs the current small team cannot absorb.

- Absence of any external funding or credit facility leaves the business exposed to cash-flow gaps during price downturns.

- Name confusion with unrelated Indian and European JRS entities risks diluting local brand recognition and SEO.

Aller plus loin sur Jrsrecycling ?Explore Jrsrecycling further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Generated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co