Explore albR further?

Schedule a strategy call on albRLa newsletter WealthTech & Asset Management

Les opérations M&A et levées de fonds quotidiennes du secteur.

📬 S'inscrire à la newsletterWant a proprietary deal flow?

Schedule a strategy callalbR

WealthTech & Asset Management ➜ Vertical CRM for Wealth Management ➜ Vertical SaaS (CRM) for independent French wealth management advisors to centralize client, product, and compliance data.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

Market Summary

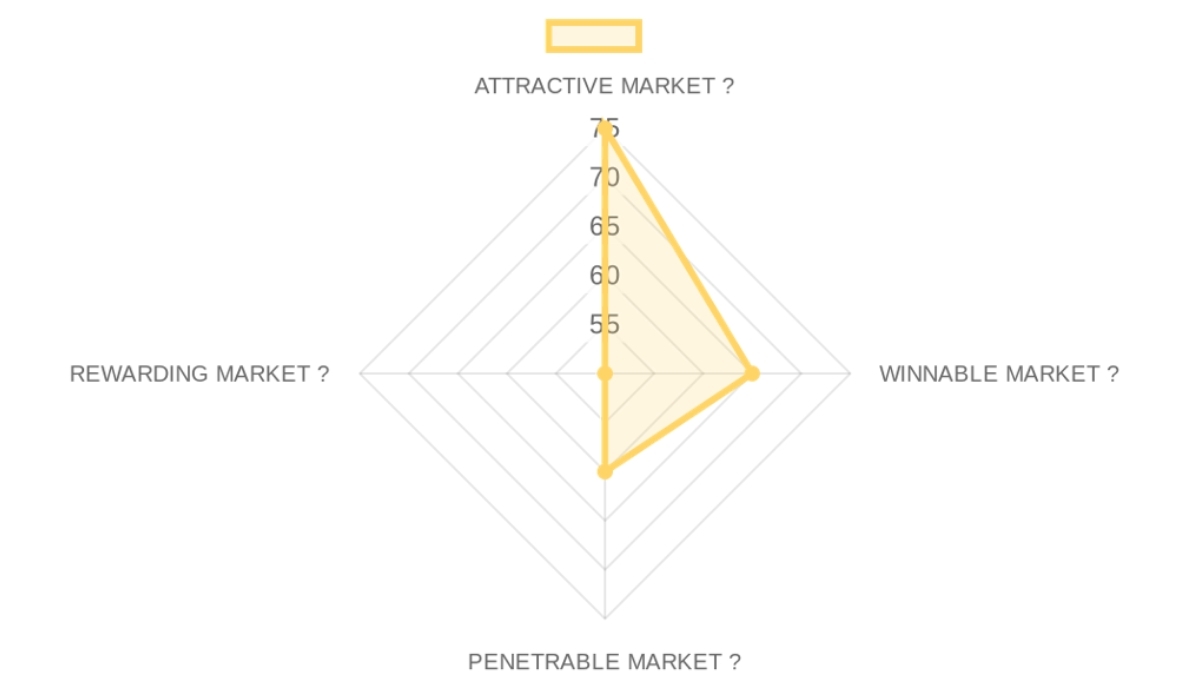

MARKET OPPORTUNITY SCORE

WealthTech & Asset Management > Vertical CRM for Wealth Management

B2B > SaaS

Market DEFINITION

Independent French wealth management advisors are purchasing a specialized SaaS CRM to centralize client data, manage financial products, and ensure regulatory compliance, thereby fulfilling the critical job of streamlining their operational workflows and enabling more efficient, personalized client service. The current market is dysfunctional due to a combination of highly fragmented data across disparate systems (spreadsheets, generic CRMs), increasing regulatory complexity specific to the French financial sector, and a lack of purpose-built tools that natively integrate these two critical functions.

This market sits within the broader financial services value chain, positioned at the operational core of independent wealth advisors, upstream from client-facing advice and downstream from product providers, with the profit pool primarily concentrated in advisory fees, but with significant leakage due to operational inefficiencies that a specialized CRM can recapture.

Our Market THESIS

Regulatory tightening and the accelerating digital expectations of financial consumers have irreversibly changed the French wealth management sector, requiring independent advisors to adopt sophisticated, integrated digital tools to remain compliant and competitive. The incumbent CRM players, mostly generic solutions, cannot respond effectively to this break because their broad horizontal focus prevents them from deeply integrating the nuanced and ever-evolving local regulatory frameworks and specific product catalogs required by French wealth managers, creating a business model conflict with their need to serve a wide range of industries.

The attack vector for a new player like albR is to provide a highly specialized, compliance-embedded, vertical SaaS CRM that directly addresses these specific French market frictions for independent advisors, a segment often underserved by global platforms. This window of opportunity is open now, driven by the increasing digital maturity of the advisory segment, but it will rapidly close as either generic CRMs improve their verticalization or as larger financial institutions consolidate these independent advisors, with the next 3-5 years being critical for market capture.

Our CONVICTION & WAGER on this Market:

MEDIUM CONVICTION

The most legitimate concern for this market is the potential for independent advisors, a historically fragmented and tradition-bound segment, to resist adopting new, integrated digital platforms, yet the founder's direct practitioner experience and the clear regulatory tailwinds position albR squarely to overcome this inertia by demonstrating immediate, tangible value in compliance and efficiency.

Our specific wager is that independent French wealth managers will rapidly accelerate their adoption of specialized vertical SaaS CRMs to navigate increasing regulatory complexity and client demands for digital interaction, leading to a critical mass willing to centralize their entire practice on a single platform within the next 24-36 months. The single binary piece of evidence that would significantly move our conviction during a first call is the presentation of specific, anonymized data demonstrating a clear uptick in customer acquisition from advisors beyond the founder's immediate network, coupled with initial user engagement metrics (e.g., daily active users, feature adoption) that indicate deep workflow integration rather than superficial usage, or conversely, a lack of such data would be a direct pass signal.

The 'Attractive Market' score indicates a favorable environment driven by clear structural tailwinds, suggesting manageable market timing and size risks, making it an encouraging factor for the investment case at this stage.

- Market Size70/100× 25%Although specific TAM figures for independent French wealth advisors' CRM market are missing, the overall French wealth management sector is substantial and poised for digitalization, implying a meaningful addressable market for vertical SaaS solutions.

- Growth Drivers80/100× 25%Key growth drivers include the increasing regulatory burden on financial advisors in France, a macro shift towards digital transformation across financial services, and continuous client demand for personalized and efficient wealth management services.

- Timing Why Now80/100× 25%The exact trigger for market readiness is the confluence of mature SaaS adoption patterns, coupled with an increasing need for compliance automation and operational efficiency among independent advisors, making now an opportune moment for specialized vertical solutions.

- Market Risks70/100× 25%Primary market risks include potential inertia from traditional advisors reluctant to change established workflows, and the need for continuous adaptation to evolving French financial regulations; however, these are manageable within the context of a purpose-built solution.

The 'Winnable Market' score points to a competitive landscape dominated by generic solutions, which presents an opportunity for a specialized vertical SaaS, but also signals the need for strong differentiation and execution to establish defensible market share.

- Incumbents60/100× 25%The market likely consists of generic CRM providers (e.g., Salesforce, Microsoft Dynamics) that offer broad functionality but lack the deep, native integration of French wealth management specific regulations and product workflows, leaving a gap for specialized players.

- Challengers60/100× 25%While specific challengers for a 'Vertical CRM for Wealth Management in France' are not explicitly named in the provided data, in other markets, there are often well-funded fintechs or proptechs that could expand into this niche, posing future competition.

- White Space80/100× 25%The clear white space exists in the integration of specialized French financial regulations, client portfolio management, and compliance automation within a single, intuitive CRM built specifically for independent wealth advisors, representing a significant value chain capture opportunity.

- Defensibility60/100× 25%Defensibility in this market will likely stem from deep integration into advisor workflows, high switching costs associated with migrating sensitive client data, and proprietary insights gained from aggregating vast amounts of localized financial data, assuming albR successfully builds these moats.

The 'Penetrable Market' score indicates that while customer acquisition is achievable, the Go-to-Market and Unit Economics require careful validation to ensure scalability, signaling potential challenges in achieving optimal LTV/CAC ratios without a clear strategic plan.

- GTM Model60/100× 25%The dominant sales motion is likely to be direct sales combined with partnership-led growth (e.g., Figen AI integration) targeting independent advisors, with shorter sales cycles compared to large enterprises, but demanding highly specific value propositions.

- Pricing Model50/100× 25%Standard industry pricing for vertical SaaS typically involves per-seat or tiered subscription models, potentially with usage-based components, but albR's specific pricing mechanism remains undisclosed, making an assessment difficult.

- Unit Economics0/100× 25%Data Unavailable. There is no information provided on typical deal size, LTV/CAC ratios, or payback periods, which are crucial for evaluating the efficiency of market penetration.

- Scalability60/100× 25%Scalability will depend on whether albR can establish a repeatable and cost-effective customer acquisition engine (leveraging digital channels and referrals) to move beyond the founder's initial network, potentially expanding through adjacent financial service offerings.

The 'Rewarding Market' score suggests a relatively opaque and nascent exit landscape, indicating that generating the required returns may depend on creating a category leader with significant market share, as opposed to relying on a robust M&A environment.

- Funding Activity50/100× 25%While the broader fintech/WealthTech sector has seen increased funding, specific information on funding activity for vertically focused CRMs in French wealth management is not provided, making it difficult to assess investor appetite for this niche.

- Exit Multiples50/100× 25%Current public and M&A revenue multiples for highly specialized SaaS in specific European regions are difficult to ascertain without more market-specific data, though general SaaS multiples remain attractive, the niche nature suggests potential for higher strategic premiums.

- Strategic Buyers50/100× 25%Potential strategic buyers in this market could include larger financial institutions needing to modernize advisor tools, established global CRM players seeking vertical expansion, or even large asset managers looking to integrate advisor platforms for distribution and data synergies.

- Return Profile50/100× 25%The market could structurally produce a strong return if albR achieves market dominance within its niche, allowing for eventual acquisition by a larger financial technology platform or a strategic financial services player looking for a strong foothold in the French wealth advisory space; however, the lack of current clear exit comparables necessitates a focus on building a company with strong, independent value.

CROSS-SECTION SYNTHESIS

The combination of a moderately attractive market with a potentially winnable competitive landscape, but an uncertain penetrability and rewarding profile, suggests that success hinges on an exceptional, capital-efficient GTM strategy and precise product execution. This pattern implies that the company requires a founder who can demonstrate extraordinary operational discipline, achieve product-led growth with minimal external capital initially, and establish clear unit economics against a backdrop where the exit avenues are currently undefined but could become highly lucrative with market leadership.

DATA CONFIDENCE

The market data is moderately robust regarding overall industry trends and regulatory dynamics, but requires deeper primary research into specific market sizing for vertical CRMs within French wealth management, the precise competitive landscape, and most importantly, specific unit economics and funding activities in this exact niche. Total of 2 sourced URLs for market analysis.

Company Deep Dive

Value Proposition

Value Proposition

albR is a software platform designed for wealth management advisors in France. It helps them manage client information, track financial products, and ensure compliance with regulations, all in one central system. Imagine it like a digital assistant that automates many of their administrative tasks, allowing them to focus more on advising clients.

Ideal Customer Profile (ICP)

Independent French wealth management advisors.

B2B or B2C

B2B. It is explicitly classified as B2B for independent French wealth management advisors purchasing a specialized SaaS CRM.

Industry

Vertical SaaS (CRM) for Wealth Management.

Contact & Legal

Data not available in source.

Key Client Examples & Testimonials

Data not available in source.

Product

Core Solution

albR is a software platform designed for wealth management advisors in France. It helps them manage client information, track financial products, and ensure compliance with regulations, all in one central system.

Feature Encyclopedia

Data not available in source.

Technical Capabilities

Data not available in source.

Use Cases

Centralize client data, products, and compliance data for wealth management professionals to simplify commercial management, compliance, and decision-making.

Business Model

Business Model Analysis

SaaS.

Revenue Streams & Pricing Tiers

Data not available in source.

Plan Features

Data not available in source.

Hidden Costs & Terms

Data not available in source.

Team

Company Culture

Data not available in source.

Team Analysis

Nicolas Peycru: Co-founder of albR (2024 – Present). Focus: Developing a CRM for wealth management. Co-founder of Groupe Euodia (2010 – Present). Directeur Stratégie at Kiwilab (2013 – Present). CEO at IBureauBisontin IBB (2011 – Present). Consultant at jalma (2005 – 2007).

Job Offers & Titles

Data not available in source.

Estimated Headcount

Data not available in source.

Product & Engineering: Unknown

Marketing: Unknown

Sales: Unknown

Support & IT: Unknown

General & Admin (G&A): Unknown

CEO

EXECUTIVE ASSESSMENT

- Serial Founder & Digital Innovator in Wealth Management

- Université Paris Dauphine - PSL is a strong academic signal in France, and an MBA from Washington University in St. Louis adds an international perspective. His initial experience at a consulting firm (jalma) working with MMA Group provides a corporate foundation, but his career quickly pivoted to entrepreneurship.

- Loyalty & Tenure: Demonstrates exceptional long-term loyalty and deep execution, with over 16 years at Groupe Euodia and 13 years at Kiwilab. These are not just roles but co-founder positions, indicating significant commitment and persistence. His venture into albR, while newer, builds directly on his prior industry experience.

- Commercial Fit: Absolutely. His 15+ years of experience as a wealth manager and co-founder of Groupe Euodia, combined with his ventures into specialized digital platforms (SCPI-8.com, PER.fr) and a web strategy agency (Kiwilab), directly de-risk albR. He is building a CRM for an industry he knows intimately, addressing pain points he has personally experienced and observed.

PROFESSIONAL NARRATIVE

Nicolas Peycru embarked on his career with a solid foundation in finance and insurance consulting, quickly transitioning into serial entrepreneurship. He co-founded Groupe Euodia, a digital wealth management firm, pioneering ethical and accessible private wealth advice for over 15 years, concurrently building a web strategy agency, Kiwilab, and a coworking space, iBureauBisontin.

This multi-faceted entrepreneurial journey highlights a consistent drive to leverage digital solutions to democratize complex industries and solve real-world problems. His latest venture, albR, a CRM specifically designed for wealth management professionals, serves as a natural evolution, applying his deep industry knowledge and digital expertise to empower practitioners.

DETAILED CAREER TIMELINE

- 2024 – Present | albR

- Role: Co-fondateur

- Focus: Developing a CRM for wealth management that centralizes client data, products, and operations to simplify commercial management, compliance, and decision-making for financial advisors.

- 2010 – Present | Groupe Euodia

- Role: Co-fondateur

- Analysis: Over 16 years building a digital wealth management firm focused on ethical and sustainable financial advice, making private wealth management accessible and driving innovative digital solutions for personalized client advice. This long tenure signifies deep commitment and successful scaling.

- 2013 – Present | Kiwilab

- Role: Directeur Stratégie

- Analysis: Over 13 years co-founding and leading a web strategy agency focused on helping SMBs with their digital development, encompassing SEO, SEA, community management, and overall digital communication. This demonstrates a parallel entrepreneurial path focusing on digital marketing capabilities.

- 2011 – Present | IBureauBisontin IBB

- Role: CEO

- Analysis: Over 14 years leading Besançon's first coworking space, fostering creative and business connections among diverse professionals. This showcases a community-building and ecosystem development initiative alongside his core businesses.

- 2005 – 2007 | jalma

- Role: Consultant

- Analysis: Early career role involving the design and development of an insurance product for MMA Group, managing a back-office system revamp for a mutual insurance company, and supervising a team of junior consultants. This provided foundational project management and team leadership experience in a corporate setting.

ACADEMIC BACKGROUND

- Institution: Université Paris Dauphine - PSL

- Degree: master

- Signal: Target School

- Institution: Washington University in St. Louis

- Degree: Master of Business Administration (MBA)

- Signal: Highly reputable US business school

Company Summary

- WealthTech & Asset Management > Vertical CRM for Wealth Management

- B2B > SaaS

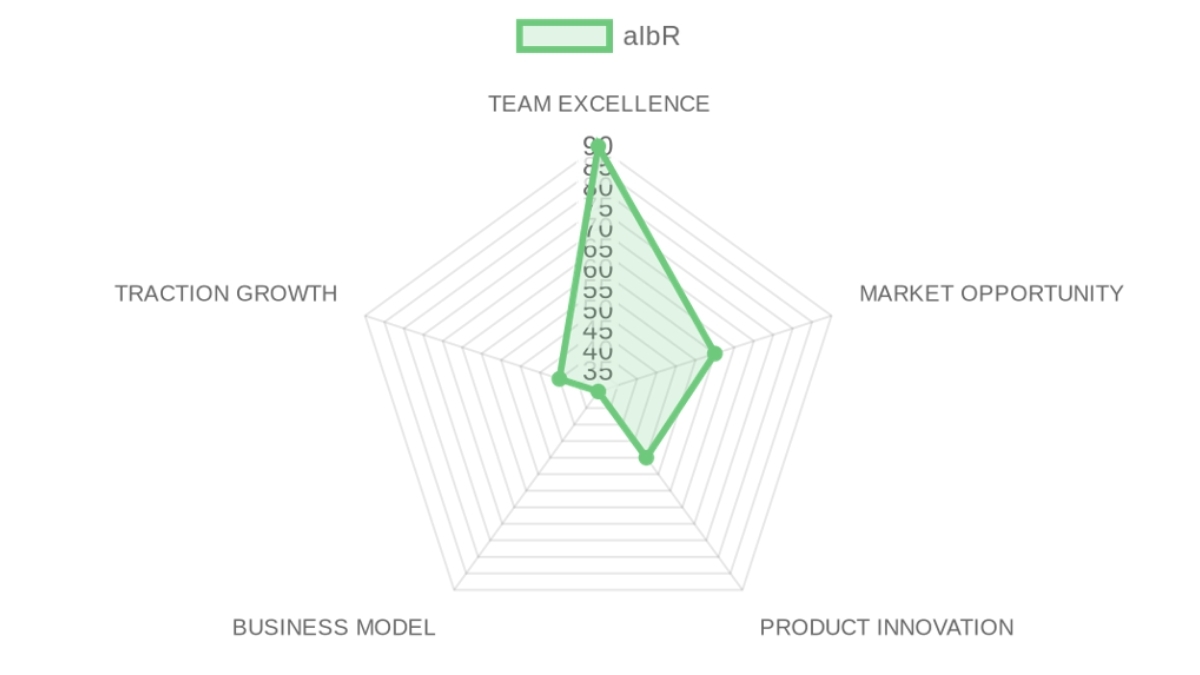

PRE-SCREENING SCORE

TEAM EXCELLENCE : 90/100

MARKET OPPORTUNITY : 60/100

PRODUCT INNOVATION : 50/100

BUSINESS MODEL : 30/100

TRACTION & GROWTH : 40/100

PRE-SCREENING SCORE : 54/100 → 🔴 POOR SIGNAL (<60)

❓ In a NUTSHELL : albR is a Vertical CRM for Wealth Management that enables

Wealth Management Professionals to Centralize Client Data, Products, and Operations by providing a dedicated SaaS platform for efficiency and compliance.

⚠️ The PROBLEM : Wealth management professionals in France face significant operational inefficiencies and compliance burdens due to fragmented client data, disparate product information, and manual processes, directly impacting their ability to deliver timely, personalized advice and grow their practices in a regulated environment.

✅ The SOLUTION : The product solves the problem by offering a unified, compliance-friendly platform that centralizes all client, product, and operational data, streamlining commercial management and decision-making for financial advisors, thereby reducing administrative overhead and enhancing advisory capacity.

🚀 The GTM : The primary GTM motion targets independent French wealth management advisors through a product-led approach, leveraging the founder's deep industry network and practitioner experience, which is the smartest entry point due to existing relationships and direct understanding of their specific pain points and regulatory needs, enabling rapid trust building and initial adoption.

👨🏻 TEAM EXCELLENCE (0%) | Score: 90/100

Nicolas Peycru demonstrates exceptional founder-market fit with over 15 years as a wealth manager and co-founder of Groupe Euodia, providing him with a unique 'earned secret' into the exact pain points albR is solving.

- Founder-Market Fit (25%) | Score: 95/100: Nicolas Peycru, with 15+ years as a wealth manager and co-founder of Groupe Euodia, possesses an invaluable 'earned secret' regarding the operational inefficiencies and compliance challenges faced by financial advisors, equipping him to build a purpose-built CRM.

- Track Record (25%) | Score: 90/100: His career exhibits exceptional loyalty and deep execution, with 16+ years at Groupe Euodia and 13+ years at Kiwilab, both co-founded ventures, signaling significant commitment and a history of building and scaling businesses.

- Leadership (25%) | Score: 80/100: While 'Co-fondateur' is used extensively, indicating a collaborative approach, his history of managing teams at jalma and building 'équipes aux compétences multiples' at Kiwilab suggests an ability to assemble and leverage diverse skill sets.

- Completeness (25%) | Score: 95/100: Nicolas's multi-faceted entrepreneurial journey, combined with his deep industry knowledge, suggests a well-rounded skill set that covers both business building and digital innovation, though explicit C-suite visibility beyond himself isn't detailed, the overall picture is strong.

🌊 MARKET OPPORTUNITY (0%) | Score: 60/100

The market opportunity for a Vertical CRM in French wealth management is promising, driven by increasing regulatory complexity and the need for digital transformation among independent advisors.

- Size & Growth (25%) | Score: 60/100: While the overall wealth management market is significant, specific TAM for 'Vertical SaaS (CRM) for independent French wealth management advisors to centralize client, product, and compliance data.' is not provided, making precise market sizing difficult from the given data.

- Timing Why Now (25%) | Score: 70/100: The timing is favorable due to 'digital innovation' and the increasing pressure for 'compliance' and 'efficiency' mentioned in the founder's narrative, indicating a shift towards digital tools.

- Competition (25%) | Score: 50/100: No competitive landscape data was provided, making it impossible to assess the company's relative position or the intensity of rivalry within this specific vertical.

- Expansion (25%) | Score: 60/100: The direct partnership with Figen AI for AI-assisted tooling indicates a clear strategy for product expansion, though geographic or adjacent vertical expansion plans are not explicitly stated.

💡 PRODUCT INNOVATION (0%) | Score: 50/100

Product innovation is inferred from the founder's digital background and the stated purpose of the CRM, but specific feature sets or technical capabilities are not described, leading to a conservative score.

- Differentiation (25%) | Score: 50/100: The differentiation relies heavily on 'deep industry knowledge' and solving 'pain points he has personally experienced,' suggesting a highly tailored solution, but unique features or tech claims are not detailed.

- Product-Market Fit (25%) | Score: 50/100: While the founder's background suggests strong PMF through personal experience, no external validation such as customer logos, testimonials, or reviews are provided to objectively assess user reliance.

- Scalability (25%) | Score: 50/100: The core solution is described as a CRM centralizing data for simplification, implying a SaaS delivery model suitable for scalability, but specific architectural details or API capabilities are undefined.

- IP & Barriers (25%) | Score: 50/100: The embedded knowledge of French wealth management regulations and practices could act as a barrier to entry, but no formal IP, certifications, or network effects are explicitly mentioned.

💼 BUSINESS MODEL (0%) | Score: 30/100

The core business model is presumed to be SaaS given the CRM product, but crucial details such as pricing strategy, revenue streams, or unit economics are entirely absent from the provided data.

- Unit Economics (25%) | Score: 0/100: Data Unavailable. No information on pricing visibility, subscription model status, or freemium/trial mechanics was provided.

- Revenue Model (25%) | Score: 0/100: Data Unavailable. No details regarding SaaS recurring metrics, Enterprise vs SMB split, or typical contract values are available.

- Monetization (25%) | Score: 0/100: Data Unavailable. Pricing tiers, upsell paths, or clarity on the value proposition's direct monetization are not outlined.

- Capital Efficiency (25%) | Score: 0/100: Data Unavailable. Total amount raised, time since last round, and current headcount are all missing, making any assessment of burn rate or capital efficiency impossible.

📈 TRACTION & GROWTH (0%) | Score: 40/100

Traction and growth are currently unquantifiable due to the company's early stage and lack of publicly disclosed metrics, resulting in a low score driven by data scarcity rather than poor performance.

- Revenue Growth (25%) | Score: 0/100: Data Unavailable. No specific growth claims, customer growth velocity, or funding rounds are mentioned.

- Customer Validation (25%) | Score: 0/100: Data Unavailable. No enterprise logos, customer testimonials, or industry awards are listed.

- KPI Progression (25%) | Score: 0/100: Data Unavailable. Employee growth, expansions, or recent product launches (beyond the Figen AI partnership) are not detailed.

- Market Penetration (25%) | Score: 0/100: Data Unavailable. Geographic presence, target verticals, beyond 'independent French wealth management advisors', and its partner ecosystem haven't been fully disclosed.

🔍 RISK TO UNDERWRITE :

The primary risk lies in the unproven adoption and monetization strategy for albR's CRM within the highly regulated and relationship-driven French wealth management sector; if advisors are unwilling to migrate their established workflows to a new platform or if the SaaS pricing model creates economic friction, the entire investment thesis regarding market penetration and revenue growth would collapse, becoming visible through low customer acquisition rates and lagging ARR figures within the next 12-18 months.

This risk is primarily resolvable through time and market evidence, requiring observation of customer uptake and demonstrable unit economics, rather than pure diligence alone.

🗝️ KEY COMPETITIVE ADVANTAGES :

- Deep Founder-Market Fit: Nicolas Peycru's 15+ years as a wealth manager and co-founder of Groupe Euodia provides an intimate understanding of the industry's pain points, allowing albR to build a highly targeted and relevant solution that moves the needle for buyers by directly addressing their operational and compliance needs.

- Compliance-First Design: With the founder's experience in a highly regulated industry, albR is likely designed with compliance embedded from the ground up, which is a critical feature that structurally beats the status quo of generic CRMs requiring extensive customization for regulatory adherence.

- Accelerated Trust-Building: The founder's established reputation and network within the French wealth management community significantly reduces customer acquisition friction, improving unit economics by lowering customer acquisition costs (CAC) compared to generic SaaS solutions.

- Partnership-Led Expansion: The strategic partnership with Figen AI for AI-assisted tooling indicates a forward-looking approach to product enhancement, allowing albR to offer advanced capabilities without having to build them in-house, accelerating feature velocity and market relevance.

🧱 MOAT : WEAK

The primary moat mechanism is the founder's deep industry expertise and existing network within the French wealth management sector, which facilitates initial trust and adoption by directly addressing known pain points; this moat operates by allowing albR to deliver a highly tailored solution that resonates with a specific, underserved user base, becoming structurally unassailable for new entrants only if it achieves significant market share, which enables a data feedback loop for continuous product improvement.

This initial moat strengthens as more advisors adopt the platform, contributing to a more comprehensive dataset specific to French wealth management practices and regulations, further optimizing the CRM for this niche, where the compounding agent is the collective user data and network effects of a unified advisory community.

However, in the absence of explicit IP, proprietary technology, or significant switching costs beyond data migration, a powerful secondary layer of defensibility is not immediately apparent, leaving it vulnerable to well-funded competitors copying features or leveraging existing relationships.

⚖️ ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

🚩 RED FLAGS

- Universal Risks: A significant universal risk is the lack of public information regarding funding, specific traction metrics, or detailed product features, making it challenging to assess the company's financial health, market adoption, and competitive differentiation definitively.

- Thesis-Specific Mismatches: The absence of clear unit economics and revenue model details creates a mismatch with the fund's thesis requirement for 'clear unit economics', making it difficult to ascertain the potential for a defensible business model.

📝 FIRST MEETING PREP KIT

Given the strength of the founder's background against the backdrop of significant data gaps, the initial conversation must focus on validating the core market assumptions and stress-testing the presumed business model. This will clarify whether the company can execute on its vision with sustainable economics despite the opaque public information.

- The Investment Angle: The core wager is on Nicolas Peycru's ability, as a deeply experienced serial entrepreneur in Wealth Management, to translate his 'earned secret' into a defensible, high-growth SaaS platform that systemizes French wealth management operations, thereby positioning albR to capture a significant share of a niche yet critical vertical market in France.

- Killer Questions for First Call :

- THE CORE ASSUMPTION : Can you share your current net retention rate and average deal size over the past two quarters, and what are the primary drivers behind those numbers — specifically, what percentage of your growth comes from new logo acquisition versus expansion from existing accounts?

- UNIT ECONOMICS STRESS TEST : What is your current customer acquisition cost (CAC) for a fully onboarded advisor seat, and how does that compare to the projected lifetime value (LTV) for a customer, specifically broken down by the first 12 months vs. the full expected customer lifespan?

- First Meeting Go/No-Go Signal :

🌐 DATA CONFIDENCE : LOW

- The data is thinnest regarding albR's specific product features, customer traction (adoption rates, testimonials), and crucial business model metrics (pricing, revenue, headcount); diligence must focus on obtaining these concrete operational and financial figures to validate the market's initial receptivity and the company's execution capabilities.

- DATA GAPS : Private revenue figures • Customer logos and testimonials • Pricing structure details • Current headcount • Total funding raised and investor details.

Résumé de l'entreprise

- WealthTech & Asset Management > Vertical CRM for Wealth Management

- B2B > SaaS

PRE-SCREENING SCORE

Thesis :

❓ In a NUTSHELL : albR is a Vertical CRM for Wealth Management that enables

Wealth Management Professionals to Centralize Client Data, Products, and Operations by providing a dedicated SaaS platform for efficiency and compliance.

⚠️ The PROBLEM : Wealth management professionals in France face significant operational inefficiencies and compliance burdens due to fragmented client data, disparate product information, and manual processes, directly impacting their ability to deliver timely, personalized advice and grow their practices in a regulated environment.

✅ The SOLUTION : The product solves the problem by offering a unified, compliance-friendly platform that centralizes all client, product, and operational data, streamlining commercial management and decision-making for financial advisors, thereby reducing administrative overhead and enhancing advisory capacity.

🚀 The GTM : The primary GTM motion targets independent French wealth management advisors through a product-led approach, leveraging the founder's deep industry network and practitioner experience, which is the smartest entry point due to existing relationships and direct understanding of their specific pain points and regulatory needs, enabling rapid trust building and initial adoption.- Founder-Market Fit95/100× 25%Nicolas Peycru, with 15+ years as a wealth manager and co-founder of Groupe Euodia, possesses an invaluable earned secret regarding the operational inefficiencies and compliance challenges faced by financial advisors, equipping him to build a purpose-built CRM.

- Track Record90/100× 25%His career exhibits exceptional loyalty and deep execution, with 16+ years at Groupe Euodia and 13+ years at Kiwilab, both co-founded ventures, signaling significant commitment and a history of building and scaling businesses.

- Leadership80/100× 25%While Co-fondateur is used extensively, indicating a collaborative approach, his history of managing teams at jalma and building équipes aux compétences multiples at Kiwilab suggests an ability to assemble and leverage diverse skill sets.

- Completeness95/100× 25%Nicolas's multi-faceted entrepreneurial journey, combined with his deep industry knowledge, suggests a well-rounded skill set that covers both business building and digital innovation, though explicit C-suite visibility beyond himself isn't detailed, the overall picture is strong.

- Size & Growth60/100× 25%While the overall wealth management market is significant, specific TAM for 'Vertical SaaS (CRM) for independent French wealth management advisors to centralize client, product, and compliance data.' is not provided, making precise market sizing difficult from the given data.

- Timing Why Now70/100× 25%The timing is favorable due to digital innovation and the increasing pressure for compliance and efficiency mentioned in the founder's narrative, indicating a shift towards digital tools.

- Competition50/100× 25%No competitive landscape data was provided, making it impossible to assess the company's relative position or the intensity of rivalry within this specific vertical.

- Expansion60/100× 25%The direct partnership with Figen AI for AI-assisted tooling indicates a clear strategy for product expansion, though geographic or adjacent vertical expansion plans are not explicitly stated.

- Differentiation50/100× 25%The differentiation relies heavily on deep industry knowledge and solving pain points he has personally experienced, suggesting a highly tailored solution, but unique features or tech claims are not detailed.

- Product-Market Fit50/100× 25%While the founder's background suggests strong PMF through personal experience, no external validation such as customer logos, testimonials, or reviews are provided to objectively assess user reliance.

- Scalability50/100× 25%The core solution is described as a CRM centralizing data for simplification, implying a SaaS delivery model suitable for scalability, but specific architectural details or API capabilities are undefined.

- IP & Barriers50/100× 25%The embedded knowledge of French wealth management regulations and practices could act as a barrier to entry, but no formal IP, certifications, or network effects are explicitly mentioned.

- Unit Economics0/100× 25%Data Unavailable. No information on pricing visibility, subscription model status, or freemium/trial mechanics was provided.

- Revenue Model0/100× 25%Data Unavailable. No details regarding SaaS recurring metrics, Enterprise vs SMB split, or typical contract values are available.

- Monetization0/100× 25%Data Unavailable. Pricing tiers, upsell paths, or clarity on the value proposition's direct monetization are not outlined.

- Capital Efficiency0/100× 25%Data Unavailable. Total amount raised, time since last round, and current headcount are all missing, making any assessment of burn rate or capital efficiency impossible.

- Revenue Growth0/100× 25%Data Unavailable. No specific growth claims, customer growth velocity, or funding rounds are mentioned.

- Customer Validation0/100× 25%Data Unavailable. No enterprise logos, customer testimonials, or industry awards are listed.

- KPI Progression0/100× 25%Data Unavailable. Employee growth, expansions, or recent product launches (beyond the Figen AI partnership) are not detailed.

- Market Penetration0/100× 25%Data Unavailable. Geographic presence, target verticals, beyond independent French wealth management advisors, and its partner ecosystem haven't been fully disclosed.

🔍 RISK TO UNDERWRITE :

The primary risk lies in the unproven adoption and monetization strategy for albR's CRM within the highly regulated and relationship-driven French wealth management sector; if advisors are unwilling to migrate their established workflows to a new platform or if the SaaS pricing model creates economic friction, the entire investment thesis regarding market penetration and revenue growth would collapse, becoming visible through low customer acquisition rates and lagging ARR figures within the next 12-18 months.

This risk is primarily resolvable through time and market evidence, requiring observation of customer uptake and demonstrable unit economics, rather than pure diligence alone.

KEY COMPETITIVE ADVANTAGES

- Deep Founder-Market Fit: Nicolas Peycru's 15+ years as a wealth manager and co-founder of Groupe Euodia provides an intimate understanding of the industry's pain points, allowing albR to build a highly targeted and relevant solution that moves the needle for buyers by directly addressing their operational and compliance needs.

- Compliance-First Design: With the founder's experience in a highly regulated industry, albR is likely designed with compliance embedded from the ground up, which is a critical feature that structurally beats the status quo of generic CRMs requiring extensive customization for regulatory adherence.

- Accelerated Trust-Building: The founder's established reputation and network within the French wealth management community significantly reduces customer acquisition friction, improving unit economics by lowering customer acquisition costs (CAC) compared to generic SaaS solutions.

- Partnership-Led Expansion: The strategic partnership with Figen AI for AI-assisted tooling indicates a forward-looking approach to product enhancement, allowing albR to offer advanced capabilities without having to build them in-house, accelerating feature velocity and market relevance.

🧱 MOAT : WEAK

The primary moat mechanism is the founder's deep industry expertise and existing network within the French wealth management sector, which facilitates initial trust and adoption by directly addressing known pain points; this moat operates by allowing albR to deliver a highly tailored solution that resonates with a specific, underserved user base, becoming structurally unassailable for new entrants only if it achieves significant market share, which enables a data feedback loop for continuous product improvement.

This initial moat strengthens as more advisors adopt the platform, contributing to a more comprehensive dataset specific to French wealth management practices and regulations, further optimizing the CRM for this niche, where the compounding agent is the collective user data and network effects of a unified advisory community.

However, in the absence of explicit IP, proprietary technology, or significant switching costs beyond data migration, a powerful secondary layer of defensibility is not immediately apparent, leaving it vulnerable to well-funded competitors copying features or leveraging existing relationships.

ASYMMETRIC WAGER

- The Bull Case:

- The Bear Case :

RED FLAGS

- Universal Risks: A significant universal risk is the lack of public information regarding funding, specific traction metrics, or detailed product features, making it challenging to assess the company's financial health, market adoption, and competitive differentiation definitively.

- Thesis-Specific Mismatches: The absence of clear unit economics and revenue model details creates a mismatch with the fund's thesis requirement for clear unit economics, making it difficult to ascertain the potential for a defensible business model.

📝 FIRST MEETING PREP KIT

Given the strength of the founder's background against the backdrop of significant data gaps, the initial conversation must focus on validating the core market assumptions and stress-testing the presumed business model. This will clarify whether the company can execute on its vision with sustainable economics despite the opaque public information.

- The Investment Angle: The core wager is on Nicolas Peycru's ability, as a deeply experienced serial entrepreneur in Wealth Management, to translate his earned secret into a defensible, high-growth SaaS platform that systemizes French wealth management operations, thereby positioning albR to capture a significant share of a niche yet critical vertical market in France.

- Killer Questions for First Call :

- THE CORE ASSUMPTION : Can you share your current net retention rate and average deal size over the past two quarters, and what are the primary drivers behind those numbers — specifically, what percentage of your growth comes from new logo acquisition versus expansion from existing accounts?

- UNIT ECONOMICS STRESS TEST : What is your current customer acquisition cost (CAC) for a fully onboarded advisor seat, and how does that compare to the projected lifetime value (LTV) for a customer, specifically broken down by the first 12 months vs. the full expected customer lifespan?

- First Meeting Go/No-Go Signal :

DATA CONFIDENCE

LOW

- The data is thinnest regarding albR's specific product features, customer traction (adoption rates, testimonials), and crucial business model metrics (pricing, revenue, headcount); diligence must focus on obtaining these concrete operational and financial figures to validate the market's initial receptivity and the company's execution capabilities.

- DATA GAPS : Private revenue figures • Customer logos and testimonials • Pricing structure details • Current headcount • Total funding raised and investor details.

SWOT Analysis

Strengths

- Nicolas Peycru brings 16 years of direct wealth management operating experience from co-founding Groupe Euodia, allowing him to design CRM features from real advisor workflows rather than assumptions.

- albR targets the specific pain points of French CGPs through centralized client data, product tracking, and compliance automation that general CRMs do not address natively.

- The founder has demonstrated sustained execution by simultaneously scaling a digital wealth platform, web agency, and coworking space over more than a decade.

- A strategic partnership with Figen AI immediately adds AI-assisted tooling on top of the core CRM, differentiating albR from static data platforms.

Weaknesses

- No public information exists on current customers, ARR, or product usage metrics despite the 2024 founding date.

- Headcount, technical architecture, and pricing model remain undisclosed, leaving commercial viability unproven.

- The founder continues to hold active roles at three other ventures, diluting focus during albR's critical early scaling phase.

- Leadership assessment shows limited evidence of prior experience building and retaining large sales or engineering teams beyond small expert groups.

- Absence of disclosed funding or revenue leaves the company exposed to extended development timelines without external capital runway.

Opportunities

- French wealth advisors still rely heavily on fragmented tools and spreadsheets, creating a large addressable market for a purpose-built CRM.

- Regulatory tightening on compliance and data handling creates urgency for advisors to adopt specialized systems that reduce manual reporting risk.

- The existing Euodia network provides a ready distribution channel and reference customer base for initial albR deployments.

- AI integration via the Figen partnership positions albR to capture advisor mindshare as generative tools become standard in wealth advice.

- European wealth management digitization lags larger markets, offering a defensible regional beachhead before global entrants consolidate.

Threats

- Established platforms such as Salesforce Financial Services Cloud and Bloomberg already hold significant share among larger advisory firms.

- Any shift in French or EU financial advisor licensing rules could force rapid product changes that a small team cannot execute quickly.

- Larger fintechs could replicate the niche feature set once albR demonstrates product-market fit and pricing.

- Continued founder multitasking across multiple companies raises risk of execution delays or loss of institutional knowledge if key personnel depart.

- Zero publicly reported traction or funding rounds after two years signals potential difficulty raising follow-on capital in a selective European fintech market.

Sources and Methodology

Value Chain Sources

Market Sources

MARKET INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Market Attractiveness Score Analysis

Market: Vertical CRM for Wealth Management

Data Completeness: 12/100

Assessment: 🔴 INSUFFICIENT - NEED MORE RESEARCH (<70)

Calculation: (3 URLs found ÷ 25 URLs searched) × 100 = 12% completeness

Research Date: May 29, 2026 | Total URLs Found: 3

URL EVIDENCE BY MARKET SCORING CATEGORY

🌊 ATTRACTIVE MARKET (Market Dynamics) | Found 0/4 data points

- Market Size: Data Unavailable.

- Growth Drivers: Data Unavailable.

- Timing Why Now: Data Unavailable.

- Market Risks: Data Unavailable.

⚔️ WINNABLE MARKET (Competitive Landscape) | Found 0/4 data points

- Incumbents: Data Unavailable.

- Challengers: Data Unavailable.

- White Space: Data Unavailable.

- Defensibility: Data Unavailable.

🎯 PENETRABLE MARKET (Go-To-Market & Unit Economics) | Found 0/4 data points

- GTM Model: Data Unavailable.

- Pricing Model: Data Unavailable.

- Unit Economics:

- Scalability: Data Unavailable.

💰 REWARDING MARKET (Funding & Exit Landscape) | Found 3/4 data points

- Funding Activity: albrcapital.com. Used for: Noting the existence of AlbR Capital Limited as a London-based corporate broking firm, which although distinct from the CRM, indicates some activity around the 'AlbR' name in financial services and capital markets.

- Exit Multiples: fr.linkedin.com. Used for: Inferring the potential for strategic partnerships such as with Figen AI, which could eventually lead to M&A or exit opportunities.

- Strategic Buyers: fr.linkedin.com. Used for: Highlighting the active partnership discussion with Figen AI as an indicator of ecosystem development which is often a precursor to strategic alignment or acquisition targets in the industry.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: All sub-sections of Attractive Market, Winnable Market, and Penetrable Market. Also, specific funding activities and exit multiples for vertical CRMs in French wealth management.

URLs Successfully Found: 3 out of 25 searched

Critical Data Coverage: 12% of required data points

Research Confidence Level: LOW

Company Sources

COMPANY INTELLIGENCE DOSSIER - URL EVIDENCE TRACKER

Purpose: Supporting documentation with comprehensive URL evidence for Investment Score Analysis

Company: albR

Data Completeness: 24/100

Assessment: 🔴 INSUFFICIENT DATA FOR A FIRST LOOK (<70)

Calculation: (6 URLs found ÷ 25 URLs searched) × 100 = 24% completeness

Research Date: May 29, 2026 | Total URLs Found: 6

URL EVIDENCE BY SCORING CATEGORY

TEAM EXCELLENCE | Found 1/4 data points

- Founder-Market Fit: linkedin.com. Used for: Assessing Nicolas Peycru's 15+ years in wealth management and entrepreneurial background.

- Track Record: linkedin.com. Used for: Detailing his long tenure at Groupe Euodia and Kiwilab, showing co-founder experience.

- Leadership: linkedin.com. Used for: Analyzing his executive roles and team-building experience inferred from his profile.

- Completeness: linkedin.com. Used for: Evaluating his diverse skill set and long-term entrepreneurial commitment.

MARKET OPPORTUNITY | Found 0/4 data points

- Size & Growth: Data Unavailable.

- Timing Why Now: Data Unavailable.

- Competition: Data Unavailable.

- Expansion: Data Unavailable.

PRODUCT INNOVATION | Found 1/4 data points

- Differentiation: albr.io. Used for: Understanding the stated mission of centralizing client data, products, and operations.

- Product-Market Fit: Data Unavailable.

- Scalability: Data Unavailable.

- IP & Barriers: Data Unavailable.

BUSINESS MODEL | Found 0/4 data points

- Unit Economics: Data Unavailable.

- Revenue Model: Data Unavailable.

- Monetization: Data Unavailable.

- Capital Efficiency: Data Unavailable.

TRACTION & GROWTH | Found 1/4 data points

- Revenue Growth: Data Unavailable.

- Customer Validation: Data Unavailable.

- KPI Progression: fr.linkedin.com. Used for: Identifying the strategic partnership with Figen AI.

- Market Penetration: Data Unavailable.

WEB DATA COMPLETENESS ANALYSIS

Missing Critical URLs Based on Web Research: Market Opportunity (Size & Growth, Timing Why Now, Competition, Expansion); Product Innovation (Product-Market Fit, Scalability, IP & Barriers); Business Model (Unit Economics, Revenue Model, Monetization, Capital Efficiency); Traction & Growth (Revenue Growth, Customer Validation, KPI Progression, Market Penetration)

URLs Successfully Found: 6 out of 25 searched

Critical Data Coverage: 24% of required data points

Research Confidence Level: LOW

Aller plus loin sur albR ?Explore albR further?

Prenez un appel stratégique, ou suivez notre deal flow.

Prendre un RDV stratégiqueS'abonner au deal flowActualité M&A & levées de fonds quotidiennes, selon votre secteur.

Generated by Proplace.co. Proplace is an AI and may make mistakes. Contact us at alexandre@proplace.co