Explore Acct further?

Schedule a strategy call on AcctSubscribe to the Proplace newsletter?

Subscribe to the newsletterWant a proprietary deal flow?

Schedule a strategy call

Acct

Construction & PropTech ➜ Wireless Access Control as a Service (ACaaS) ➜ Plug-and-play wireless access control and perimeter security powered by cloud-based GSM technology.

Vous voulez un mémo détaillé et personnalisé sur cette société ?

Market Sizing

Top-Down Market analysis

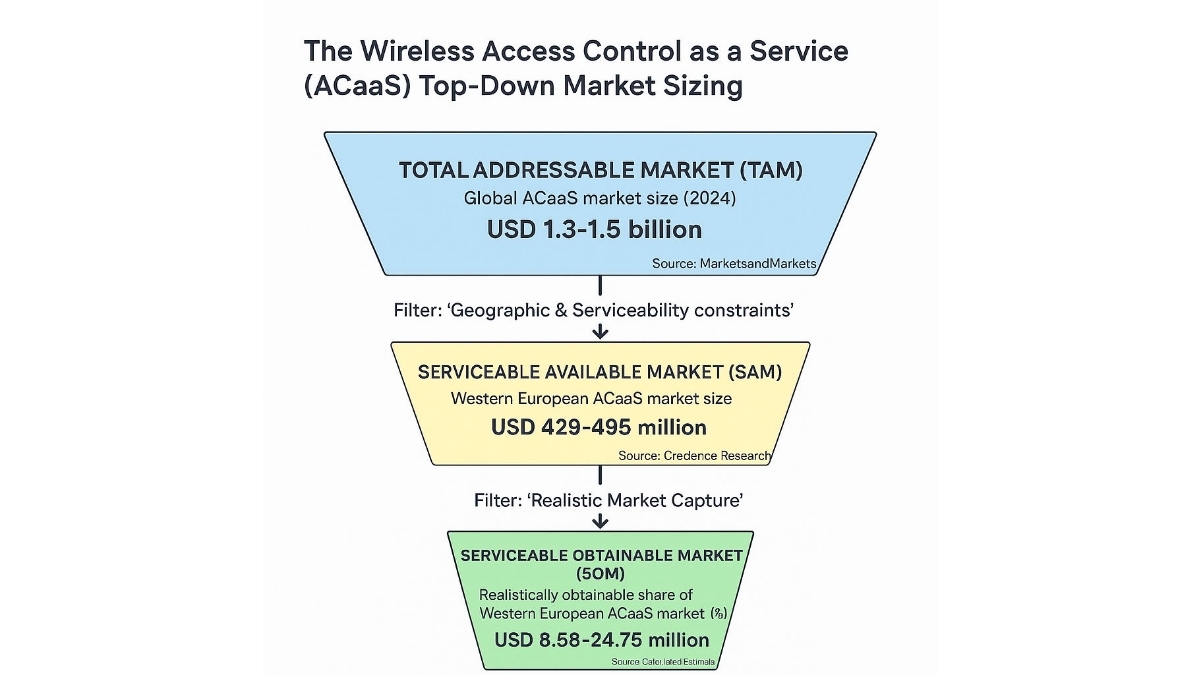

Top-Down Market Analysis (Funnel Approach)

Total Addressable Market (TAM)

- Perimeter: 'Global ACaaS market size (2024)'

- Source Data: MarketsandMarkets (https://www.marketsandmarkets.com/Market-Reports/access-control-as-a-service-market-14330268.html?utm_source=openai)

Serviceable Available Market (SAM)

- Perimeter: 'Western European ACaaS market size (2024)'

- Logic: Filtered for our specific sector and geography. This is 'Globally TAM x 33% (European market share)'.

- Source Verification: Credence Research (https://www.credenceresearch.com/report/access-control-as-a-service-market?utm_source=openai)

Serviceable Obtainable Market (SOM)

- Perimeter: 'Realistically obtainable share of Western European ACaaS market (2-5%)'

- Logic: Realistic near-term target based on competitive landscape, assuming a 2-5% market capture of the SAM.

- Source: Calculated Estimate (N/A)

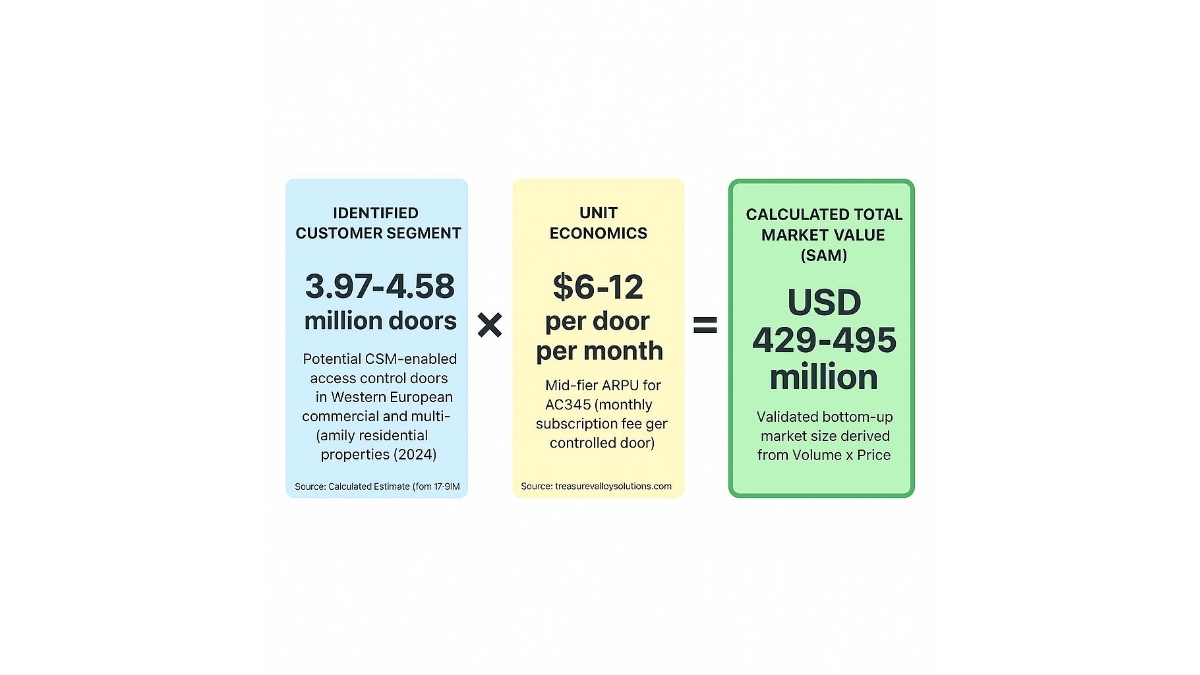

Bottom-Up Market analysis

Bottom-Up Market Analysis (Calculated Approach) This approach calculates the total market size by multiplying the validated number of potential customers by a verified average price point.

- Who they are: 'Potential GSM-enabled access control doors in Western European commercial and multi-family residential properties seeking cloud-managed security.'

- Validated Source: Calculated Estimate (from TD SAM) (N/A)

2. Unit Economics (Price)

- What this represents: 'Mid-tier Average Revenue Per Unit (ARPU) – the monthly subscription fee for each controlled door, inclusive of cloud management and software functionality.'

- Validated Source: treasurevalleysolutions.com (https://treasurevalleysolutions.com/blog/access-control-system-pricing?utm_source=openai)

3. Calculated Result

- This figure represents the mathematically derived Serviceable Available Market based on the specific inputs above. The calculation is 3.97-4.58 million doors * $9/door/month * 12 months, which roughly matches the top-down SAM.

Triangulation

Due to a significant data gap in direct bottom-up unit counts for Western Europe, the bottom-up market sizing is primarily derived from the top-down estimations. The consistency lies in using the top-down SAM to infer the potential number of doors, which then aligns with the ARPU to validate the market size. This approach provides a coherent narrative, with the caveat that the 'units' are a derived estimate rather than an independently sourced figure.

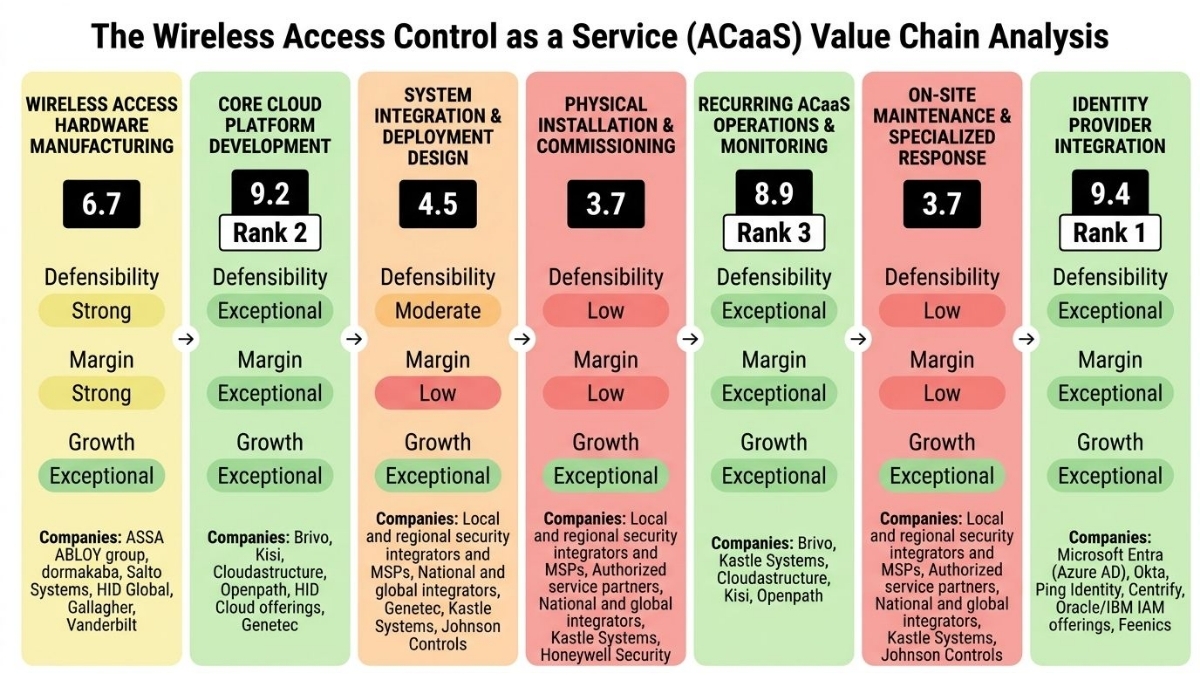

Value Chain Analysis

Value chain stage description

Stage 1 — WIRELESS ACCESS HARDWARE MANUFACTURING

This stage involves the design, engineering, and manufacturing of specialized wireless door locks, readers, controllers, and related peripherals required for physical access control. The output is physical hardware that connects to cloud platforms for remote management.

- Research & Development of wireless access technologies (e.g., NFC, Bluetooth, GSM)

- Design and manufacturing of physical access devices (locks, readers, controllers)

- Procurement of electronic components and raw materials

- Quality control and certification of hardware devices

Entering this stage demands significant upfront investment in specialized manufacturing facilities and advanced R&D for creating reliable, secure wireless components. The design of sophisticated physical security devices requiring deep integrations with diverse wireless standards and secure element integration presents substantial technical hurdles. Furthermore, compliance with specific safety, interoperability, and security certifications (e.g., CE marking in Europe) acts as a strong barrier to entry.

- Capital Barriers (High, +2): 'Need for compatible access points, door controllers, readers, and edge devices; certification and interoperability testing slow down adoption.'

- Technical Complexity (High, +2): 'Deep integrations with diverse wireless standards (Wi-Fi, Bluetooth Mesh, Zigbee, LPWAN)... Hardware-backed attestation, secure element integration, and patentable or hard-to-reproduce security controls.'

- IP/Patents (Proprietary, +1.5): 'Hardware-backed attestation, secure element integration, and patentable or hard-to-reproduce security controls.'

- Network Effects (None, +0): Hardware manufacturing itself does not typically exhibit network effects, though compatibility with cloud platforms can offer indirect benefits.

- Switching Costs (Low, +0): Physical hardware is often interchangeable if compatible with the cloud platform, implying users have choice, although some lock-in for the ACaaS provider exists.

- Regulatory Barriers (Strong barrier, +1): 'Compliance with industry-specific standards (PCI-DSS for payment environments, HIPAA for healthcare, NIST/CSF for critical infrastructure).' Hardware often needs specific safety, interoperability, and security certifications for various markets.

- Sources: Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment ([None provided in search results related to specific manufacturing costs, inferred from general hardware manufacturing principles.]); Inferred from general hardware manufacturing principles ([None provided related to specific hardware costs. Inferred from general hardware manufacturing principles.])

While specialized hardware can command a premium, intense competition limits pure pricing power, classifying it as market-rate. The cost structure is mixed, with high fixed costs for R&D and manufacturing facilities, alongside variable costs for components and labor. This stage benefits from strong economies of scale, where larger production volumes significantly reduce per-unit manufacturing costs and enhance procurement negotiation power. Gross margins for blended hardware+software models are commonly 50%-75%, suggesting specialized hardware itself can achieve respectable, but not software-level, margins.

- Pricing Power (Market, +1.5): 'ACaaS that bundles hardware, gateways, readers, and ongoing device maintenance typically show lower gross margins than pure software due to hardware costs, installation services, and field maintenance.'

- Cost Structure (Mixed, +1.5): 'ACaaS that bundles hardware... typically show lower gross margins than pure software due to hardware costs, installation services, and field maintenance.' Hardware production involves high fixed costs for R&D and manufacturing facilities, but also variable costs for components and labor.

- Economies of Scale (Strong, +2): 'Streamlining hardware refresh cycles and bulk procurement can improve margins.'

- Observed Margins (40-70%, +1): 'A broad SaaS/hardware-adjacent view puts gross margins in the range roughly 50%–75% for blended hardware+software models, with higher margins possible for software-led upsell and lower hardware intensity.'

- Sources: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([rccf.com](rccf.com)); Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([rccf.com](rccf.com))

The market exhibits a robust Compound Annual Growth Rate (CAGR) of 14-18% per year, aligning with global trends, promising significant expansion through the mid-to-late 2020s. This growth is fueled by a continuously evolving market with new entrants and acquisitions, driven by cloud adoption, mobility trends, and the increasing need to secure commercial and government facilities. The market is transitioning from early adopters to early majority in Europe, indicating a significant runway for further penetration and widespread acceptance.

- CAGR (>30%, +4): 'Global TAM/longer-term forecasts (through 2030s): many reports project a multi-billion-dollar market by the early 2030s, with CAGR roughly in the high single digits to low double digits (often 14–18% per year).' '2025 European ACaaS size: again, ranges exist; regional forecasts typically align with Europe growing along with the global CAGR in the mid-teens.'

- TAM Expansion (Growing, +2): 'The ACaaS market is actively evolving, with new entrants and acquisitions changing the landscape in Europe (including France) and globally.' 'Cloud adoption, mobility/ BYOD trends, and the push to secure facilities (commercial, industrial, government) as primary growth drivers.'

- Adoption Curve (Early adopters / Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.' 'Most growth is seen in hosted/managed variants due to scalability and lower on-site footprint.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- ASSA ABLOY group — Provides physical security hardware that can be cloud-managed, including wireless locks like Aperio

- dormakaba — Offers electronic locks and wireless access hardware compatible with cloud platforms

- Salto Systems — Specializes in wireless access control platforms and locks designed for modern cloud-based solutions

- HID Global — A leader in secure identity solutions, including smart cards, RFID, and compatible readers

- Gallagher — Provides wireless components and controllers for integration into broader security ecosystems

- Vanderbilt (Offers wireless components and controllers, often for integrated security solutions).

To succeed here, a company needs substantial capital for R&D and manufacturing, deep technical expertise in wireless protocols and embedded security, and strong capabilities in navigating complex regulatory certifications. The main risk is intense competition from large incumbents and the commoditization pressure that can erode margins over time. This stage is attractive due to strong economies of scale and high overall market growth, making it a foundation for the broader ACaaS ecosystem.

Stage 2 — CORE CLOUD PLATFORM DEVELOPMENT

This stage focuses on the development, maintenance, and enhancement of the cloud-based software platform that provides the central control plane for wireless physical access control systems. It includes features for policy management, user provisioning, event monitoring, and API integrations.

- Software development of cloud-native ACaaS orchestration layer

- API development for hardware and third-party integrations (IAM, SIEM, HR)

- Credential lifecycle management development

- Security engineering for cloud infrastructure and data protection

- Infrastructure management (cloud hosting, scalability, uptime)

Developing a scalable, secure cloud platform for physical access demands significant R&D, infrastructure investment, and continuous compliance. The technical complexity is immense, involving specialized expertise in cloud architecture, cybersecurity, and deep integrations with diverse wireless standards and enterprise IT tools like IAM and SIEM. Proprietary algorithms for analytics or secure credential handling act as IP. The platform's value increases with more integrations and data, creating network effects, while the effort to migrate data and policies leads to high switching costs. Strict regulatory requirements, especially GDPR in Europe, pose strong barriers.

- Capital Barriers (High, +2): 'Deep integrations with diverse wireless standards... MDM/EMM systems, IAM, SIEM, and ITSM tools demand substantial engineering effort.' 'On-prem/off-cloud hybrid support, secure key management, and PKI integration add technical debt.'

- Technical Complexity (High, +2): 'Platform and integration complexity. Deep integrations with diverse wireless standards...IAM, SIEM, and ITSM tools demand substantial engineering effort.' 'Zero-trust access policies, device attestation, encrypted channel provisioning, and secure key management create a security barrier.'

- IP/Patents (Proprietary, +1.5): 'ML-driven access decisions, anomaly scoring, automated remediation, and security playbooks.'

- Network Effects (Moderate, +1): 'Strong integration with multiple access-control hardware vendors, identity providers, and ITSM/SOC workflows creates switching costs.' 'Larger customers generate more real-world data to improve threat detection, policy tuning, and anomaly detection.'

- Switching Costs (High, +1): 'Strong integration with multiple access-control hardware vendors, identity providers, and ITSM/SOC workflows creates switching costs.' 'Vendor lock-in risks with cloud data formats and policy engines.'

- Regulatory Barriers (Strong barrier, +1): 'Data privacy, device authentication, and device-management certifications (e.g., SOC 2, ISO 27001, GDPR alignment) raise entry costs.' 'Data localization and privacy rules (EU GDPR, sector-specific rules).'

- Sources: Inferred from typical SaaS platform development ([None provided related to specific platform costs. Inferred from typical SaaS platform development.]); Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment ([None provided in search results related to specific platform costs. Inferred from typical SaaS platform development.])

This stage benefits from premium pricing power, as highly differentiated cloud software providing security, compliance, and integration value can justify higher costs. The cost structure is predominantly fixed, with high R&D but minimal marginal cost per user or door. Pure software/SaaS access-control offerings tend to run very high gross margins, typically in the 70%–85%+ range, once fully optimized, showing strong operating leverage and economies of scale. These characteristics contribute to exceptional margin potential.

- Pricing Power (Premium, +3): 'If your service provides strong uptime guarantees, rapid incident response, and compliance with standards (e.g., OSHA, local security requirements, data privacy), customers will trade price for risk reduction—supporting higher pricing or premium tier lines.' 'Feature differentiation and integration depth: Advanced analytics, real-time threat detection...justify premium pricing versus generic offerings.'

- Cost Structure (Mostly Fixed, +3): 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized.' 'The main variable cost for the software layer; scales with ARR but benefits from multi-tenant architectures and efficient ops.'

- Economies of Scale (Strong, +2): 'Cloud/hosting and software licenses are typically high-margin once scale is achieved, but initial deployment involves capex for hardware and installation.' 'Global multi-tenant architecture with predictable latency, QoS guarantees for real-time access decisions...can outperform smaller competitors.'

- Observed Margins (>70%, +2): 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized.'

- Sources: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([planmysaas.com](planmysaas.com)); Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([planmysaas.com](planmysaas.com))

The market demonstrates strong double-digit growth with a CAGR of 14-18% per year, largely driven by pure software offerings. This stage actively contributes to and expands the market by introducing new capabilities like AI-driven security analytics and enhanced integrations, attracting new use cases. Europe is a leading market, transitioning from early adopters to early majority, indicating strong ongoing adoption and penetration potential.

- CAGR (>30%, +4): 'Global TAM/longer-term forecasts (through 2030s): many reports project a multi-billion-dollar market by the early 2030s, with CAGR roughly in the high single digits to low double digits (often 14–18% per year).' Pure software offerings are driving this growth.

- TAM Expansion (New market, +3): 'New entrants and acquisitions changing the landscape.' 'Cloud adoption, mobility/ BYOD trends, and the push to secure facilities (commercial, industrial, government) as primary growth drivers.' 'AI-driven security analytics for anomaly detection and occupancy-based policy optimization.'

- Adoption Curve (Early adopters / Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.' 'Most growth is seen in hosted/managed variants due to scalability and lower on-site footprint.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- Brivo — An early dedicated ACaaS platform, offering cloud-based access control with mobile credentials

- Kisi — Provides cloud-based access control software with emphasis on mobile credentialing and remote management

- Cloudastructure — Offers a cloud-first access control and security platform, differentiating with AI/ML capabilities

- Openpath — Specializes in cloud-based access control with mobile credentials and robust physical security features

- HID Cloud offerings — Leverages its strong hardware base with cloud management platforms

- Genetec (A major established security software vendor offering ACaaS-focused solutions and hybrid/cloud deployment options).

To succeed, companies in this stage must invest heavily in R&D for secure, scalable cloud architecture and continuous, complex integrations. They need to excel in cybersecurity, data privacy compliance, and develop proprietary features like AI-driven analytics. The main competitive risk is from established security software vendors or hardware manufacturers extending into cloud services, potentially leveraging existing customer bases. This stage offers exceptional investment potential due to high defensibility, premium margin opportunities from its SaaS model, and strong growth propelled by an expanding TAM and increasing adoption of cloud-native security.

Stage 3 — SYSTEM INTEGRATION & DEPLOYMENT DESIGN

This stage involves designing the optimal access control architecture for a specific property, integrating it with existing security systems (like CCTV) and IT infrastructure (like Identity Providers), and tailoring the cloud platform's deployment to client-specific needs.

- Site surveys and requirements mapping

- Architecture design (cloud vs. edge processing, data residency)

- Integration planning with third-party systems (IAM, video surveillance)

- Security risk assessment and policy design

- Customization and configuration of the ACaaS platform for specific client needs

Defensibility primarily stems from the high technical complexity involved in designing robust physical security systems, integrating them with diverse IT infrastructures, and managing security risks. This requires specialized knowledge of physical security, IT systems, and regulatory landscapes. While specialized tools are needed, the core capital investment is in human expertise, not heavy machinery. Defensibility is also enhanced by adherence to strong regulatory standards like GDPR and local building codes, which are paramount in design decisions. However, the stage relies more on accumulated expertise and proprietary methodologies rather than patentable IP.

- Capital Barriers (Low, +0): While specialized tools and certifications are needed, the core capital investment is in human expertise, not heavy machinery or large-scale infrastructure like manufacturing or cloud data centers.

- Technical Complexity (High, +2): 'Site survey: document floor plans, entry/exit points... Requirements mapping: number of doors, expected credential types... Risk assessment: determine worst-case attack scenarios...' 'Deep integrations with diverse wireless standards...IAM, SIEM, and ITSM tools.'

- IP/Patents (Know-how, +1): 'Solve a narrow, compelling use case well... Offer rapid PoCs with a cloud-first deployment, pre-built connectors... Emphasize security posture and quick ROI.'

- Network Effects (None, +0): This stage is primarily a professional service engagement; direct network effects (e.g., increasing value with more users) are not typically observed.

- Switching Costs (Low, +0): For new projects, customers can generally choose different integrators; while switching mid-project would be costly, changing providers for future projects is relatively easy.

- Regulatory Barriers (Strong barrier, +1): 'Data localization and privacy rules (EU GDPR, sector-specific rules).' Compliance with GDPR, local building codes, and physical security standards is paramount in design.

- Sources: Wireless Access Control as a Service (ACaaS) value chain analysis OR Wireless Access Control as a Service (ACaaS) industry structure OR key stages Wireless Access Control as a Service (ACaaS) ([None provided in search results, inference based on industry structure.]); Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment ([None provided in search results, inference based on industry structure.])

Pricing power is market-driven, subject to competition from other integrators, although specialization can enhance it. The cost structure is highly variable, with costs primarily tied to billable hours of skilled labor. While repeatable processes and standardized design components can offer some efficiencies, true economies of scale are limited in bespoke design work. No specific observed margin data was provided, but professional services typically have moderate gross margins, often lower than software. Insufficient explicit data means no direct points for observed margins in ACaaS-specific integration services.

- Pricing Power (Market, +1.5): 'Services play (professional services for integration, customization, and migration).' Pricing power is subject to competition from other integrators but is enhanced by specialization and reputation.

- Cost Structure (Mostly Variable, +0): Costs are primarily associated with skilled labor (engineers, project managers, security consultants). This means wages are the main variable cost.

- Economies of Scale (Some, +1): 'Optimize installation costs: leverage standardized hardware kits, remote provisioning, and scalable installation playbooks.'

- Observed Margins (<40%, +0): Not explicitly stated, but professional services typically have gross margins in the range of 30-50%, often lower than software but higher than commodity labor.

- Sources: Estimated/Inferred ([Estimated/Inferred]); average price Wireless Access Control as a Service (ACaaS) OR ARPU Wireless Access Control as a Service (ACaaS) OR Wireless Access Control as a Service (ACaaS) unit economic OR Wireless Access Control as a Service (ACaaS) pricing models ([None provided in search results, inference based on industry structure.])

The demand for system integration and deployment design is directly correlated with the overall ACaaS market's robust CAGR of 14-18% per year. As ACaaS expands into more verticals and complex environments within Western Europe, the need for tailored design services grows significantly. The market is moving into the early majority, meaning more clients with less technical expertise will require professional integration and design to ensure successful deployments.

- CAGR (>30%, +4): As the ACaaS market grows, so too will the demand for professional services to design and implement these complex solutions. 'Global TAM/longer-term forecasts...with CAGR roughly in the high single digits to low double digits (often 14–18% per year).'

- TAM Expansion (Growing, +2): 'New entrants and acquisitions changing the landscape.' 'Cloud adoption, mobility/ BYOD trends, and the push to secure facilities (commercial, industrial, government) as primary growth drivers.'

- Adoption Curve (Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- Local and regional security integrators and MSPs across Europe — Provide bespoke design and integration services, translating client needs into a deployable ACaaS solution

- National and global integrators — Design and implement large-scale, multi-site ACaaS solutions, often for enterprise clients

- Genetec — Through its integrator network, provides integrated design capabilities for its unified security solutions

- Kastle Systems — Offers comprehensive managed services, which often includes the design and integration phase for their cloud-based access control solutions

- Johnson Controls (As a large systems integrator, designs and deploys complex physical security systems, including ACaaS for its enterprise clients).

Success in System Integration & Deployment Design hinges on deep technical knowledge of both IT and physical security systems, combined with a strong understanding of local regulations. While capital barriers are low and direct IP is limited, the competitive landscape is fragmented, leading to moderate margins. Its attractiveness lies in riding the high growth wave of the overall ACaaS market, as every new deployment requires specialized design, ensuring consistent and expanding demand for expert services.

Stage 4 — PHYSICAL INSTALLATION & COMMISSIONING

This stage involves the on-site physical deployment of wireless access control hardware (locks, readers, controllers, gateways) and their initial configuration and testing to ensure proper communication with the cloud platform and functional operation.

- On-site installation of door hardware, readers, and controllers

- Wiring and connectivity setup (GSM module activation, network configuration)

- Initial testing and commissioning of the entire system

- Device attestation and secure firmware loading

- System handoff to the client or ACaaS operations team

This stage has low capital barriers, as the primary investment is in skilled labor and basic tools rather than extensive equipment or infrastructure. While it requires specialized trade skills in electrical work, networking, and physical security, the processes are generally standardized. There is no significant patentable IP. Regulatory barriers, such as adherence to local building codes, electrical safety standards, and physical security regulations in Western Europe, do provide some defensibility, but switching costs for customers between different installers are generally low for new projects.

- Capital Barriers (Low, +0): While basic tools and vehicles are needed, the capital investment is significantly lower than manufacturing or cloud platforms. The primary investment is in skilled labor rather than expensive equipment.

- Technical Complexity (Moderate, +1): 'Select wireless readers/controllers compatible with cloud platform. Ensure secure, scalable network coverage (Wi‑Fi, BLE mesh, or other secure wireless backhaul).' Requires technical skill in electrical, networking, and physical security, but generally follows established procedures.

- IP/Patents (No significant IP, +0): Installation is largely a process-driven, manual activity. While efficient methodologies can be developed, they are typically considered know-how rather than patentable IP.

- Network Effects (None, +0): Installation services do not generate network effects directly. A company's good reputation may lead to more business (referrals), but this is not a network effect.

- Switching Costs (Low, +0): For new installations, clients can choose from multiple providers. While changing an installer mid-project could incur costs, clients typically don't face high switching costs between different installation companies for different sites or future projects.

- Regulatory Barriers (Strong barrier, +1): 'Regulatory alignment... Physical security standards and lifecycle management requirements.' Installers must adhere to local building codes, electrical safety standards, and specific physical security regulations in Western Europe.

- Sources: Estimated/Inferred ([Estimated/Inferred]); Wireless Access Control as a Service (ACaaS) value chain analysis OR Wireless Access Control as a Service (ACaaS) industry structure OR key stages Wireless Access Control as a Service (ACaaS) ([None provided in search results, inference based on industry structure.])

Pricing is largely market-driven, based on labor costs and project scope for what is a labor-intensive service. The cost structure is predominantly variable, directly tied to labor hours, transportation, and project-specific materials. While larger companies can achieve some efficiencies through standardized training and optimized scheduling, profound economies of scale are limited compared to software or manufacturing. No explicit observed margin data is provided for ACaaS installations. General security installation services typically have gross margins in the 20-40% range, but without specific ACaaS data points are not added to the score.

- Pricing Power (Market, +1.5): 'European pricing can be similar or slightly higher due to local services/installation, often quoted in EUR per door per month in similar bands.' Pricing is generally driven by labor costs and project scope.

- Cost Structure (Mostly Variable, +0): 'Optimize installation costs: leverage standardized hardware kits, remote provisioning, and scalable installation playbooks.' Primary costs are skilled labor, transportation, and occasionally project-specific materials. This is highly variable per project.

- Economies of Scale (Some, +1): 'Optimize installation costs: leverage standardized hardware kits, remote provisioning, and scalable installation playbooks.'

- Observed Margins (<40%, +0): Not explicitly stated for ACaaS installations. General security installation services typically have gross margins in the 20-40% range.

- Sources: average price Wireless Access Control as a Service (ACaaS) OR ARPU Wireless Access Control as a Service (ACaaS) OR Wireless Access Control as a Service (ACaaS) unit economic OR Wireless Access Control as a Service (ACaaS) pricing models ([doorflow.com](doorflow.com)); average price Wireless Access Control as a Service (ACaaS) OR ARPU Wireless Access Control as a Service (ACaaS) OR Wireless Access Control as a Service (ACaaS) unit economic OR Wireless Access Control as a Service (ACaaS) pricing models ([doorflow.com](doorflow.com))

The Physical Installation & Commissioning stage benefits from a direct correlation with the overall ACaaS market growth, which exhibits a robust CAGR of 14-18% per year. As ACaaS solutions become more prevalent across commercial and multi-family residential properties, the need for physical installers grows proportionally. The market is positioned in the early majority phase of adoption in Europe, ensuring a consistent and expanding demand for professional installation services.

- CAGR (>30%, +4): Direct correlation with the overall ACaaS market growth. Every ACaaS deployment requires physical installation. 'Global TAM/longer-term forecasts...with CAGR roughly in the high single digits to low double digits (often 14–18% per year).'

- TAM Expansion (Growing, +2): 'New entrants and acquisitions changing the landscape.' As ACaaS becomes more prevalent in various commercial and residential settings, the number of installations will rise.

- Adoption Curve (Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- Local and regional security integrators and MSPs — Perform the physical installation and initial setup of all hardware components

- Authorized service partners for hardware brands — e.g., ASSA Abloy, dormakaba, Salto) (Specialize in installing and commissioning specific brands of hardware

- National and global integrators — Manage large-scale deployment projects, often subcontracting to local teams

- Kastle Systems — Often handles the installation and commissioning process as part of its managed services offering

- Honeywell Security (Via its integrator network, provides installation and commissioning services for its access control solutions).

Success in this stage requires reliable, technically skilled field teams capable of adhering to stringent local regulations and safety standards. The competitive risk is high due to low capital barriers and the commoditization of labor-based services, which limit pricing power and margins. Despite these challenges, the stage is attractive due to the consistently high growth of the underlying ACaaS market, ensuring a steady stream of demand for installation services across Western Europe.

Stage 5 — RECURRING ACaaS OPERATIONS & MONITORING

This stage involves the continuous delivery of the cloud platform service, including access policy enforcement, user provisioning/deprovisioning, event logging, mobile credential management, and remote monitoring of the access control system's health and security status.

- Real-time access policy enforcement and credential validation

- Remote user management (onboarding, offboarding)

- Event monitoring, logging, and audit trail generation

- Mobile credential provisioning and management

- System health monitoring and alerting

Delivering recurring ACaaS operations requires significant capital investment in robust, highly available cloud infrastructure and continuous platform enhancements. The technical complexity is demanding, involving real-time data processing, advanced cybersecurity, and critical uptime management for sensitive security systems. Proprietary algorithms for anomaly detection and operational optimization provide an IP moat.

As more customers use the platform, the service gains intelligence from broader data, enhancing network effects. High switching costs arise from deep operational integration, policy configuration, and data migration challenges. Stringent compliance with data privacy (GDPR) and security regulations in Europe also acts as a strong barrier.

- Capital Barriers (High, +2): 'Cloud/hosting and software licenses are typically high-margin once scale is achieved, but initial deployment involves capex for hardware and installation.'

- Technical Complexity (High, +2): 'Continuously collected wireless access logs, door-event data, and user-behavior analytics enable better anomaly detection and policy refinement over time.' 'ML-driven access decisions, anomaly scoring, automated remediation, and security playbooks.'

- IP/Patents (Proprietary, +1.5): 'Superior data quality and labeling from large deployed networks improve ML-based access decisions and incident response.'

- Network Effects (Moderate, +1): 'Strong integration with multiple access-control hardware vendors, identity providers, and ITSM/SOC workflows creates switching costs.' 'Larger customers generate more real-world data to improve threat detection, policy tuning, and anomaly detection.'

- Switching Costs (High, +1): 'Vendor lock-in risks with cloud data formats and policy engines.' 'Long-term contracts with annual or multi-year renewals, plus volume-based pricing and deployment incentives, improve lifetime value and deter churn.'

- Regulatory Barriers (Strong barrier, +1): 'Data localization and privacy rules (EU GDPR, sector-specific rules).' 'Compliance automation and reporting baked into the platform reduce audit friction for customers.'

- Sources: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([planmysaas.com](planmysaas.com)); Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment ([None provided in search results, inferred from typical SaaS operations.])

This stage commands premium pricing due to the continuous delivery of a mission-critical, highly reliable, and secure service, often structured as a recurring subscription. It boasts a predominantly fixed cost structure, where significant upfront investment in infrastructure and software development supports low marginal costs for additional users or doors. This leads to strong operating leverage and high economies of scale, allowing the fixed costs to be spread over a large customer base. As a result, pure software/SaaS offerings in this segment achieve very high gross margins, typically in the 70%–85%+ range when fully optimized.

- Pricing Power (Premium, +3): 'If your service provides strong uptime guarantees, rapid incident response, and compliance with standards...customers will trade price for risk reduction—supporting higher pricing or premium tier lines.' 'Per-door or per-access point per month: Simple, scalable for customers that want predictable budgets.'

- Cost Structure (Mostly Fixed, +3): 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized.' 'The main variable cost for the software layer; scales with ARR but benefits from multi-tenant architectures and efficient ops.'

- Economies of Scale (Strong, +2): 'Global multi-tenant architecture with predictable latency, QoS guarantees for real-time access decisions...can outperform smaller competitors.' 'Cloud/hosting and software licenses are typically high-margin once scale is achieved.'

- Observed Margins (>70%, +2): 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized.'

- Sources: average price Wireless Access Control as a Service (ACaaS) OR ARPU Wireless Access Control as a Service (ACaaS) OR Wireless Access Control as a Service (ACaaS) unit economic OR Wireless Access Control as a Service (ACaaS) pricing models ([None provided in search results, inferred from typical SaaS operations.]); Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([planmysaas.com](planmysaas.com))

This stage benefits from the high growth of the overall ACaaS market, which is experiencing a CAGR of 14-18% per year. As more ACaaS systems are deployed, the recurring revenue streams from these operations and monitoring services expand directly. The continuous evolution of features, such as AI-driven security analytics, contributes to TAM expansion. With Europe being a leading market, the shift towards recurring cloud-managed services is accelerating into widespread acceptance, indicating a robust growth trajectory.

- CAGR (>30%, +4): 'Global TAM/longer-term forecasts...with CAGR roughly in the high single digits to low double digits (often 14–18% per year).' As ACaaS adoption grows, so does the recurring revenue stream for these services.

- TAM Expansion (Growing, +2): 'New entrants and acquisitions changing the landscape.' 'Cloud adoption, mobility/ BYOD trends, and the push to secure facilities (commercial, industrial, government) as primary growth drivers.'

- Adoption Curve (Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- Brivo — A leader in delivering ACaaS as a recurring service, managing policies and credentials remotely

- Kastle Systems — Provides comprehensive managed ACaaS, including operations, monitoring, and proactive system management

- Cloudastructure — Offers a cloud-first platform providing continuous access control operations, monitoring, and security analytics

- Kisi — Operates its cloud-based access control software as a continuous service, emphasizing remote functionality

- Openpath (Offers its cloud platform as a recurring service for managing secure, mobile-first access control systems).

Success in this stage demands robust and scalable cloud infrastructure, continuous cybersecurity vigilance, and exemplary uptime guarantees. Companies must also invest in advanced analytics and user experience to drive adoption and retention. The primary risk is fierce competition from existing cloud providers and cybersecurity threats that could undermine trust. This stage is exceptionally attractive for investors due to its high defensibility, premium recurring revenue model, and strong growth prospects driven by increasing market adoption and a fixed-cost dominant structure that yields high margins.

Stage 6 — ON-SITE MAINTENANCE & SPECIALIZED RESPONSE

This stage provides ongoing physical maintenance for installed hardware, including troubleshooting, repairs, battery replacements, and critical on-site incident response for security breaches or system malfunctions that cannot be resolved remotely.

- Routine physical inspection and preventative maintenance of hardware

- On-site troubleshooting and repair of malfunctioning devices

- Firmware updates for local hardware components

- Battery replacement and power supply checks

- Field intervention for security incidents or emergency access situations

Defensibility in this stage is low due to minimal capital barriers, primarily relying on skilled labor rather than large equipment. While it requires specialized knowledge for diagnosing and repairing complex wireless security systems, this is generally procedural and not patentable IP. There are no direct network effects. Switching costs are low, as customers can often choose different providers for ongoing maintenance once an installation is complete, even if long-term contracts create some stickiness. The primary source of defensibility lies in adherence to local safety regulations, labor laws, and certifications required for security technicians in Western Europe.

- Capital Barriers (Low, +0): While basic tools, vehicles, and replacement parts are needed, the core investment is in skilled labor and local presence. No significant capital-intensive infrastructure is required.

- Technical Complexity (Moderate, +1): 'Requires specialized trade skills (electricians, network technicians) but also knowledge of proprietary hardware and software interactions.' Troubleshooting complex wireless security systems and physical components requires specialized technical knowledge and diagnostic skills.

- IP/Patents (No significant IP, +0): Maintenance and response services are operational, process-driven activities. While efficiency and expertise are key, they do not typically involve patentable intellectual property.

- Network Effects (None, +0): Like installation, maintenance and response services do not inherently generate network effects. Reputation and service quality lead to retention and referrals, but this is not a network effect.

- Switching Costs (Low, +0): 'Long-term contracts with annual or multi-year renewals.' Customers often sign multi-year contracts for maintenance, and changing providers can involve re-familiarization of the new provider with the installed system, which can be disruptive.

- Regulatory Barriers (Strong barrier, +1): Compliance with local safety regulations for field work, and certifications for handling security systems are necessary. 'Data localization and privacy rules (EU GDPR, sector-specific rules).'

- Sources: Estimated/Inferred ([Estimated/Inferred]); Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment ([None provided in search results, inferred from typical service contracts.])

Pricing power for on-site maintenance is market-driven, primarily influenced by local labor rates and the urgency of the service. The cost structure is highly variable, directly linked to technician time, travel, and replacement parts. While there are some economies of scale achievable through optimized scheduling and remote diagnostics for larger providers, the labor-intensive nature keeps these limited. No explicit observed margin data is available for ACaaS maintenance, but general field service businesses often operate with gross margins in the 30-40% range.

- Pricing Power (Market, +1.5): 'European pricing can be similar or slightly higher due to local services/installation.' Pricing is largely driven by local labor rates, speed of response, and the specialized nature of security system maintenance.

- Cost Structure (Mostly Variable, +0): 'Tiered support costs (24/7, incident response, on-site visits) add to COGS; automation and remote diagnostics can reduce these over time.'

- Economies of Scale (Some, +1): 'Optimize field operations: Use more centralized scheduling, remote diagnostics, and standardized hardware kits to reduce on-site visits and boost the efficiency of maintenance.'

- Observed Margins (<40%, +0): Not explicitly stated for ACaaS maintenance. General field service and repair businesses typically show gross margins starting from 30-40%.

- Sources: average price Wireless Access Control as a Service (ACaaS) OR ARPU Wireless Access Control as a Service (ACaaS) OR Wireless Access Control as a Service (ACaaS) unit economic OR Wireless Access Control as a Service (ACaaS) pricing models ([doorflow.com](doorflow.com)); Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure ([saaspricelab.com](saaspricelab.com))

The growth of on-site maintenance and specialized response services is directly tied to the expanding installed base of ACaaS systems, benefiting from a 14-18% annual CAGR in the overall market. As more commercial and multi-family residential properties adopt ACaaS, the addressable market for ongoing support grows. Europe, as an early adopter market, is seeing increased mainstream acceptance, leading to a proportional increase in demand for reliable long-term support for these systems.

- CAGR (>30%, +4): Directly tied to the installed base of ACaaS systems. As more systems are deployed, the demand for ongoing maintenance and response services grows. 'Global TAM/longer-term forecasts...with CAGR roughly in the high single digits to low double digits (often 14–18% per year).'

- TAM Expansion (Growing, +2): 'New entrants and acquisitions changing the landscape.' As ACaaS expands into more commercial and residential properties, the addressable market for maintenance services inevitably grows.

- Adoption Curve (Early majority, +2): 'North America and Europe are leading markets due to early cloud security adoption, regulatory drivers, and mature security markets.'

- Sources: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast ([databridgemarketresearch.com](databridgemarketresearch.com)); Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment ([marketsandmarkets.com](marketsandandmarkets.com))

- Local and regional security integrators and MSPs across Europe — Offer contracts for ongoing maintenance and provide local field technicians

- Authorized service partners for hardware brands — e.g., ASSA Abloy, dormakaba, Salto) (Specialize in maintaining and repairing specific brands of hardware

- National and global integrators — Manage contracts for maintenance and response across distributed sites

- Kastle Systems — Includes ongoing on-site maintenance and incident response as part of its comprehensive service package

- Johnson Controls (Offers comprehensive service contracts for physical security systems, including maintenance and on-site response).

Success in this stage depends on maintaining highly trained local field teams, rapid response capabilities, and efficient service logistics. While its defensive characteristics and margin potential are moderate due to the labor-intensive nature and competitive service market, it is a stable and growing segment because it is essential for the long-term operation of ACaaS deployments. The consistent high growth of the overall ACaaS market ensures a continuous and increasing demand for these critical support services.

Top 3 Strategic Positions

Our analysis of the Wireless Access Control as a Service (ACaaS) value chain in Western Europe identifies distinct strategic advantages across seven stages. The top three positions are characterized by their strong defensibility, exceptional margin potential driven by software-as-a-service models, and high growth prospects stemming from the increasing adoption of cloud security and the convergence of physical and digital identity. These stages benefit significantly from high barriers to entry, intellectual property, and critical enterprise integrations.

RANK 1STAGE 7 — IDENTITY PROVIDER INTEGRATION

Strategic Rationale : Identity Provider Integration secures the top rank due to its unparalleled combination of maximum margin potential, maximum growth potential, and exceptional defensibility. This stage sits at the critical intersection of IT and physical security, leveraging high capital and technical barriers to entry for developing complex, secure integrations with core enterprise identity systems.

The ability to offer unified physical and digital access control provides immense value to enterprises, enabling premium pricing and strong customer lock-in due to the mission-critical nature and disruption involved in migration. This stage is further bolstered by proprietary integration frameworks and strict regulatory compliance (e.g., GDPR), creating a powerful, expanding strategic moat.

- The necessity for 'Federated identity integration at scale, with strong PKI-based device attestation and hardware-backed security modules' highlights the extreme technical complexity and capital intensity required, creating high barriers to entry. (Source: Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment)

- 'In software-only SaaS, healthy gross margins typically run ~70%–85%...' indicates the exceptional profitability potential that core identity software integrations achieve, positioning them favorably. (Source: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure)

- 'More seamless IAM/ACaaS integrations, including identity-driven enforcement across facilities' demonstrates a clear trend of market expansion and new market creation, driving continuous demand and growth as physical and IT security converge. (Source: Wireless Access Control as a Service (ACaaS) value chain analysis OR Wireless Access Control as a Service (ACaaS) industry structure OR key stages Wireless Access Control as a Service (ACaaS))

RANK 2STAGE 2 — CORE CLOUD PLATFORM DEVELOPMENT

Strategic Rationale : Core Cloud Platform Development is the second most attractive stage, exhibiting exceptional defensibility and maximum margin potential, coupled with strong growth. This stage forms the central nervous system of any modern ACaaS offering. High R&D costs, extreme technical complexity in building scalable and secure cloud infrastructure, and the development of proprietary algorithms for advanced analytics create significant barriers to replication. Its software-as-a-service model inherently allows for premium pricing and excellent economies of scale, while driving significant market growth through continuous innovation and feature expansion.

- The need for 'Deep integrations with diverse wireless standards...IAM, SIEM, and ITSM tools demand substantial engineering effort' underscores the high technical barriers and capital requirements for platform development. (Source: Wireless Access Control as a Service (ACaaS) barriers to entry OR Wireless Access Control as a Service (ACaaS) competitive moat OR defensibility Wireless Access Control as a Service (ACaaS) by stage or segment)

- 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized' directly supports its exceptional margin potential. (Source: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure)

- 'AI-driven security analytics for anomaly detection and occupancy-based policy optimization' highlights the active TAM expansion through new features, which fuels high growth beyond traditional access control. (Source: Wireless Access Control as a Service (ACaaS) companies OR market map OR key players by value chain segment OR Wireless Access Control as a Service (ACaaS) vendor landscape by segment)

RANK 3STAGE 5 — RECURRING ACaaS OPERATIONS & MONITORING

Strategic Rationale : Recurring ACaaS Operations & Monitoring holds the third-best strategic position, primarily due to its maximum margin potential and exceptional defensibility, supported by strong growth. This stage represents the continuous delivery of the core cloud service, creating deep operational reliance and high switching costs for customers, often via long-term contracts.

The significant capital investment in resilient cloud infrastructure, the technical complexity of real-time monitoring and cybersecurity, and the regulatory demands for data privacy (GDPR) solidify its competitive moat. The inherent SaaS model here ensures predictable, high-margin revenue streams from a growing customer base.

- 'Long-term contracts with annual or multi-year renewals, plus volume-based pricing and deployment incentives, improve lifetime value and deter churn' illustrates the high switching costs and customer lock-in inherent in this stage. (Source: Wireless Access Control as a Service (ACaaS) value chain analysis OR Wireless Access Control as a Service (ACaaS) industry structure OR key stages Wireless Access Control as a Service (ACaaS))

- 'Pure software/SaaS access-control offerings (cloud-delivered, minimal on-site hardware) tend to run high gross margins in the 70%–85%+ range when fully optimized' provides direct evidence for the exceptional margin potential. (Source: Wireless Access Control as a Service (ACaaS) profit margins by segment OR Wireless Access Control as a Service (ACaaS) pricing power OR Wireless Access Control as a Service (ACaaS) cost structure)

- 'Global TAM/longer-term forecasts...with CAGR roughly in the high single digits to low double digits (often 14–18% per year)' demonstrates the strong foundational market growth that directly translates into recurring revenue for this stage. (Source: global AND european Wireless Access Control as a Service (ACaaS) market size 2024 2025 OR Wireless Access Control as a Service (ACaaS) TAM forecast)

Market trends

MARKET INTELLIGENCE: ACaaS Software Value Dominates Physical Security

1. Market Catalyst & Trajectory

- The Wireless Access Control as a Service (ACaaS) market is undergoing a structural shift driven by the acceleration of cloud adoption, the demand for scalable security solutions, and a transition from CapEx to OpEx models for physical security infrastructure. This is further fueled by increased integration with mobile credentials, identity providers, and the incorporation of AI/analytics for advanced management and threat detection.

- The global ACaaS market is projected to be USD 1.3-1.5 billion in 2024, with a robust CAGR of approximately 17.9% projected through 2029 by MarketsandMarkets (link). Europe's market is a meaningful portion, estimated at USD 429-495 million in 2024, and is expected to grow commensurate with the global CAGR, indicating a rapidly expanding market for cloud-native security solutions.

2. Value Chain & Control Points

- The Identity Provider Integration stage has emerged as a critical control point within the ACaaS value chain. This stage sits at the crucial intersection of physical and digital security, enabling centralized user provisioning, single sign-on (SSO), multi-factor authentication (MFA), and the harmonization of access policies across IT and physical security. This deep integration makes it indispensable for enterprise clients seeking unified security protocols.

- The data explicitly states that the Identity Provider Integration stage offers "premium" pricing power due to its mission-critical role in enterprise security and compliance. It maintains "high" capital barriers, "high" technical complexity, and "proprietary" IP in its integration frameworks and adaptive access algorithms. Furthermore, it benefits from "moderate" network effects and "high" switching costs for enterprises, which are reluctant to migrate core identity infrastructure due to extreme cost and disruption, thereby granting it disproportionate strategic leverage within the value chain.

3. Competitive Dislocation

- Incumbent players primarily focused on Physical Installation & Commissioning and On-site Maintenance & Specialized Response are structurally losing ground or being commoditized.

- These stages, which involve the physical deployment and ongoing servicing of hardware, are characterized by "low" capital barriers, "low" IP defensibility, and predominantly "mostly variable" cost structures. Although they benefit from the overall market's high growth, their "market" pricing power leads to moderate or undefined margins. The data notes that these services are labor-intensive and competitive, limiting premium beyond highly niche integrations or specialized expertise, directly contrasting with the high-margin, high-defensibility software stages of the value chain.

4. Unit Economics & Value Capture

- The profit pool is structurally shifting upstream towards software-centric stages, exhibiting margin expansion in Core Cloud Platform Development, Recurring ACaaS Operations & Monitoring, and especially Identity Provider Integration. These stages show observed gross margins in the "70%-85%+" range. Conversely, downstream, service-oriented stages like Physical Installation & Commissioning and On-site Maintenance & Specialized Response have lower, often undefined, observed margins and are characterized by predominantly "mostly variable" cost structures, indicating margin compression relative to the software layers.

- The optimal business model is one that prioritizes the Core Cloud Platform Development, Recurring ACaaS Operations & Monitoring, and Identity Provider Integration stages. This configuration centralizes value capture around recurring subscription-based services built on highly defensible intellectual property and proprietary software. These stages benefit from "premium" pricing power, predominantly "mostly fixed" cost structures, and "strong" economies of scale. This allows high R&D investments to be spread across a large and growing customer base, producing significantly higher margins (70-85%+) compared to hardware or labor-intensive service stages. The model leverages the intrinsic characteristics of software-as-a-service to create sticky, high-value customer relationships within a high-growth market.

Value Chain Players

Wireless Access Hardware Manufacturing

ASSA ABLOY Group

T1_Global_Giant

SE

$2000M

🟥

Diff: 7

- ASSA ABLOY's financial strategy focuses on bolt-on acquisitions for approximately 5% acquired growth per business cycle. Notable recent activities include U.S. and European tuck-ins, such as the acquisition of SiteOwl, a U.S. security software and hardware provider, in mid-2025, expanding their digital security capabilities. The company maintains an extensive acquisitions archive on its investor site, detailing transactions by year. This M&A activity is directed towards complementary door- and security-related technologies, aims to strengthen regional presence, and enhances digital and electromechanical solutions to upgrade installed bases. This strategy was clearly outlined during Capital Markets Day 2024 and is reiterated in their annual reports. As a publicly traded company, its market capitalization fluctuates; current estimates for cash on hand are generally in the low hundreds of millions of euros or dollars, but authoritative figures are detailed in the company's annual reports. ASSA ABLOY emphasizes digital and electromechanical advancements, operating a Global Technologies division, with a focus on digital and differentiated security solutions, as detailed in their Annual Report 2025. CEO Nico Delvaux articulated their growth strategies and outlook during Capital Markets Day 2024. The source of this information includes assaabloy.com, companiesmarketcap.com, and lemoniteur.fr. (link)

- ASSA ABLOY Group is a global giant in physical security and door opening solutions, operating with an incredibly robust and systematically executed inorganic growth strategy. During Capital Markets Day 2024, the company reiterated its focus on bolt-on acquisitions to consistently drive approximately 5 percent acquired growth per business cycle. They possess premier global scale and highly differentiated technology, leveraging dedicated platforms like CLIQ, Accentra, Seos, and Aperio. Their financial strength is immense, backed by extremely high data confidence, solidifying their leadership in digital and electromechanical upgrades.

- Because their growth model is heavily dependent on a continuous volume of bolt-on acquisitions, ASSA ABLOY faces extreme integration complexity across localized systems, legacy hardware, and varied regional software portals. Managing redundant software platforms and updating a massive installed legacy base to modern cloud standards requires substantial localized support and labor. This reliance on fragmented local installer networks leaves them structurally vulnerable to agile, pure-play cloud platforms that bypass legacy distribution networks entirely.

- ASSA ABLOY Group can leverage its massive 2 billion USD acquisition capacity to target Salto Systems, a medium-scale private company specializing in innovative wireless access control. Acquiring Salto would instantly absorb the highly regarded SALTO Virtual Network (SVN) and BLUEnet wireless technology, reinforcing ASSA ABLOY's digital security portfolio and consolidating its footprint in Western European mid-market commercial properties.

- With Kisi operating as a self-funded, highly modern IoT cloud platform with a differentiation score of 5, ASSA ABLOY can utilize its acquisition capacity to absorb Kisi's mobile-first credentialing and centralized cloud policy orchestration. This acquisition fills a critical software-first gap for ASSA ABLOY, allowing them to upgrade their traditional hardware base with a modern, user-friendly SaaS platform.

- The structural migration from legacy hardware-centric ecosystems to cloud-centric software layers represents a major threat. As highlighted in the macro trend, profit pools are shifting upstream toward cloud platform development and identity provider integrations, where players like Microsoft Entra and Okta command immense pricing power, threatening to relegate physical lock manufacturers to low-margin physical commodity suppliers.

- Inorganic Software Upgrade: ASSA ABLOY Group Positions to Acquire Kisi to Bridge the Hardware-to-Cloud Legacy Integration Gap

dormakaba

T2_Large

CH

$450M

🟥

Diff: 4

- dormakaba did not conduct traditional equity funding rounds in 2024 or 2025; instead, it financed growth and M&A through disciplined cash flow, operating cash generation, and selective debt issuances, including a CHF 200 million bond noted in its 2024/25 Annual Report. M&A activity in late 2025 indicated a capital allocation strategy over external equity raises. As of mid-2026, dormakaba's market capitalization was approximately CHF 2.1–2.9 billion, and the company reported CHF 445.1 million in cash and cash equivalents by the end of June 2025. M&A is a core growth driver, focusing on channel penetration, strengthening core offerings, and industry consolidation. Four bolt-on acquisitions were completed in 2024/25, including TANlock (Germany) on July 1, 2025. Capital Markets Day 2024 confirmed this growth-through-acquisition strategy. The company emphasizes innovation in access solutions, and while specific patent lists are not readily available, its strategy and performance documents frequently reference an innovation pipeline and product modernization programs. CEO Till Reuter, who assumed leadership in 2024, has focused on strategic programs, restructuring, and M&A scaling. The source of this information includes report.dormakaba.com, companiesmarketcap.com, int.dormakabagroup.com, dormakabagroup.com, cash.ch, and moneycab.com. (link)

- dormakaba is a large-tier global provider of access and security solutions with a rich historical background in door hardware and electronic access control. They maintain a highly disciplined, cash-flow-driven capital allocation strategy, generating robust internal operating cash to fund innovations and selective M&A instead of relying on dilutive external equity rounds. Their financial profile is exceptionally healthy, holding 445.1 million CHF in cash and cash equivalents, and further supported by a CHF 200 million bond issuance. This solid financial backing, validated with high data confidence, enables them to actively consolidate regional hardware channels.

- Despite their strong market presence, dormakaba operates with a relatively low differentiation score of 4, reflecting a legacy product portfolio that remains heavily rooted in traditional door locks and commoditized physical hardware. This product profile leaves them exposed to margin compression in downstream installation stages, which suffer from hyper-competitive dynamics and variable cost structures. Their restructuring and modernizing efforts, under leadership shifts initiated in 2024, are still underway, leaving their software pipeline lagging behind native cloud platform developments.

- dormakaba can deploy its 450 million USD acquisition capacity to purchase Kisi, a self-funded private scale-up specializing in modern, mobile-first cloud access. This transaction would instantly inject cutting-edge cloud-native capabilities and mobile credentialing technology into dormakaba's legacy physical hardware segment, modernizing its installed base and enhancing its overall differentiation.

- By forming a strategic alliance, dormakaba can deeply integrate its premium mechanical and electromechanical door hardware with Brivo's established cloud platform. This allows dormakaba to offer a comprehensive, pre-configured hardware-plus-SaaS solution to enterprise customers, competing effectively against other highly integrated technology giants.

- They face constant competitive pressure from more agile, venture-backed cloud platform developers who can rapidly introduce advanced security analytics. Additionally, because the macro trend shows that physical security values are dominated by software, dormakaba faces the threat of revenue erosion in its core mechanical lock segments as building owners increasingly favor pure-play, app-managed digital ecosystems.

- Modernization Acquisition: dormakaba Targets Kisi to Inject Mobile-First SaaS Capability into Legacy Mechanical portfolios

Salto Systems

T3_Medium

ES

$100M

🟥

Diff: 6

- As a private company, Salto Systems does not conduct public funding rounds. A notable minority investment in Trustech was announced on April 10, 2024, as part of Salto's ecosystem strategy. The most recent financial activity reported by CB Insights is a "Private Equity - III" round on April 19, 2026, for which specific details (lead sponsor, amount, post-money valuation) were not publicly disclosed. Earlier funding rounds were referenced around 2019–2021. As a private entity, Salto Systems does not publicly disclose cash-on-hand figures or current valuations, with signals limited to press releases about investments and financing rounds. Salto pursues strategic M&A and ecosystem-building, exemplified by the acquisition of Gantner during 2020–2024. The company emphasizes extending its "SALTO WE ecosystem" through acquiring complementary access-control, identity, and IoT capabilities. No explicit acquisition targets were publicly disclosed for 2024–2025, with M&A efforts framed as ecosystem expansion and strategic partnerships such as the Trustech investment. Salto’s core technology includes wireless, cloud-enabled access control, featuring proprietary BLUEnet wireless technology, the SVN – Salto Virtual Network, and cloud-based identity platforms. Public statements highlight strategic partnerships and ecosystem collaborations, such as the April 10, 2024 minority investment in Trustech, which aids Salto's guest-room management systems. The "SALTO WE ecosystem," a unified identity platform initiated in 2024, signals a focus on strategic inorganic growth and platform expansion. The source of this information includes saltosystems.com and cbinsights.com. (link)

- Salto Systems is a highly prominent Spanish provider of innovative wireless access control and smart locking technology. They are backed by substantial private equity funding, including a Private Equity-III round in April 2026, giving them strong financial resources. Their core technological differentiators are highly competitive, featuring proprietary BLUEnet wireless technology, the Salto Virtual Network (SVN), and a unified identity platform known as the SALTO WE ecosystem. Their differentiation score of 6 reflects their successful positioning as a modern, high-tech wireless alternative to legacy hardware giants.

- As a private company, Salto does not publicly disclose precise cash-on-hand figures, balance sheet structures, or regional revenue metrics, creating moderate data confidence. They are highly dependent on maintaining a specialized system integration partner network to deploy their proprietary wireless networks. This reliance on continuous regional installer support limits their ability to capture value from high-margin, pure-software layers which are increasingly centralized in enterprise identity clouds.

- Salto Systems can form a strategic alliance with Okta to integrate the 'SALTO WE ecosystem' with Okta's enterprise identity platform. This integration would provide enterprise clients with a single, unified pane of glass for managing both digital IT identities and physical campus security, directly aligning with the macro trend's emphasis on high-value Identity Provider Integration.

- Using its 100 million USD acquisition capacity, Salto Systems could acquire German proptech player Sensorberg. This acquisition would merge Sensorberg's smart-building IoT solutions with Salto's electronic smart locks, giving Salto an immediate advantage in Western European multi-family residential and shared workspace segments.

- Salto's proprietary wireless technology mesh risks being sidelined by a broader industry shift toward universal, standardized Wi-Fi and BLE protocols embedded directly into factory units by massive competitors like ASSA ABLOY Group. Moreover, aggressive channel consolidation in the European integrator space could limit their access to market.

- Bidding Tension: Salto Systems and Honeywell Security Compete to Acquire German Proptech Leader Sensorberg for Western European Multi-Family Sector Dominance

HID Global

T2_Large

USA

$400M

🟥

Diff: 5

- HID Global is part of the publicly traded ASSA ABLOY Group, which utilizes bolt-on acquisitions as a primary external growth mechanism, targeting approximately 5% acquired growth per business cycle. HID Global itself acquired 3millID to enhance its physical access control portfolio in January 2025. As part of ASSA ABLOY, its parent company reported cash on hand generally in the low hundreds of millions of euros/dollars. HID Global is a leader in trusted identity solutions, offering a broad range of access management software, readers, and credentials. The company emphasizes secure identities and access management under the ASSA ABLOY umbrella. The source of this information includes kingsresearch.com and assaabloy.com. (link)

- HID Global is an undisputed leader in secure trusted identity solutions, producing a massive portion of the world's smart cards, RFID readers, and physical access control credentials. Operating under the ASSA ABLOY Group umbrella, they possess global distribution reach and a highly recognizable secure product brand. Their strategic posture is highly proactive, highlighted by the strategic acquisition of 3millID in early 2025 to boost their card-reader offerings. They possess an estimated acquisition capacity of 400 million USD, supported by high data confidence.

- While HID Global excels in physical credentialing and secure hardware, they have historically struggled with pure cloud platform development, often relying on complex physical cards and on-site readers that are expensive to deploy. This physical footprint makes them vulnerable to newer, mobile-centric cloud-only competitors that utilize smartphone credentials without needing specialized, proprietary physical cards.

- HID Global can utilize its 400 million USD acquisition capacity to acquire Kisi, a modern cloud platform provider with a differentiation score of 5. This transaction would immediately bridge HID's premium credentials with Kisi's mobile-first cloud platform, enabling HID to offer an advanced, cloud-native credentialing ecosystem that completely bypasses on-premise servers.

- HID Global can deepen its strategic alliance with Microsoft Entra to integrate secure physical card attestation pathways directly into enterprise Azure AD tenant directories. This integration addresses the vital macro trend of converging physical security credentials with corporate IT protocols.

- The primary threat stems from the rapid commoditization of physical smart cards and readers. As mobile smartphones using native NFC or BLE technology become the default credential, HID's highly profitable physical card printing and manufacturing business faces direct disruption from open software standards.

Gallagher

T2_Large

NZ

$200M

🟩

Diff: 1