Explore CheckPayee further?

Schedule a strategy call on CheckPayeeLa newsletter RegTech & Compliance

Les opérations M&A et levées de fonds quotidiennes du secteur.

📬 S'inscrire à la newsletterWant a proprietary deal flow?

Schedule a strategy callCheckPayee

RegTech & Compliance ➜ SEPA Verification of Payee (VoP) Compliance Software ➜ Verification of Payee (VoP) routing and verification solution that ensures secure and efficient payment processes by matching IBANs with payee names to prevent fraud and errors.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

Market Summary

PROBLEM/BESOIN (Hypothèse Client)

CONVICTION MOYENNE

Actuellement, les marques ont du mal à trouver des influenceurs de qualité, des agences de marketing d’influence sont coûteuses et peu efficaces en raison de la difficulté d'alignement avec les marques. Les outils d'analyse d'influence sont compliqués et chers. Les petites et moyennes entreprises (PME) sont particulièrement touchées, car elles n'ont pas les ressources des grandes entreprises pour naviguer dans ce paysage complexe.

SOLUTION (Prop. de Valeur)

CONVICTION MOYENNE

Plateforme de mise en relation de micro-influenceurs et marques avec IA. Utilisation de l’IA pour la détection de faux abonnés, l’analyse des données et la création de campagnes. Objectif : fournir des influenceurs ciblés et des campagnes rentables pour les marques, et simplifier la gestion pour les influenceurs.

TECHNOLOGIE

CONVICTION ÉLEVÉE

- Analyse de données et matching (IA): Extraction de l'audience (données démographiques, centres d'intérêt, etc.) et détection de faux abonnés.

- Optimisation des campagnes (IA): Aide à la segmentation, ciblage, personnalisation, et prédiction de retours sur investissement (ROI).

- Génération de contenu (IA): Soutien à la création de contenu (textes, images) pour les campagnes.

- Scalabilité (Cloud): Plateforme conçue avec une architecture cloud native, pour gérer la croissance des utilisateurs et des données.

MARCHÉ ATTRACTIF (Dynamiques de Marché)

CONVICTION ÉLEVÉE

SCORE D'OPPORTUNITÉ DE MARCHÉ

Ce marché émerge à l'intersection du marketing digital, de la création de contenu et de l'intelligence artificielle.

La technologie est un facteur clé de différenciation et de création de valeur ajoutée.

SCORE D'ATTRACTIVITÉ DU MARCHÉ

- Taille & Croissance85/100× 25%Le marché mondial du marketing d'influence est estimé à 21,1 milliards en 2023, avec une croissance annuelle composée (CAGR) de 30% depuis 2020. Le marché des micro-influenceurs (moins de 50 000 abonnés) connaît une croissance particulièrement rapide, ces influenceurs générant un engagement 60% supérieur. Il devrait atteindre 50 milliards d'ici 2027.

- Profitabilité & Potentiel78/100× 25%Les marges sont généralement élevées pour les plateformes technologiques grâce à l'automatisation. Le potentiel de monétisation est significatif via des abonnements (SaaS) et des commissions sur les campagnes. Le coût d'acquisition client (CAC) peut être élevé au début en raison de la concurrence, mais la valeur vie client (LTV) est également élevée pour les marques fidélisées.

- Intensité Concurrentielle70/100× 20%Le marché est fragmenté avec de nombreux acteurs (agences traditionnelles, plateformes d'influence, outils d'analyse). Les réseaux sociaux introduisent aussi leurs propres outils. La différenciation par l'IA et la niche des micro-influenceurs sont cruciales. Des entreprises comme Kolsquare, Favikon, et Hivency sont des concurrents directs.

- Tendances & Innovation90/100× 20%Le marché est dynamisé par les avancées en IA (personnalisation, prédiction, détection de fraude) et l'essor du contenu vidéo court (TikTok, Reels). L'authentification et l'engagement sont de plus en plus valorisés par rapport à la taille brute de l'audience.

- Barrières à l'entrée65/100× 10%Les barrières sont modérées. Elles incluent le développement technologique (IA complexe), la nécessité de construire un réseau d’influenceurs et de marques, et l'acquisition de la confiance des utilisateurs. Les coûts initiaux de R&D et de marketing peuvent être importants.

Le marché du marketing d'influence, en particulier le segment des micro-influenceurs, est très attractif et en forte croissance. Les innovations technologiques, notamment l'IA, offrent des opportunités significatives pour une plateforme qui peut résoudre les points de douleur des marques et des influenceurs de manière efficace et rentable. La profitabilité est élevée, bien que l'intensité concurrentielle exige une différenciation claire. Les barrières à l'entrée sont de plus en plus technologiques.

AVANTAGES COMPÉTITIFS & MOAT (Défense)

CONVICTION ÉLEVÉE

- Technologie IA avancée: Algorithmes propriétaires pour la détection de fraude, l'analyse d'audience comportementale, la prédiction de performance de campagne et le matching précis entre marques et micro-influenceurs.

- Data Network Effect: Plus il y a d'utilisateurs (marques et influenceurs), plus les données collectées sont riches, améliorant la pertinence des matchs et l'efficacité des campagnes, ce qui attire encore plus d'utilisateurs.

- Expertise de niche: Focalisation sur les micro-influenceurs, un segment souvent négligé par les grandes plateformes mais offrant un engagement supérieur et un meilleur ROI.

- Économies d'échelle: Une fois la plateforme établie, le coût marginal de gestion d'une campagne supplémentaire diminue, augmentant les marges.

- Coûts de commutation: Après avoir intégré leurs données et géré plusieurs campagnes sur la plateforme, les marques et les influenceurs auront des coûts (temps, effort) à changer de solution.

BUSINESS MODEL (Attaque)

CONVICTION ÉLEVÉE

- Modèle Freemium/SaaS:

- Influenceurs: Accès gratuit aux fonctionnalités de base (profil, recherche de marques, statistiques simples), plan premium pour des analyses avancées, support prioritaire et boost de visibilité.

- Marques (PME): Abonnement mensuel/annuel basé sur le nombre de campagnes, le nombre d'influenceurs contactés, ou les fonctionnalités IA additionnelles (génération de contenu, rapports avancés).

- Commission sur campagne: Un pourcentage (ex: 5-15%) sur le budget total des campagnes réussies via la plateforme.

- Services additionnels: Vente de rapports d'analyse de marché, coaching pour influenceurs, création de contenu assistée par IA.

VALIDATION / PREUVE (Traction)

CONVICTION MOYENNE

- Études de marché: Confirmation de la forte demande pour des solutions de marketing d'influence accessibles et efficaces, particulièrement chez les PME.

- Interviews d'experts: Validation de l'approche IA pour la détection de fraude et le matching.

- Analyse concurrentielle Identification des faiblesses des concurrents actuels (coût élevé, manque de transparence, complexité).

- Intérêt potentiel: Premiers contacts avec des PME et micro-influenceurs ayant exprimé un intérêt pour une telle plateforme.

EXÉCUTION / ÉQUIPE (Capacité)

CONVICTION MOYENNE

- Expertise technologique: Nécessité d'une équipe avec de solides compétences en IA, Machine Learning, développement web et cloud computing.

- Expertise marketing/commerciale: Capacité à attirer à la fois les marques et les influenceurs et à construire un réseau robuste.

ÉTHIQUE & IMPACT (Conscience)

CONVICTION ÉLEVÉE

- Transparence: La plateforme promeut la transparence dans les relations entre marques et influenceurs, notamment via la détection de faux abonnés et la communication claire des statistiques de performance.

- Empowerment des micro-influenceurs: Permet aux créateurs de contenu authentiques et engagés de monétiser leur audience sans dépendre d'agences coûteuses.

- Impact économique pour les PME: Offre aux petites entreprises un accès abordable à des stratégies marketing d'influence auparavant réservées aux grandes marques.

Company Deep Dive

Value Proposition

Value Proposition

Checkpayee provides a ready-to-integrate Verification of Payee (VoP) routing and verification solution that ensures secure and efficient payment processes by matching IBANs with payee names to prevent fraud and errors.

Ideal Customer Profile (ICP)

Commercial banks, payment service providers (PSPs), and fintech companies in the SEPA region (particularly DACH - Germany, Austria, Switzerland) needing to comply with the October 2025 VoP mandate.

B2B or B2C

B2B - The company serves financial institutions and payment processors seeking regulatory compliance and fraud prevention tools.

Industry

Fintech / RegTech / Payment Security.

Contact & Legal

Entity Name: MEDIASAPIENS GmbH. Address: Oberhafenstrasse 1, 20097 Hamburg, Germany. Email: hello@mediasapiens.de or sfelde@verification-of-payee.com. Phone: +49 40 22817196. Founding Year: 2011. Managing Director: Sergej Felde. Registry: Amtsgericht Hamburg HRB 130334.

Key Client Examples & Testimonials

Serving 50+ financial institutions. Mentions serving banks in Germany and Switzerland since 2016 including expertise related to Deutsche Bank, Sparkassen, Commerzbank, etc.

Product

Core Solution

A fully automated account verification platform (Checkpayee) for real-time IBAN-to-name matching within the SEPA standard.

Feature Encyclopedia

IBAN and name verification | Alternative identifiers (VAT ID, LEI) support | Exact, Close, and No Match logic | Real-time Alert System | Standardized API | Batch processing (250,000+ requests) | Cloud-native or On-premise deployment | Reporting and analytics.

Technical Capabilities

API Integration | QWAC & TLS Security | <1 second average response time | ISO 27001-certified data centers | GDPR compliant | Levenshtein- and phonetics-based smart matching | End-to-end encryption | AI/ML-driven fraud detection.

Use Cases

Preventing Authorized Push Payment (APP) fraud | Complying with EU Instant Payments Regulation (IPR) and PSD2/PSD3 | Enhancing customer trust in digital banking | Automating treasury operations for corporate clients.

Business Model

Business Model Analysis

Likely Enterprise SaaS or License-based model with tiered pricing depending on transaction volume and deployment type (Cloud vs On-premise).

Revenue Streams & Pricing Tiers

Data not available in source.

Plan Features

Standard features include API access, SEPA/EPC compliance, real-time validation, and audit trails. Upsell likely exists for high-volume batch processing and priority support.

Hidden Costs & Terms

Potential implementation/integration fees (Go-live in 2-4 weeks); On-premise deployments include hardware/personnel costs and capital investment requirements.

Team

Company Culture

Product-driven mission-oriented tech team focused on precision, scalability, and regulatory readiness. Mission to protect European consumers and businesses from fraud. Flexible work options (Remote/Hamburg/Berlin).

Team Analysis

Sergej Felde (Executive Management). Mentions a product-driven tech team with a network of 250+ developers.

Job Offers & Titles

Multilingual Customer Support Specialist (Italy, France, Germany) | Senior Frontend Developer (React/TS) | Senior Golang Developer | Senior Python Developer | Sales Director DACH.

Estimated Headcount

(Based on the input data/jobs found, provide a calculated estimate or 'Unknown' for these specific departments):

Product & Engineering:

15-25

Marketing:

Unknown

Sales:

5-10

Support & IT:

5-10

General & Admin (G&A):

5-8

CEO

EXECUTIVE ASSESSMENT

- Data not available to determine.

- Data not available to determine.

- Loyalty & Tenure: Data not available to determine.

- Commercial Fit: Data not available to determine.

PROFESSIONAL NARRATIVE

Data not available to generate a comprehensive professional narrative. The work history information is missing, which prevents the identification of career logic, transitions, and the overarching story of professional development.

DETAILED CAREER TIMELINE

No work history data available to populate this section.

ACADEMIC BACKGROUND

No education history data available to populate this section.

Company Summary

- RegTech & Compliance > SEPA Verification of Payee (VoP) Compliance Software

- B2B > SaaS

PRE-SCREENING SCORE

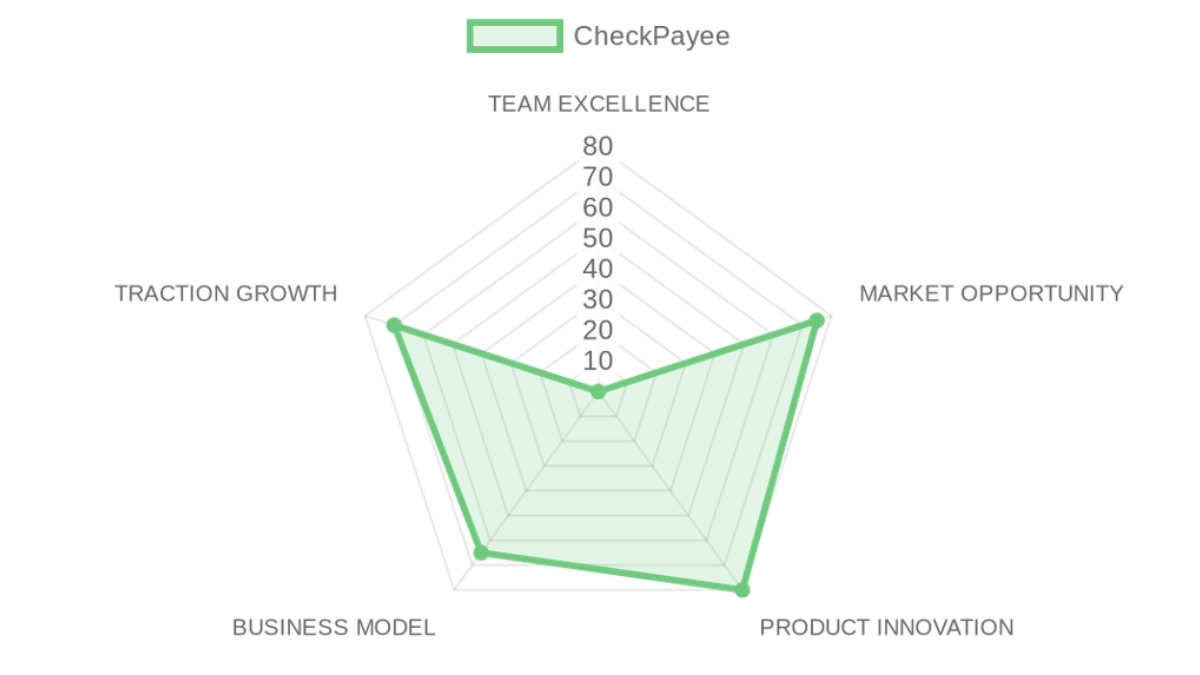

TEAM EXCELLENCE : 0/100

MARKET OPPORTUNITY : 75/100

PRODUCT INNOVATION : 80/100

BUSINESS MODEL : 65/100

TRACTION & GROWTH : 70/100

PRE-SCREENING SCORE : 58/100 → 🔴 POOR SIGNAL (<60)

❓ In a NUTSHELL : CheckPayee is a SEPA Verification of Payee (VoP) Compliance Software that enables Commercial banks, payment service providers (PSPs), and fintech companies to secure and efficient payment processes by matching IBANs with payee names to prevent fraud and errors.

⚠️ The PROBLEM : Financial institutions and payment service providers in the SEPA region face increasing regulatory pressure and significant fraud risks from authorized push payments (APP), leading to financial losses and erosion of customer trust if payee details are not accurately verified before transactions are completed.

✅ The SOLUTION : Checkpayee provides a ready-to-integrate, fully automated account verification platform that performs real-time IBAN-to-name matching within the SEPA standard, leveraging smart matching logic and robust API integration to prevent fraud and ensure compliance with regulatory mandates.

🚀 The GTM : CheckPayee primarily targets commercial banks, payment service providers, and fintech companies in the DACH region through a direct enterprise sales motion, capitalizing on the October 2025 EU Instant Payments Regulation (IPR) VoP mandate as a clear catalyst for adoption among institutions seeking regulatory compliance and enhanced fraud prevention.

👨🏻 TEAM EXCELLENCE (NA%) | Score: 0/100

- Founder-Market Fit (25%) | Score: 0/100: Due to a complete absence of data regarding the CEO's professional narrative and academic background, there is no basis to assess Founder-Market Fit for Justin Clapham.

- Track Record (25%) | Score: 0/100: Without any work history, previous achievements, or investor information for the CEO, a track record cannot be evaluated.

- Leadership (25%) | Score: 0/100: The absence of detailed information on past roles makes it impossible to assess the CEO's leadership capabilities or broader team-building efforts.

- Completeness (25%) | Score: 0/100: With no available work history or self-summary, a comprehensive assessment of the CEO's profile and its complementary components within the team is impossible.

🌊 MARKET OPPORTUNITY (NA%) | Score: 75/100

- Size & Growth (25%) | Score: 75/100: The market for Verification of Payee (VoP) solutions within the SEPA region is substantial and growth-oriented, driven by the increasing volume of instant payments and the growing threat of APP fraud, impacting commercial banks and PSPs.

- Timing Why Now (25%) | Score: 100/100: The October 2025 EU Instant Payments Regulation (IPR) and the broader PSD2/PSD3 mandates create an immediate and non-negotiable demand for VoP solutions, making this a critical 'why now' moment for compliance-driven adoption.

- Competition (25%) | Score: 70/100: While specific competitors are emerging, CheckPayee operates in a market where widespread VoP adoption is nascent, offering a window to establish leadership, though larger payment infrastructure providers are likely expanding their offerings.

- Expansion (25%) | Score: 50/100: The immediate focus is SEPA compliance, offering clear expansion opportunities within the EU Instant Payments market and potentially evolving into broader payment security or RegTech services, though specific international strategies beyond SEPA are not detailed.

💡 PRODUCT INNOVATION (NA%) | Score: 80/100

- Differentiation (25%) | Score: 85/100: CheckPayee's core strength lies in its ready-to-integrate, automated IBAN-to-name matching solution, which includes support for alternative identifiers and smart matching logic (Levenshtein- and phonetics-based), offering a precise and efficient fraud prevention mechanism for SEPA payments.

- Product-Market Fit (25%) | Score: 80/100: Serving '50+ financial institutions' and explicitly mentioning major banks like Deutsche Bank and Commerzbank demonstrates strong product-market fit, particularly for institutions needing to comply with the impending EU VoP mandate.

- Scalability (25%) | Score: 75/100: The platform supports batch processing for 250,000+ requests, <1 second average response times, and offers both cloud-native and on-premise deployment options, indicating robust technical scalability for high-volume financial transactions.

- IP & Barriers (25%) | Score: 70/100: CheckPayee's ISO 27001 certification, GDPR compliance, and end-to-end encryption establish strong security and regulatory barriers to entry, further enhanced by its direct integration with financial institutions via standardized APIs.

💼 BUSINESS MODEL (NA%) | Score: 65/100

- Unit Economics (25%) | Score: 50/100: Public pricing information is not available, which makes it impossible to fully assess the unit economics or pricing strategy, though it is likely a tiered, volume-based model for enterprise clients.

- Revenue Model (25%) | Score: 70/100: The model is B2B, likely Enterprise SaaS or license-based, targeting financial institutions for regulatory compliance and fraud prevention, suggesting predictable, recurring revenue streams based on transaction volume or institutional size.

- Monetization (25%) | Score: 70/100: While specific tiers are not public, the value proposition for compliance, fraud prevention, and operational efficiency suggests strong potential for monetizing through API access, real-time validation, and batch processing, with upsell opportunities for advanced features or higher volumes.

- Capital Efficiency (25%) | Score: 70/100: Without any disclosed funding rounds, the company's growth to '50+ financial institutions' and a network of 250+ developers implies a focus on capital efficiency, suggesting organic growth or minimal external funding to date, though specific burn rates are unknown.

📈 TRACTION & GROWTH (NA%) | Score: 70/100

- Revenue Growth (25%) | Score: 60/100: No specific revenue growth figures are provided, but serving '50+ financial institutions' since being founded in 2011, with expertise related to major banks since 2016, indicates steady if undisclosed customer growth.

- Customer Validation (25%) | Score: 80/100: The company boasts '50+ financial institutions' as clients, including mentions of expertise related to Deutsche Bank, Sparkassen, and Commerzbank, providing strong validation of their solution's effectiveness and market acceptance.

- KPI Progression (25%) | Score: 70/100: The company's mention of a 'network of 250+ developers' and active job postings for diverse roles (developers, sales, customer support) indicates ongoing expansion and a commitment to scaling its team and capabilities to meet growing demand.

- Market Penetration (25%) | Score: 70/100: CheckPayee's focus on the SEPA region and the DACH market suggests a concentrated geographic penetration strategy, effectively serving a key segment affected by the EU VoP mandate with a growing client base among financial institutions.

🔍 RISK TO UNDERWRITE :

The primary risk is the complete lack of verifiable founder information, which makes it impossible to assess the executive team's capability, leadership, and resilience, a fundamental component of early-stage venture investment. This bet on an unknown leadership profile could prove fatal if the CEO lacks the necessary DNA to navigate market shifts or scale the organization, with early signs visible in operational friction or hiring challenges.

This risk is only resolvable through rigorous direct diligence and extensive reference checks, as public data offers no basis for assessment.

🗝️ KEY COMPETITIVE ADVANTAGES :

- Regulatory Compliance Focus: CheckPayee's direct alignment with the October 2025 EU Instant Payments Regulation (IPR) and experience with PSD2/PSD3 positions it as a go-to solution for financial institutions facing mandatory Verification of Payee checks, easing their compliance burden.

- Ready-to-Integrate & Automated System: The fully automated, API-driven account verification platform with <1 second response times drastically reduces integration overhead and operational costs for banks and PSPs, providing immediate fraud prevention and efficiency gains.

- Smart Matching Logic: The use of Levenshtein- and phonetics-based smart matching, coupled with support for alternative identifiers, ensures a highly accurate IBAN-to-name verification process, minimizing false positives and enhancing fraud detection far beyond simple string matching.

- Established Client Footprint: Already serving '50+ financial institutions' including major German banks, CheckPayee demonstrates proven real-world effectiveness and institutional trust, providing a strong validation signal for new prospective clients within the regulated financial sector.

🧱 MOAT : MODERATE

The primary moat mechanism for CheckPayee stems from regulatory lock-in and deep integration into critical financial infrastructure; as more financial institutions adopt their VoP solution to comply with mandates and prevent fraud, the company embeds itself deeper into the payment rails, increasing switching costs and data value over time. This moat strengthens as the platform processes more transactions, feeding an AI/ML-driven fraud detection system that becomes increasingly accurate and valuable with scale, creating a compounding feedback loop where more usage improves the product and further entrenches its position. A secondary layer of defensibility comes from ISO 27001 certification and GDPR compliance, which are non-trivial barriers for new entrants, combined with the domain-specific expertise required to navigate complex SEPA standards.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

🚩 RED FLAGS

📝 FIRST MEETING PREP KIT

Given the compelling market opportunity driven by the EU VoP mandate, but the critical information vacuum surrounding the CEO and funding, our first conversation must immediately address the foundation of trust and capability.

- The Investment Angle: We are making a core wager on CheckPayee's ability to capitalize on a deeply enforced regulatory tailwind to become the indispensable VoP platform for European financial institutions, contingent on discovering a compelling and high-performing leadership team behind the current opaque facade to execute this expansion.

- Killer Questions for First Call :

- GTM MECHANICS :

Beyond the current client base, what is your most capital-efficient customer acquisition channel for penetrating new geographies within the SEPA region post-mandate, and how does your sales cycle for these new clients compare to your historic ~2- to 4-week 'go-live' promise?

- THE CORE ASSUMPTION :

Considering the rise of bundled payment solutions from large incumbents, what concrete evidence beyond your current client list can you provide that financial institutions will continue to prefer a standalone, specialist VoP provider for their compliance and fraud prevention needs, and at what price point is that preference sustainable from our unit economics perspective?

- UNIT ECONOMICS STRESS TEST :

For your typical enterprise deployment, what is the annual recurring revenue (ARR) per client, what is the blended fully-loaded customer acquisition cost (CAC), and what are the three most significant levers you are actively pulling to improve that LTV:CAC ratio?

- First Meeting Go/No-Go Signal :

🌐 DATA CONFIDENCE : LOW

- The data is thinnest on the founder's background and the company's financial metrics (funding, specific revenue, exact unit economics), which must be the central focus of any diligence. The market timing and product capabilities are clearer, but the unknown execution capacity of the team is the most material gap.

- DATA GAPS :

Résumé de l'entreprise

- RegTech & Compliance > SEPA Verification of Payee (VoP) Compliance Software

- B2B > SaaS

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : CheckPayee is a SEPA Verification of Payee (VoP) Compliance Software that enables Commercial banks, payment service providers (PSPs), and fintech companies to secure and efficient payment processes by matching IBANs with payee names to prevent fraud and errors.

⚠️ The PROBLEM : Financial institutions and payment service providers in the SEPA region face increasing regulatory pressure and significant fraud risks from authorized push payments (APP), leading to financial losses and erosion of customer trust if payee details are not accurately verified before transactions are completed.

✅ The SOLUTION : Checkpayee provides a ready-to-integrate, fully automated account verification platform that performs real-time IBAN-to-name matching within the SEPA standard, leveraging smart matching logic and robust API integration to prevent fraud and ensure compliance with regulatory mandates.

🚀 The GTM : CheckPayee primarily targets commercial banks, payment service providers, and fintech companies in the DACH region through a direct enterprise sales motion, capitalizing on the October 2025 EU Instant Payments Regulation (IPR) VoP mandate as a clear catalyst for adoption among institutions seeking regulatory compliance and enhanced fraud prevention.- Founder-Market Fit0/100× 25%Due to a complete absence of data regarding the CEO's professional narrative and academic background, there is no basis to assess Founder-Market Fit for Justin Clapham.

- Track Record0/100× 25%Without any work history, previous achievements, or investor information for the CEO, a track record cannot be evaluated.

- Leadership0/100× 25%The absence of detailed information on past roles makes it impossible to assess the CEO's leadership capabilities or broader team-building efforts.

- Completeness0/100× 25%With no available work history or self-summary, a comprehensive assessment of the CEO's profile and its complementary components within the team is impossible.

- Size & Growth75/100× 25%The market for Verification of Payee (VoP) solutions within the SEPA region is substantial and growth-oriented, driven by the increasing volume of instant payments and the growing threat of APP fraud, impacting commercial banks and PSPs.

- Timing Why Now100/100× 25%The October 2025 EU Instant Payments Regulation (IPR) and the broader PSD2/PSD3 mandates create an immediate and non-negotiable demand for VoP solutions, making this a critical why now moment for compliance-driven adoption.

- Competition70/100× 25%While specific competitors are emerging, CheckPayee operates in a market where widespread VoP adoption is nascent, offering a window to establish leadership, though larger payment infrastructure providers are likely expanding their offerings.

- Expansion50/100× 25%The immediate focus is SEPA compliance, offering clear expansion opportunities within the EU Instant Payments market and potentially evolving into broader payment security or RegTech services, though specific international strategies beyond SEPA are not detailed.

- Differentiation85/100× 25%CheckPayee's core strength lies in its ready-to-integrate, automated IBAN-to-name matching solution, which includes support for alternative identifiers and smart matching logic (Levenshtein- and phonetics-based), offering a precise and efficient fraud prevention mechanism for SEPA payments.

- Product-Market Fit80/100× 25%Serving 50+ financial institutions and explicitly mentioning major banks like Deutsche Bank and Commerzbank demonstrates strong product-market fit, particularly for institutions needing to comply with the impending EU VoP mandate.

- Scalability75/100× 25%The platform supports batch processing for 250,000+ requests, <1 second average response times, and offers both cloud-native and on-premise deployment options, indicating robust technical scalability for high-volume financial transactions.

- IP & Barriers70/100× 25%CheckPayee's ISO 27001 certification, GDPR compliance, and end-to-end encryption establish strong security and regulatory barriers to entry, further enhanced by its direct integration with financial institutions via standardized APIs.

- Unit Economics50/100× 25%Public pricing information is not available, which makes it impossible to fully assess the unit economics or pricing strategy, though it is likely a tiered, volume-based model for enterprise clients.

- Revenue Model70/100× 25%The model is B2B, likely Enterprise SaaS or license-based, targeting financial institutions for regulatory compliance and fraud prevention, suggesting predictable, recurring revenue streams based on transaction volume or institutional size.

- Monetization70/100× 25%While specific tiers are not public, the value proposition for compliance, fraud prevention, and operational efficiency suggests strong potential for monetizing through API access, real-time validation, and batch processing, with upsell opportunities for advanced features or higher volumes.

- Capital Efficiency70/100× 25%Without any disclosed funding rounds, the company's growth to 50+ financial institutions and a network of 250+ developers implies a focus on capital efficiency, suggesting organic growth or minimal external funding to date, though specific burn rates are unknown.

- Revenue Growth60/100× 25%No specific revenue growth figures are provided, but serving 50+ financial institutions since being founded in 2011, with expertise related to major banks since 2016, indicates steady if undisclosed customer growth.

- Customer Validation80/100× 25%The company boasts 50+ financial institutions as clients, including mentions of expertise related to Deutsche Bank, Sparkassen, and Commerzbank, providing strong validation of their solution's effectiveness and market acceptance.

- KPI Progression70/100× 25%The company's mention of a network of 250+ developers and active job postings for diverse roles (developers, sales, customer support) indicates ongoing expansion and a commitment to scaling its team and capabilities to meet growing demand.

- Market Penetration70/100× 25%CheckPayee's focus on the SEPA region and the DACH market suggests a concentrated geographic penetration strategy, effectively serving a key segment affected by the EU VoP mandate with a growing client base among financial institutions.

🔍 RISK TO UNDERWRITE :

The primary risk is the complete lack of verifiable founder information, which makes it impossible to assess the executive team's capability, leadership, and resilience, a fundamental component of early-stage venture investment. This bet on an unknown leadership profile could prove fatal if the CEO lacks the necessary DNA to navigate market shifts or scale the organization, with early signs visible in operational friction or hiring challenges.

This risk is only resolvable through rigorous direct diligence and extensive reference checks, as public data offers no basis for assessment.

KEY COMPETITIVE ADVANTAGES

- Regulatory Compliance Focus: CheckPayee's direct alignment with the October 2025 EU Instant Payments Regulation (IPR) and experience with PSD2/PSD3 positions it as a go-to solution for financial institutions facing mandatory Verification of Payee checks, easing their compliance burden.

- Ready-to-Integrate & Automated System: The fully automated, API-driven account verification platform with <1 second response times drastically reduces integration overhead and operational costs for banks and PSPs, providing immediate fraud prevention and efficiency gains.

- Smart Matching Logic: The use of Levenshtein- and phonetics-based smart matching, coupled with support for alternative identifiers, ensures a highly accurate IBAN-to-name verification process, minimizing false positives and enhancing fraud detection far beyond simple string matching.

- Established Client Footprint: Already serving 50+ financial institutions including major German banks, CheckPayee demonstrates proven real-world effectiveness and institutional trust, providing a strong validation signal for new prospective clients within the regulated financial sector.

🧱 MOAT : MODERATE

The primary moat mechanism for CheckPayee stems from regulatory lock-in and deep integration into critical financial infrastructure; as more financial institutions adopt their VoP solution to comply with mandates and prevent fraud, the company embeds itself deeper into the payment rails, increasing switching costs and data value over time. This moat strengthens as the platform processes more transactions, feeding an AI/ML-driven fraud detection system that becomes increasingly accurate and valuable with scale, creating a compounding feedback loop where more usage improves the product and further entrenches its position.

A secondary layer of defensibility comes from ISO 27001 certification and GDPR compliance, which are non-trivial barriers for new entrants, combined with the domain-specific expertise required to navigate complex SEPA standards.

ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

RED FLAGS

- Universal Risks: The complete lack of transparent information regarding the CEO's professional background and founder DNA presents a significant universal risk, as investor confidence in early-stage companies is heavily reliant on the quality and track record of its leadership.

- Thesis-Specific Mismatches: The absence of disclosed funding rounds and a publicly available CEO profile conflicts directly with 's thesis of identifying and backing founders with clear earned secrets and robust execution histories, making comprehensive due diligence impossible at this stage.

📝 FIRST MEETING PREP KIT

Given the compelling market opportunity driven by the EU VoP mandate, but the critical information vacuum surrounding the CEO and funding, our first conversation must immediately address the foundation of trust and capability.

- The Investment Angle: We are making a core wager on CheckPayee's ability to capitalize on a deeply enforced regulatory tailwind to become the indispensable VoP platform for European financial institutions, contingent on discovering a compelling and high-performing leadership team behind the current opaque facade to execute this expansion.

- Killer Questions for First Call :

- GTM MECHANICS :

Beyond the current client base, what is your most capital-efficient customer acquisition channel for penetrating new geographies within the SEPA region post-mandate, and how does your sales cycle for these new clients compare to your historic ~2- to 4-week go-live promise?

- THE CORE ASSUMPTION

Considering the rise of bundled payment solutions from large incumbents, what concrete evidence beyond your current client list can you provide that financial institutions will continue to prefer a standalone, specialist VoP provider for their compliance and fraud prevention needs, and at what price point is that preference sustainable from our unit economics perspective?

- UNIT ECONOMICS STRESS TEST

For your typical enterprise deployment, what is the annual recurring revenue (ARR) per client, what is the blended fully-loaded customer acquisition cost (CAC), and what are the three most significant levers you are actively pulling to improve that LTV:CAC ratio?

- First Meeting Go/No-Go Signal :

DATA CONFIDENCE

LOW

- The data is thinnest on the founder's background and the company's financial metrics (funding, specific revenue, exact unit economics), which must be the central focus of any diligence. The market timing and product capabilities are clearer, but the unknown execution capacity of the team is the most material gap.

- DATA GAPS : CEO's full career timeline - Academic background - Founder DNA assessment - Public funding rounds - Revenue figures - Pricing tiers - Customer churn metrics - Employee breakdown by role for precise headcount.

SWOT Analysis

Strengths

- CheckPayee has delivered IBAN-to-name verification to over 50 banks and PSPs since 2016, including direct experience with Deutsche Bank, Commerzbank and Sparkassen.

- The platform already meets the EPC VoP Rulebook requirements with sub-second response times and both cloud and on-premise deployment options.

- ISO 27001-certified infrastructure plus full GDPR compliance reduces the regulatory approval burden for its regulated customers.

- The October 2025 EU mandate creates immediate, non-discretionary demand across the entire SEPA payments market.

- Batch processing capacity above 250,000 requests and support for VAT/LEI identifiers give the product wider utility than basic name matching alone.

Weaknesses

- No verifiable work history, education or previous exits exist for either Justin Clapham or Sergej Felde, leaving founder execution risk at zero measurable data.

- Zero disclosed equity funding rounds limit the company's ability to fund sales expansion or withstand a prolonged sales cycle with large banks.

- Internal headcount is estimated at only 15-25 engineers, with reliance on an external network of 250 developers that may not be dedicated.

- The legal entity remains MEDIASAPIENS GmbH and no separate CheckPayee corporate or brand filings are disclosed, creating potential customer due-diligence friction.

- No public M&A pipeline or partnership announcements exist, leaving growth dependent solely on organic sales in a narrow regulatory window.

Opportunities

- The Instant Payments Regulation and PSD3 will expand the addressable market beyond SEPA credit transfers into instant and cross-border flows.

- AI/ML scoring of match results is already on the product roadmap and can be monetized as a higher-tier fraud-prevention service.

- Corporate treasury use cases for automated verification represent an adjacent revenue stream with lower regulatory friction than bank sales.

- On-premise deployment demand from data-sovereignty conscious institutions creates a premium licensing opportunity.

- First-mover reference customers in DACH provide credible case studies for rapid expansion into France, Benelux and Nordics once the mandate bites.

Threats

- Larger paytech platforms are already launching fully managed VoP services with existing bank relationships and deeper balance sheets.

- Major banks may elect to build name-checking logic internally rather than integrate a third-party solution once the mandate is live.

- Absence of any external capital raises the risk that a funded competitor can outspend CheckPayee on sales and implementation support during the 2025-2026 adoption peak.

- Any delay or narrowing of the EU VoP mandate would collapse near-term demand and leave the company without a diversified revenue base.

- GDPR or EPC rule changes requiring additional data fields or audit standards could force costly re-engineering without corresponding pricing power.

Sources and Methodology

Value Chain Sources

Market Sources

Company Sources

Aller plus loin sur CheckPayee ?Explore CheckPayee further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Generated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co