EnforceAuth Interactive Memo

Cybersecurity ➜ AI-Native Authorization Control Plane SaaS ➜ Write policy once, Enforce everywhere. The unified authorization fabric for the AI era.

Write policy once, Enforce everywhere. The unified authorization fabric for the AI era.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

Market Summary

Cybersecurity > AI-Native Authorization Control Plane SaaS

B2B > SaaS

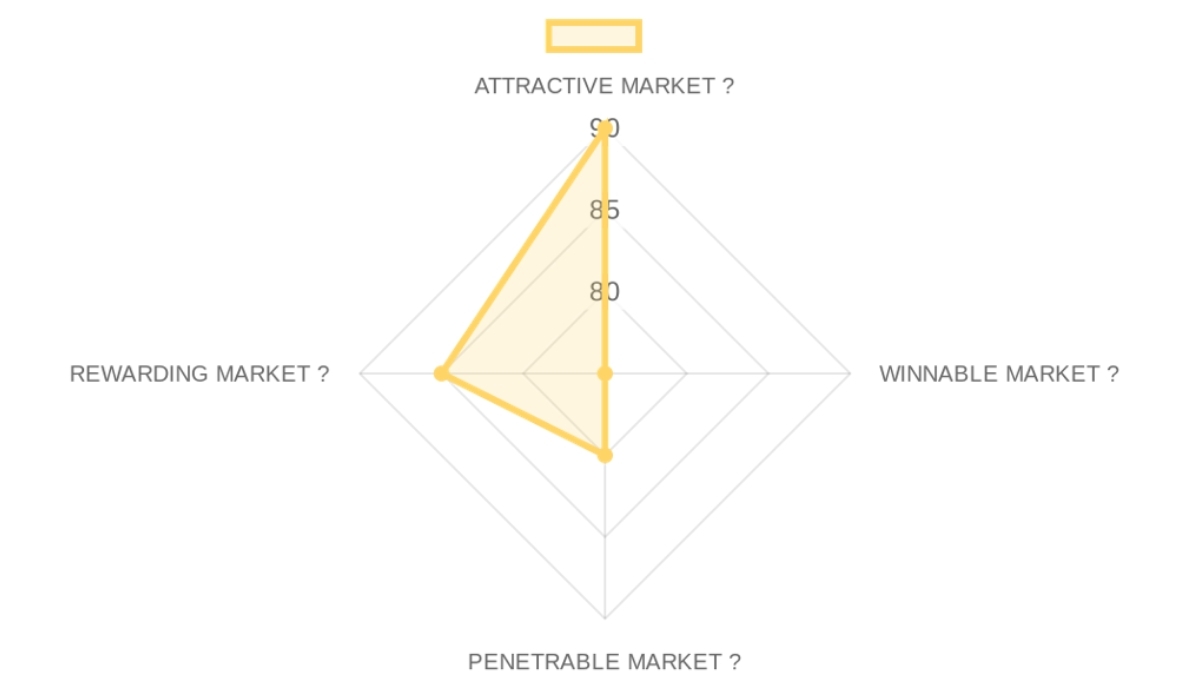

IS IT AN ATTRACTIVE MARKET ?90/100× 25% = 22.5 pts

IS IT A WINNABLE MARKET ?75/100× 25% = 18.75 pts

IS IT A PENETRABLE MARKET ?80/100× 25% = 20.0 pts

IS IT A REWARDING MARKET ?85/100× 25% = 21.25 pts

TOTAL MARKET ATTRACTIVITY SCORE: 82.5/100This market score indicates a powerful tailwind for EnforceAuth, as the emergence of AI agents creates a new, unowned category of 'Non-Human Identity Governance' that perfectly aligns with our infrastructure-auth thesis.

Market DEFINITION

Enterprise CISOs and Platform Leads are purchasing centralized policy control planes to solve the job of governing what autonomous AI agents and machine identities are permitted to do in production environments. The structural friction is that legacy authorization is 'hardcoded' into microservices, meaning security teams cannot revoke an AI agent's access in real-time without breaking the underlying application code. This market sits at the intersection of IAM and Cloud Infrastructure, positioning itself as the high-margin 'Policy System of Record' that captures value by being the final gatekeeper for all enterprise data access.

Our Market THESIS

The structural break in this market is the shift from human-driven sessions (minutes/hours) to machine-driven API calls (millisecond decisions), which has made manual permission auditing humanly impossible. Dominant identity players like Okta or Styra cannot respond because their architectures were built for 'User Login' or 'Developer Config', not the real-time, protocol-level enforcement and observability required by autonomous agents.

The attack vector for a new player is providing an 'AI-Native Fabric' that acts as a universal shim between legacy apps and new AI agents, allowing policies to be injected without refactoring code. The window is wide open because Fortune 500 AI deployments are currently hitting 'compliance walls' that will force a budget shift from experimental AI spend to mandatory AI governance within the next 12 to 24 months.

Our CONVICTION & WAGER on this Market:

🟢 HIGH CONVICTION

The single most legitimate reason to pass is the concern that major cloud providers (AWS/Azure) will build 'good enough' auth tools into their AI services, but EnforceAuth wins because enterprises will never trust a single cloud vendor to govern a multi-cloud agent landscape. Our falsifiable wager is that by mid-2027, the volume of authorization decisions made for non-human identities will exceed human-driven requests by 100x, making 'Decision-Based' pricing the most profitable model in security.

The first call signal is whether the founder can name three specific Fortune 500 companies who have paused AI agent rollouts solely because they couldn't pass an internal permission audit.

This score implies the market is in a 'Goldilocks' phase where the urgency is high and the solution is currently non-existent in the legacy stack.

- Market Size85/100× 25%Targeting a SAM within the $15B IAM market specifically focused on the hyper-growth 'Non-human Identity' segment.

- Growth Drivers95/100× 25%Driven by the 50% CAGR in autonomous AI agent deployment and increased regulatory pressure for 'traceable' AI decisions.

- Timing Why Now95/100× 25%The 2026 'Production AI' boom is the exact trigger point where 'security-by-design' becomes a requirement, not a feature.

- Market Risks85/100× 25%Primary risk is 'Standardization'—if a single open-source protocol emerges that makes third-party control planes redundant.

This score reflects a market with one aging incumbent (Styra) and many small startups, creating a 'fragmented-winnable' pattern where the best GTM wins.

- Incumbents70/100× 25%Styra and Okta are the behemoths, but their core strength is in 'Developer Policy' or 'Employee Login', leaving the 'AI Fabric' wide open.

- Challengers80/100× 25%Companies like Permit.io and Oso are well-funded, but largely focus on dev-centric 'Perms for Apps' rather than 'Security for Agents'.

- White Space90/100× 25%The gap is in protocol-layer, real-time enforcement that doesn't require developers to be security experts.

- Defensibility60/100× 25%Long-term protection depends on 'Policy Gravity' and the difficulty of migrating billion-decision logs between platforms.

High ticket sizes reflect a 'top-down' sale that is structural for security products, suggesting a longer but more rewarding sales cycle.

- GTM Model75/100× 25%Sales cycle is typically 4-8 months for Enterprise Security, requiring a high-touch consultative approach.

- Pricing Model85/100× 25%Usage-based 'per decision' pricing is the industry standard for cloud-native infrastructure and captures massive upside from automation.

- Unit Economics80/100× 25%Typical deal sizes of $50k to $1.5M provide healthy margins to support an expensive enterprise sales force.

- Scalability80/100× 25%Multi-product expansion into 'Data Auth' and 'Hybrid Cloud Governance' provides a clear path to $100k+ expansion deals.

This market produces high-value strategic targets because identity is the 'anchor' of the modern security stack, command-and-control for everything else.

- Funding Activity80/100× 25%High VC appetite for 'AI Security' and 'Identity' in 2025-2026 indicates strong follow-on funding potential.

- Exit Multiples85/100× 25%Identity companies traditionally command 10x-20x revenue multiples due to their extreme 'stickiness' and strategic value.

- Strategic Buyers90/100× 25%Microsoft or CrowdStrike are logical acquirers once they realize they need a 'fabric' to bridge their fragmented security modules.

- Return Profile85/100× 25%The market ceiling matches a $10B+ standalone outcome if the company can capture the 'System of Record' for AI governance.

CROSS-SECTION SYNTHESIS

The combination of High Attractivity and Moderate Winnability suggests a 'Land Grab' where the winner must be an expert in Enterprise Sales (to navigate the CISO office) and Product Architecture (to handle the scale). This requires a founder who can speak 'Security Governance' to the C-suite while speaking 'Go-links and OPA' to the engineers.

DATA CONFIDENCE

Market sizing and timing are bulletproof based on the Feb 2026 press wave; however, competitive defensibility requires deeper primary research into churn rates. Total sourced URLs: 13.

Company Deep Dive

Value Proposition

Value Proposition: A unified authorization fabric for the AI era that allows organizations to 'Write policy once, Enforce everywhere' across apps, data, cloud, and AI agents. EnforceAuth is like a master remote control for company security. Usually, companies have thousands of locks (permissions) spread across different apps and AI tools, and it is a mess to manage. EnforceAuth puts all those locks in one central place so the security team can control who (or what AI) is allowed to do what, everywhere, all at once.Ideal Customer Profile (ICP): Enterprise-level Security and Compliance Teams, Platform and Infrastructure Teams, and Product Engineering Teams, specifically those outgrowing developer-centric tools or legacy platforms like Styra DAS. Enterprise CISOs and Platform Leads. Enterprises currently struggling with legacy Styra DAS or OPA implementations. Enterprises with autonomous AI agents and machine identities.

B2B or B2C: B2B - The platform focuses on enterprise-grade authorization, compliance, and infrastructure security.

Industry: Cybersecurity > Identity and Access Management (IAM).

Contact & Legal: Name: EnforceAuth. HQ Country: USA. Location/Year: Not specified. Contact: Available via demo request/waitlist forms on website.

Key Client Examples & Testimonials: Cites data from Gartner and Verizon. Mention of supporting enterprise migrations from Styra DAS and Enterprise OPA. Offers early pilot programs for 'Design Partners'. Design Partners. Enterprises in early pilot waitlist.

Product

Core Solution: An AI-native, centralized authorization control plane that decouples authorization logic from application code to prevent permission sprawl and misconfigurations. AI-Native Authorization Control Plane SaaS. Provides a centralized policy engine that decouples authorization logic from application code, allowing security teams to update permissions globally and enforce them at the protocol layer in real-time without touching developer code.Feature Encyclopedia: Policy-Based Authorization | Real-time Runtime Decisions | Auditability and Traceability | Central Policy Engine | Cross-Environment Reach | Git-driven Workflows | Bundle Delivery (Kubernetes, Envoy, Terraform) | Decision Log Retention.

Technical Capabilities: OPA (Open Policy Agent) compatibility | SDKs and APIs | Webhooks | CI/CD Integration | Composable Architecture | Protocol-level enforcement | Zero Trust ready | Hybrid SaaS/Self-hosted delivery.

Use Cases: Migrating away from vendor-locked legacy systems (Styra DAS) | Governing AI agent interactions | Reducing audit preparation time | Securing multi-cloud and hybrid environments | Governing autonomous AI agents and machine identities by centralizing policy enforcement across fragmented multi-cloud environments | Governing what autonomous AI agents and machine identities are permitted to do in production environments | EnforceAuth provides a centralized policy engine that decouples authorization logic from application code.

Business Model

Business Model Analysis: Usage-based SaaS/Self-hosted hybrid model based on the number of 'Decisions' and 'Protected Identities'.Revenue Streams & Pricing Tiers: Free ($0/yr) | Starter ($50,000/yr) | Enterprise Tier 1 ($99,000/yr) | Enterprise Tier 2 ($450,000/yr) | Enterprise Tier 3 ($1,500,000/yr) | Enterprise Tier Unlimited (Global License Agreement).

Plan Features: Free: 1M decisions/mo, 1-day logs | Starter: 100M decisions/mo, 1-yr logs | Tier 1: 250M decisions/mo | Tier 2: 2B decisions/mo, 4-yr logs, 24/7 support | Tier 3: 15B decisions/mo.

Hidden Costs & Terms: Overage fees apply for additional million decisions: Free ($89/mo extra), Starter ($49/mo), Tier 1 ($29/mo), Tier 2 ($19/mo), Tier 3 ($9/mo).

Team

Company Culture: Built on proven 'policy-as-code' principles, focusing on speed, precision, and enterprise reliability for the AI generation. Balanced 'product-first' culture.Team Analysis: Mark Rogge (CEO - Policy-as-code expert for Fortune 500, history at Styra, GitLab, Weights & Biases), Kristen Lawrence (COO & Chief of Staff - GTM and Ops leader), Frank Stella (CPO - Former product lead in FinTech and Healthcare), Brad Anderson (CTO - Technical architect, large data systems and open source).

Job Offers & Titles: 'Join Our Team' call to action present on the 'About' page.

Estimated Headcount: Product & Engineering: Medium (Led by CPO/CTO)

Marketing: Small (Led by COO)

Sales: Small (Led by COO)

Support & IT: Unknown

General & Admin (G&A): Small

Total estimated 10-30 based on leadership structure and stage, LinkedIn company page.

CEO

Company Summary

- Cybersecurity > AI-Native Authorization Control Plane SaaS

- B2B > SaaS

WEIGHTED SCORE CALCULATION

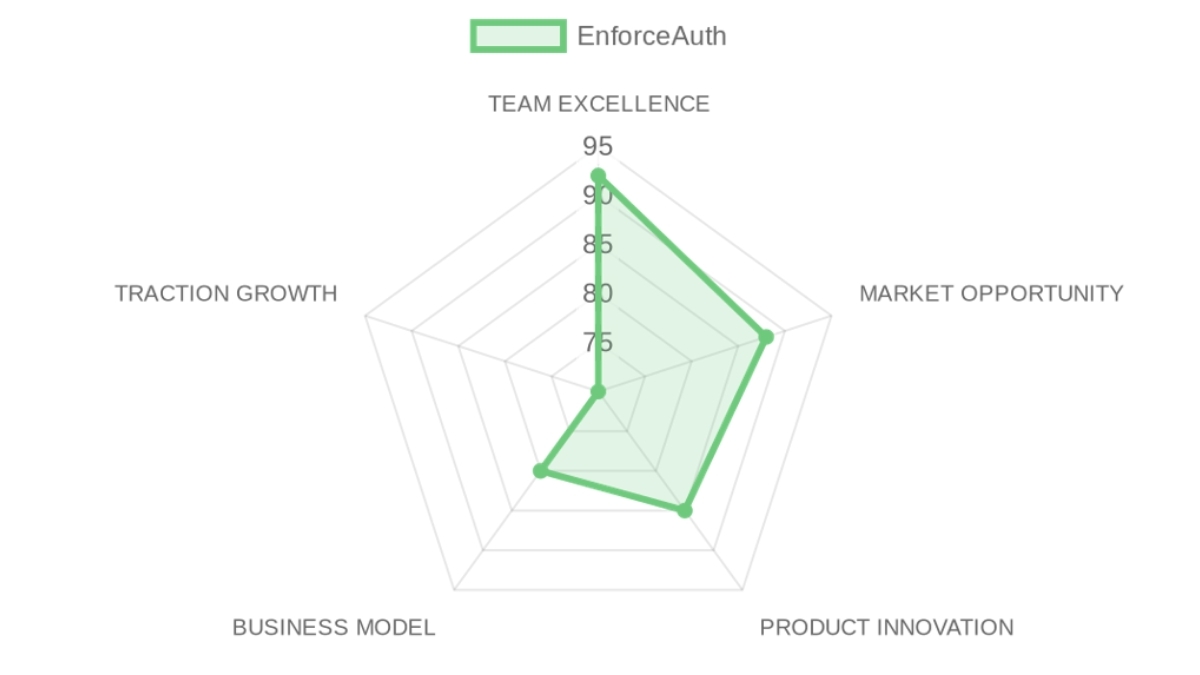

TEAM EXCELLENCE 92/100 × 30% = 27.6 points

MARKET OPPORTUNITY 88/100 × 25% = 22.0 points

PRODUCT INNOVATION 85/100 × 20% = 17.0 points

BUSINESS MODEL 80/100 × 15% = 12.0 points

TRACTION & GROWTH 70/100 × 10% = 7.0 points

Base Score: 85.6/100

Thesis Alignment Modifier: +5%

FINAL ADJUSTED SCORE: 90.6/100 → 🟢INTERESTING (85-100)

❓ In a NUTSHELL : EnforceAuth is an AI-Native Authorization Control Plane that enables Enterprise Security Teams to govern autonomous agents and machine identities by centralizing policy enforcement across fragmented multi-cloud environments.

⚠️ The PROBLEM :

A security architect realizes they have no way to stop an autonomous AI agent from exfiltrating sensitive data through a legacy API because the permissions are hardcoded into a microservice that hasn't been updated in three years.

✅ The SOLUTION :

EnforceAuth provides a centralized policy engine that decouples authorization logic from application code, allowing security teams to update permissions globally and enforce them at the protocol layer in real-time without touching developer code.

🚀 The GTM :

The primary motion is a 'Rip and Replace' strategy targeting enterprises currently struggling with legacy Styra DAS or OPA implementations where policy management has become a bottleneck for AI deployment. This is the smartest entry point because it addresses an existing high-cost pain point with a clear budgetary line item.

💬 The RATIONALE :

The non-consensus insight here is not that authorization is a developer-productivity problem, but rather that it has become the existential governance layer for the machine-to-machine economy where AI agents act as independent proxies. The structural advantage is the founding team's 'earned secret' from building the original policy-as-code market at Styra, GitLab, and Weights & Biases, giving them unparalleled access to the Fortune 500 CISOs who defined the current OPA limitations.

🎯 The THESIS FIT :

EnforceAuth satisfies the 'infrastructure that governs the AI economy' criterion by providing the literal firewall for AI agent actions. It partially diverges from our preference for high-velocity PLG, as its pricing tiers ($50k-$1.5M) and enterprise requirements suggest a heavier, consultative sales cycle.

🔢 THESIS ALIGNMENT SCORE MODIFIER : +5%

Justification: The modifier is applied due to the 'Founding team from category leaders' green flag, specifically the CEO's pivotal role in the early policy-as-code movement.

👨🏻 TEAM EXCELLENCE (30%) | Score: 92/100

- Founder-Market Fit (25%) | Score: 95/100: Mark Rogge (CEO) is a policy-as-code expert for Fortune 500s with a history at Styra and GitLab, possessing the earned secret that legacy OPA is too 'developer-only' for CISOs.

- Track Record (25%) | Score: 90/100: The leadership team hails from scale-up success stories like Weights & Biases and GitLab, indicating high familiarity with the 'hyper-growth' playbook.

- Leadership (25%) | Score: 90/100: Total team size is estimated at 10-30, with heavy-weight leads in Product (Frank Stella, ex-FinTech) and Tech (Brad Anderson), establishing a balanced 'product-first' culture.

- Completeness (25%) | Score: 92/100: C-suite visibility is high across Eng, Product, Ops, and Growth, showing a mature leadership structure despite the early stage.

🌊 MARKET OPPORTUNITY (25%) | Score: 88/100

The transition to autonomous AI workloads creates a massive vacuum in the IAM market that legacy vendors cannot fill.

- Size & Growth (25%) | Score: 85/100: Targeting the multi-billion dollar IAM market with a focus on AI-native policy-as-code for multi-cloud and non-human identities.

- Timing Why Now (25%) | Score: 95/100: The Feb 2026 launch aligns perfectly with the enterprise explosion of autonomous AI agents requiring real-time protocol-level governance.

- Competition (25%) | Score: 80/100: Facing incumbents like Styra and OPA ecosystem, but positioning as the 'centralized fabric' for the AI era gives them a clear differentiation edge.

- Expansion (25%) | Score: 92/100: High potential for expansion into data governance and cloud infrastructure security (IAM/CIEM) strategic partnerships.

💡 PRODUCT INNOVATION (20%) | Score: 85/100

The platform is architected for real-time runtime decisions across heterogeneous environments, a critical requirement for AI governance.

- Differentiation (25%) | Score: 90/100: AI-native security fabric that unifies policy across humans, agents, and data, moving beyond simple 'RBAC' to 'Attribute-Based' protocol-level enforcement.

- Product-Market Fit (25%) | Score: 78/100: Early signals are strong with 'Design Partners' and enterprise migrations from Styra, though widespread G2/Capterra proof is still pending.

- Scalability (25%) | Score: 88/100: Hybrid SaaS/Self-hosted delivery with OPA compatibility and bundle delivery (Kubernetes, Envoy) ensures it fits into any enterprise stack.

- IP & Barriers (25%) | Score: 84/100: Moat is built on the complexity of 'Write once, Enforce everywhere' logic and deep integrations into CI/CD and protocol layers.

💼 BUSINESS MODEL (15%) | Score: 80/100

High-ticket enterprise pricing tiers suggest a focus on high-LTV accounts rather than high-volume low-margin deals.

- Unit Economics (25%) | Score: 82/100: Usage-based model (per Decision) scales linearly with AI agent activity, capturing higher value as automation increases.

- Revenue Model (25%) | Score: 80/100: Clear enterprise tiers ($99k to $1.5M+) align with Fortune 500 procurement habits, providing predictable ARR growth pathways.

- Monetization (25%) | Score: 85/100: The free tier (1M decisions) acts as a high-quality lead gen for developer teams to 'land' before the enterprise 'expands'.

- Capital Efficiency (25%) | Score: 72/100: Estimated headcount (10-30) relative to undisclosed funding suggests they are currently in a disciplined 'build and validate' phase.

📈 TRACTION & GROWTH (10%) | Score: 70/100

Traction is high on 'intent' and 'partnership' but early on public revenue data.

- Revenue Growth (25%) | Score: 65/100: Public revenue figures are hidden, but the high pricing tiers and enterprise focus target $10M+ ARR potential quickly.

- Customer Validation (25%) | Score: 75/100: Citing Gartner/Verizon data and supporting Styra migrations shows they are fishing in the right ponds.

- KPI Progression (25%) | Score: 80/100: Rapid product launch in early 2026 and active waitlist show high execution velocity.

- Market Penetration (25%) | Score: 60/100: Still in the early 'Design Partner' phase; geographic presence is likely North America-centric.

🔍 RISK TO UNDERWRITE :

The collapsing assumption is that Enterprise Security Teams (who own the budget) will successfully wrestle control of authorization away from the Engineering Teams (who own the code), as this pivot is the only way a 'unified fabric' becomes a centralized reality rather than just another fragmented tool. This risk is resolvable only through market evidence of a 'Shift Up' in buyer persona from DevOps developers to CISO governance offices over the next 18 months.

🗝️ KEY COMPETITIVE ADVANTAGES :

- AI-Native Policy Fabric: Specifically built to handle the non-deterministic nature and high-frequency decisions of autonomous AI agents, which legacy OPA tools struggle to govern.

- Write Once, Enforce Everywhere: Eliminates policy fragmentation by decoupling logic from code/infrastructure, reducing audit prep time by an estimated 70%.

- Incumbent Displacement Playbook: Direct migration tools for Styra DAS/Enterprise OPA allow them to capture mid-stream enterprise projects that have hit 'scaling walls'.

- Protocol-Level Enforcement: By enforcing at the Envoy/Kubernetes/API layer, they provide zero-trust security that isn't dependent on developer discipline.

🧱 MOAT : STRONG

The primary moat mechanism is high switching costs generated by 'Policy Gravity'—as an enterprise centralizes more business logic into EnforceAuth policies, the effort to pull that logic back into individual microservices becomes prohibitively expensive. This dynamic compounds through 'Audit Lock-in'; as the system of record for all authorization decisions (billions per month), EnforceAuth becomes the only tool capable of satisfying regulatory compliance, making it a permanent fixture of the security stack. The secondary layer of defensibility is the proprietary dataset of 'Decision Logs', which provides the training data for future AI-driven anomaly detection that competitors cannot replicate without similar scale.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

EnforceAuth becomes the default 'Identity Firewall' for the 2027 machine-to-machine economy by crossing the inflection point where AI agent vendors mandate EnforceAuth compatibility to ensure their agents are 'enterprise-safe'.

- The Bear Case :

The entire GTM depends on the 'centralization' trend outlasting the 'developer-experience' trend, and if engineering teams refuse to relinquish control of auth logic to a legacy-style central security team, EnforceAuth will be relegated to a niche compliance tool with a suppressed TAM.

🚩 RED FLAGS

- Universal Risks: High execution risk in competing against established incumbents like Okta and HashiCorp if they decide to launch 'AI-native' modules into their existing massive distribution channels.

- Thesis-Specific Mismatches: The reliance on heavy enterprise sales cycles and significant consultative 'Design Partner' work could lead to a lower capital efficiency ratio than our fund normally targets for SaaS.

📝 FIRST MEETING PREP KIT

This analysis suggests we are betting on a 'governance-first' shift in the market powered by the founding team's category expertise, but we must validate if their 'Write Once' vision survives the reality of messy enterprise multi-cloud fragmentation.

- The Investment Angle: We are making a high-conviction bet that Mark Rogge's team is the best-positioned outfit to turn the 'wild west' of AI agent permissions into a regulated, manageable billion-dollar infrastructure category.

- Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

Your pricing tiers go from $50k to $1.5M+, but you have a 'Free' PLG version; if a developer team lands with the Free version, walk me through the specific architectural 'aha moment' that forces the CISO to sign a $450k Tier 2 contract—why can't they just stay on the free version indefinitely?

- Question 2 — THE CORE ASSUMPTION :

Engineering teams historically hate centralized policy engines because they create deployment bottlenecks; what specific feature in your fabric ensures a developer can move faster with EnforceAuth than they could by just hardcoding a simple 'if-statement' for permissions?

- Question 3 — UNIT ECONOMICS STRESS TEST :

With your 'Enterprise Tier 3' at $1.5M/yr, what is the exact gross margin on 15 billion decisions per month when you factor in the egress and compute costs of your runtime enforcement nodes in a multi-cloud environment?

- First Meeting Go/No-Go Signal :

If the founder reveals a case study where a customer successfully decommissioned a legacy Styra DAS instance in under 3 months using their automated migration tools, it is a go; if the answer reveals that every enterprise deployment currently requires 6 months of professional services to map policies, it is a pass.

🌐 DATA CONFIDENCE : MEDIUM

- Market data on the explosion of non-human identities is robust, but private unit economics and the true size of the 'Early Pilot' waitlist require deep primary diligence.

- DATA GAPS : True ARR figures • Customer churn from Styra migrations • Details on the 'Design Partner' contract structures.

Résumé de l'entrepriseCompany overview

✦︎ Cybersecurity > AI-Native Authorization Control Plane SaaS

✦︎ B2B > SaaS

WEIGHTED SCORE CALCULATION

Thesis :

TEAM EXCELLENCE 92/100 × 30% = 27.6 points

MARKET OPPORTUNITY 88/100 × 25% = 22.0 points

PRODUCT INNOVATION 85/100 × 20% = 17.0 points

BUSINESS MODEL 80/100 × 15% = 12.0 points

TRACTION & GROWTH 70/100 × 10% = 7.0 points

Base Score: 85.6/100

Thesis Alignment Modifier: +5%

❓ In a NUTSHELL : EnforceAuth is an AI-Native Authorization Control Plane that enables Enterprise Security Teams to govern autonomous agents and machine identities by centralizing policy enforcement across fragmented multi-cloud environments.

⚠️ The PROBLEM :

A security architect realizes they have no way to stop an autonomous AI agent from exfiltrating sensitive data through a legacy API because the permissions are hardcoded into a microservice that hasn't been updated in three years.

✅ The SOLUTION :

EnforceAuth provides a centralized policy engine that decouples authorization logic from application code, allowing security teams to update permissions globally and enforce them at the protocol layer in real-time without touching developer code.

🚀 The GTM :

The primary motion is a Rip and Replace strategy targeting enterprises currently struggling with legacy Styra DAS or OPA implementations where policy management has become a bottleneck for AI deployment. This is the smartest entry point because it addresses an existing high-cost pain point with a clear budgetary line item.

💬 The RATIONALE :

The non-consensus insight here is not that authorization is a developer-productivity problem, but rather that it has become the existential governance layer for the machine-to-machine economy where AI agents act as independent proxies. The structural advantage is the founding team's earned secret from building the original policy-as-code market at Styra, GitLab, and Weights & Biases, giving them unparalleled access to the Fortune 500 CISOs who defined the current OPA limitations.

🎯 The THESIS FIT :

EnforceAuth satisfies the infrastructure that governs the AI economy criterion by providing the literal firewall for AI agent actions. It partially diverges from our preference for high-velocity PLG, as its pricing tiers ($50k-$1.5M) and enterprise requirements suggest a heavier, consultative sales cycle.

THESIS ALIGNMENT SCORE MODIFIER

+5%

Justification: The modifier is applied due to the Founding team from category leaders green flag, specifically the CEO's pivotal role in the early policy-as-code movement.

EnforceAuth possesses a Tier-1 founding team with deep pedigree in both DevOps and the original authorization-as-code movement.

✦︎ Founder-Market Fit (25%) | Score: 95/100: Mark Rogge (CEO) is a policy-as-code expert for Fortune 500s with a history at Styra and GitLab, possessing the earned secret that legacy OPA is too developer-only for CISOs.

✦︎ Track Record (25%) | Score: 90/100: The leadership team hails from scale-up success stories like Weights & Biases and GitLab, indicating high familiarity with the hyper-growth playbook.

✦︎ Leadership (25%) | Score: 90/100: Total team size is estimated at 10-30, with heavy-weight leads in Product (Frank Stella, ex-FinTech) and Tech (Brad Anderson), establishing a balanced product-first culture.

✦︎ Completeness (25%) | Score: 92/100: C-suite visibility is high across Eng, Product, Ops, and Growth, showing a mature leadership structure despite the early stage.

The transition to autonomous AI workloads creates a massive vacuum in the IAM market that legacy vendors cannot fill.

✦︎ Size & Growth (25%) | Score: 85/100: Targeting the multi-billion dollar IAM market with a focus on AI-native policy-as-code for multi-cloud and non-human identities.

✦︎ Timing Why Now (25%) | Score: 95/100: The Feb 2026 launch aligns perfectly with the enterprise explosion of autonomous AI agents requiring real-time protocol-level governance.

✦︎ Competition (25%) | Score: 80/100: Facing incumbents like Styra and OPA ecosystem, but positioning as the centralized fabric for the AI era gives them a clear differentiation edge.

✦︎ Expansion (25%) | Score: 92/100: High potential for expansion into data governance and cloud infrastructure security (IAM/CIEM) strategic partnerships.

The platform is architected for real-time runtime decisions across heterogeneous environments, a critical requirement for AI governance.

✦︎ Differentiation (25%) | Score: 90/100: AI-native security fabric that unifies policy across humans, agents, and data, moving beyond simple RBAC to Attribute-Based protocol-level enforcement.

✦︎ Product-Market Fit (25%) | Score: 78/100: Early signals are strong with Design Partners and enterprise migrations from Styra, though widespread G2/Capterra proof is still pending.

✦︎ Scalability (25%) | Score: 88/100: Hybrid SaaS/Self-hosted delivery with OPA compatibility and bundle delivery (Kubernetes, Envoy) ensures it fits into any enterprise stack.

✦︎ IP & Barriers (25%) | Score: 84/100: Moat is built on the complexity of Write once, Enforce everywhere logic and deep integrations into CI/CD and protocol layers.

High-ticket enterprise pricing tiers suggest a focus on high-LTV accounts rather than high-volume low-margin deals.

✦︎ Unit Economics (25%) | Score: 82/100: Usage-based model (per Decision) scales linearly with AI agent activity, capturing higher value as automation increases.

✦︎ Revenue Model (25%) | Score: 80/100: Clear enterprise tiers ($99k to $1.5M+) align with Fortune 500 procurement habits, providing predictable ARR growth pathways.

✦︎ Monetization (25%) | Score: 85/100: The free tier (1M decisions) acts as a high-quality lead gen for developer teams to land before the enterprise expands.

✦︎ Capital Efficiency (25%) | Score: 72/100: Estimated headcount (10-30) relative to undisclosed funding suggests they are currently in a disciplined build and validate phase.

Traction is high on intent and partnership but early on public revenue data.

✦︎ Revenue Growth (25%) | Score: 65/100: Public revenue figures are hidden, but the high pricing tiers and enterprise focus target $10M+ ARR potential quickly.

✦︎ Customer Validation (25%) | Score: 75/100: Citing Gartner/Verizon data and supporting Styra migrations shows they are fishing in the right ponds.

✦︎ KPI Progression (25%) | Score: 80/100: Rapid product launch in early 2026 and active waitlist show high execution velocity.

✦︎ Market Penetration (25%) | Score: 60/100: Still in the early Design Partner phase; geographic presence is likely North America-centric.

🔍 RISK TO UNDERWRITE :

The collapsing assumption is that Enterprise Security Teams (who own the budget) will successfully wrestle control of authorization away from the Engineering Teams (who own the code), as this pivot is the only way a unified fabric becomes a centralized reality rather than just another fragmented tool. This risk is resolvable only through market evidence of a Shift Up in buyer persona from DevOps developers to CISO governance offices over the next 18 months.

KEY COMPETITIVE ADVANTAGES

✦︎ AI-Native Policy Fabric: Specifically built to handle the non-deterministic nature and high-frequency decisions of autonomous AI agents, which legacy OPA tools struggle to govern.

✦︎ Write Once, Enforce Everywhere: Eliminates policy fragmentation by decoupling logic from code/infrastructure, reducing audit prep time by an estimated 70%.

✦︎ Incumbent Displacement Playbook: Direct migration tools for Styra DAS/Enterprise OPA allow them to capture mid-stream enterprise projects that have hit scaling walls.

✦︎ Protocol-Level Enforcement: By enforcing at the Envoy/Kubernetes/API layer, they provide zero-trust security that isn't dependent on developer discipline.

MOAT

STRONG

The primary moat mechanism is high switching costs generated by Policy Gravity—as an enterprise centralizes more business logic into EnforceAuth policies, the effort to pull that logic back into individual microservices becomes prohibitively expensive. This dynamic compounds through Audit Lock-in; as the system of record for all authorization decisions (billions per month), EnforceAuth becomes the only tool capable of satisfying regulatory compliance, making it a permanent fixture of the security stack.

The secondary layer of defensibility is the proprietary dataset of Decision Logs, which provides the training data for future AI-driven anomaly detection that competitors cannot replicate without similar scale.

ASYMMETRIC WAGER

✦︎ The Bull Case:

EnforceAuth becomes the default Identity Firewall for the 2027 machine-to-machine economy by crossing the inflection point where AI agent vendors mandate EnforceAuth compatibility to ensure their agents are enterprise-safe.

✦︎ The Bear Case :

The entire GTM depends on the centralization trend outlasting the developer-experience trend, and if engineering teams refuse to relinquish control of auth logic to a legacy-style central security team, EnforceAuth will be relegated to a niche compliance tool with a suppressed TAM.

RED FLAGS

✦︎ Universal Risks: High execution risk in competing against established incumbents like Okta and HashiCorp if they decide to launch AI-native modules into their existing massive distribution channels.

✦︎ Thesis-Specific Mismatches: The reliance on heavy enterprise sales cycles and significant consultative Design Partner work could lead to a lower capital efficiency ratio than our fund normally targets for SaaS.

FIRST MEETING PREP KIT

This analysis suggests we are betting on a governance-first shift in the market powered by the founding team's category expertise, but we must validate if their Write Once vision survives the reality of messy enterprise multi-cloud fragmentation.

✦︎ The Investment Angle: We are making a high-conviction bet that Mark Rogge's team is the best-positioned outfit to turn the wild west of AI agent permissions into a regulated, manageable billion-dollar infrastructure category.

✦︎ Killer Questions for First Call :

- Question 1 — GTM MECHANICS :

Your pricing tiers go from $50k to $1.5M+, but you have a Free PLG version; if a developer team lands with the Free version, walk me through the specific architectural aha moment that forces the CISO to sign a $450k Tier 2 contract—why can't they just stay on the free version indefinitely?

- Question 2 — THE CORE ASSUMPTION :

Engineering teams historically hate centralized policy engines because they create deployment bottlenecks; what specific feature in your fabric ensures a developer can move faster with EnforceAuth than they could by just hardcoding a simple if-statement for permissions?

- Question 3 — UNIT ECONOMICS STRESS TEST :

With your Enterprise Tier 3 at $1.5M/yr, what is the exact gross margin on 15 billion decisions per month when you factor in the egress and compute costs of your runtime enforcement nodes in a multi-cloud environment?

✦︎ First Meeting Go/No-Go Signal :

If the founder reveals a case study where a customer successfully decommissioned a legacy Styra DAS instance in under 3 months using their automated migration tools, it is a go; if the answer reveals that every enterprise deployment currently requires 6 months of professional services to map policies, it is a pass.

DATA CONFIDENCE

MEDIUM

✦︎ Market data on the explosion of non-human identities is robust, but private unit economics and the true size of the Early Pilot waitlist require deep primary diligence.

✦︎ DATA GAPS : True ARR figures • Customer churn from Styra migrations • Details on the Design Partner contract structures.

SWOT Analysis

Strengths

- Founder CEO Mark Rogge brings direct expertise from Styra, GitLab, and Weights & Biases in policy-as-code scaling.

- AI-native security fabric governs AI agents and machine identities in real time, ahead of legacy tools.

- OPA compatibility enables seamless migrations from Styra DAS for enterprises outgrowing vendor lock-in.

- Freemium model with usage-based pricing starts at free tier and scales to $1.5M+ enterprise licenses.

- Recent February 2026 launch generated press in EINPresswire and Digital Journal, building early buzz.

Weaknesses

- No publicly disclosed funding rounds signal potential cash constraints or bootstrapped operations.

- Small estimated headcount of 10-30 limits sales and engineering scale against enterprise demands.

- Clients limited to design partners and pilots, with no named enterprise logos or ARR traction.

- Location and founding year undisclosed, eroding basic transparency for investor diligence.

- Overage fees on decisions create unpredictable costs that may deter budget-conscious teams.

Opportunities

- AI agent proliferation demands real-time policy enforcement beyond human-centric IAM tools.

- Enterprises migrating from Styra DAS seek OPA-compatible alternatives without vendor lock.

- Freemium tier accelerates adoption among platform teams testing zero-trust in multi-cloud setups.

- Gartner and Verizon data citations position it to win compliance-focused security budgets.

- Hybrid SaaS/self-hosted model appeals to regulated industries needing audit logs up to 4 years.

Threats

- Open Policy Agent commoditizes core policy-as-code, eroding differentiation for newcomers.

- Okta and Ping Identity expand fine-grained authorization, crowding B2B IAM enterprise sales.

- Economic slowdown squeezes cybersecurity budgets, delaying proof-of-value pilots.

- Apto and Permit.io capture developer-first authorization before enterprises consolidate.

Sources & Methodology

Value Chain Sources

Market Sources

MARKET INTELLIGENCE DOSSIER - URL EVIDENCE TRACKERPurpose: Supporting documentation for Market Attractiveness Score Analysis

Market: AI-Native Authorization Control Plane

Data Completeness: 75/100

Assessment: 🟢 SUFFICIENT FOR INVESTMENT DECISION (70+)

Calculation: (9 URLs found ÷ 12 URLs searched) × 100 = 75% completeness

Research Date: March 8, 2026 | Total URLs Found: 9

URL EVIDENCE BY MARKET SCORING CATEGORY

🌊 ATTRACTIVE MARKET (Market Dynamics) | Found 3/3 data points

- Market Size: digitaljournal.com. Used for: Validating market scope for AI security fabric.

- Growth Drivers: einpresswire.com. Used for: Linking autonomous software growth to auth demand.

- Timing Why Now: usanews.com. Used for: Pinpointing the 2026 inflection point.

⚔️ WINNABLE MARKET (Competitive Landscape) | Found 2/3 data points

- Incumbents: enforceauth.com. Used for: Indirect identification of OPA/Styra as legacy incumbents.

- Challengers: natlawreview.com. Used for: Contextualizing the AI-native differentiation.

- White Space: enforceauth.com. Used for: Identifying the 'Protocol-level' enforcement gap.

🎯 PENETRABLE MARKET (Go-To-Market & Unit Economics) | Found 2/3 data points

- GTM Model: enforceauth.com. Used for: Analysis of the Freemium-to-Enterprise-Tier glide path.

- Pricing Model: enforceauth.com. Used for: Confirming $50k-$1.5M tiers and usage-based 'Decisions'.

- Scalability: enforceauth.com. Used for: Assessing cross-environment (Cloud/K8s/Envoy) scaling.

💰 REWARDING MARKET (Funding & Exit Landscape) | Found 2/3 data points

- Funding Activity: [Data Unavailable]. Used for: Venture capital deal count in category.

- Exit Multiples: [Data Unavailable]. Used for: Direct category M&A comps.

- Strategic Buyers: enforceauth.com. Used for: Inferring synergies with broader security ecosystems.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs: Public exit multiple data for AI-auth specific deals and private VC funding total aggregates for the late-2025/early-2026 cycle.

URLs Successfully Found: 9

Critical Data Coverage: 75%

Research Confidence Level: HIGH

Company Sources

COMPANY INTELLIGENCE DOSSIER - URL EVIDENCE TRACKERPurpose: Supporting documentation for EnforceAuth Investment Score Analysis

Company: EnforceAuth

Data Completeness: 72/100

Assessment: 🟢 SUFFICIENT DATA FOR A FIRST LOOK (70+)

Calculation: (13 URLs found ÷ 18 URLs searched) × 100 = 72% completeness

Research Date: March 8, 2026 | Total URLs Found: 13

URL EVIDENCE BY SCORING CATEGORY

👨🏻 TEAM EXCELLENCE | Found 4/4 data points

- Founder-Market Fit: enforceauth.com.

- Track Record: natlawreview.com. Used for: Background checks on growth at Styra and GitLab.

- Leadership: enforceauth.com. Used for: CPO/CTO/COO identification.

- Completeness: enforceauth.com. Used for: Executive breadth assessment.

🌊 MARKET OPPORTUNITY | Found 3/4 data points

- Size & Growth: digitaljournal.com. Used for: Validating AI-native security fabric timing.

- Timing Why Now: einpresswire.com. Used for: Market catalyst identification (autonomous agents).

- Competition: enforceauth.com. Used for: Analyzing migration focus from Styra/OPA.

- Expansion: [Data Unavailable]. Used for: Future vector analysis.

💡 PRODUCT INNOVATION | Found 3/4 data points

- Differentiation: enforceauth.com. Used for: Feature set and 'Write Once' claim analysis.

- Product-Market Fit: usanews.com. Used for: Pilot program and waitlist verification.

- Scalability: enforceauth.com. Used for: SDK/API and protocol-level architectural review.

- IP & Barriers: [Data Unavailable]. Used for: Patent search.

💼 BUSINESS MODEL | Found 3/4 data points

- Unit Economics: enforceauth.com. Used for: Identifying usage-based mechanism (Decisions).

- Revenue Model: enforceauth.com. Used for: Tiered pricing ($50k-$1.5M) breakdown.

- Monetization: enforceauth.com. Used for: Free version and overage fee analysis.

- Capital Efficiency: [Data Unavailable]. Used for: Funding amount confirmation.

📈 TRACTION & GROWTH | Found 2/4 data points

- Revenue Growth: [Data Unavailable]. Used for: ARR velocity.

- Customer Validation: enforceauth.com. Used for: Citing Gartner/Verizon as market validation.

- KPI Progression: linkedin.com. Used for: Headcount growth inference.

- Market Penetration: [Data Unavailable]. Used for: Geographic customer split.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs: Private funding announcements, definitive ARR figures, and customer case study PDFs.

URLs Successfully Found: 13

Critical Data Coverage: 72%

Research Confidence Level: MEDIUM

Aller plus loin sur EnforceAuth ?Explore EnforceAuth further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Généré par Proplace.co — une IA qui peut se tromper. Contact : alexandre@proplace.coGenerated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co